Sukuk is usually known as Islamic bonds. It has been the most active Islamic fixed income market instrument. When you buy bonds, you are basically lending the money to the bond issuer for a set period of time. You will get a predetermined interest rate and usually, you will receive it annually in a fixed period of time. The bond's principal is then repaid at the end of the period, and you receive your money back.

However, this transaction is similar to generating money from money (interest or riba) which Islam prohibits. Therefore, Sukuk comes to bridge the gap between Islamic financing and the global capital market.

The AAOFI defines Sukuk as:

“Certificates of equal value representing undivided shares in ownership of a tangible asset, usufruct and services, assets of particular projects or special investment activity.”

While IFSB defines Sukuk as:

“Certificates that represent the holder’s proportionate ownership in an undivided part of the underlying asset where the holder assumes all rights and obligations to such asset.”

The issuance of Sukuk and its trading must follow the Shariah principles, which prohibit riba or interest. Unlike bondholders, Sukuk holders are given the ownership interest in the assets or the financed business, and the return is based on the asset's performance. Sukuk is classified into two categories based on its technical and commercial features, namely Asset-Based Sukuk and Asset-Backed Sukuk. Here is the explanation of both types of Sukuk.

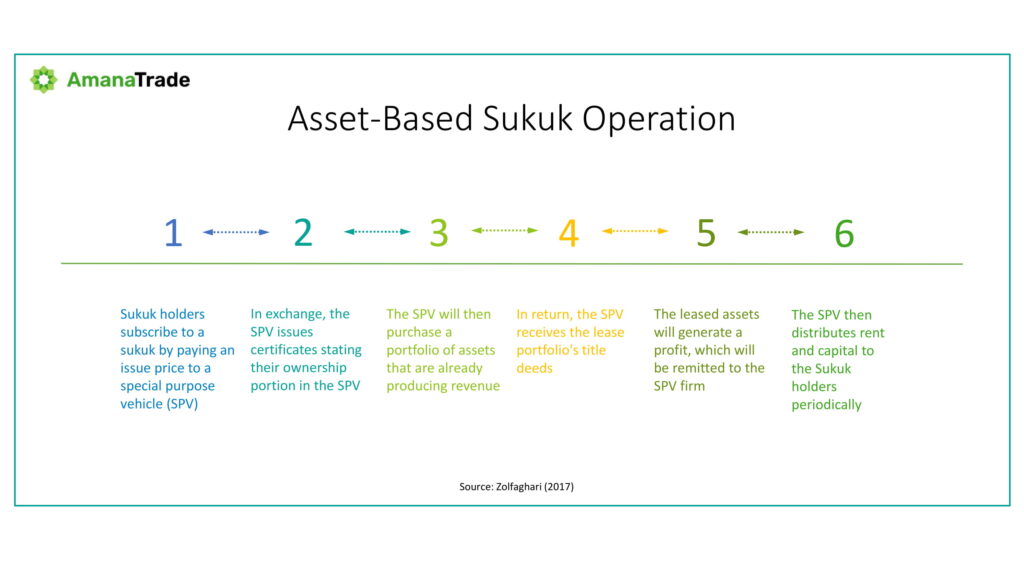

Asset-Based Sukuk

In this type of Sukuk, the Sukuk issuer, usually Special Purpose Vehicle (SPV), purchases the underlying assets and then invests, trades, or leases them on behalf of Sukuk holders using the fund raised from the issuance of Sukuk certificate. The originator (the raising fund company) only transfers beneficial ownership of the asset to the Sukuk holders. In other words, there is no actual sale in an asset-based structure from the legal point of view because the Sukuk holders have no interest in the underlying asset. This arrangement is most commonly disguised as a sale-lease to the originator. Later, the originator promises to repurchase the underlying assets at maturity. As a result, Sukuk holders cannot sell the asset to a third party, which means that Sukuk holders can only recourse to the originator.

In this case, Sukuk holders own the asset through the SPV. The rental payments will provide the return, and the Sukuk is finally redeemed at a pre-determined value. Because the lessee is the obligor, the Sukuk holders have recourse to the obligor in the event of default. Therefore, this kind of Sukuk is likely to reflect debt or bonds.

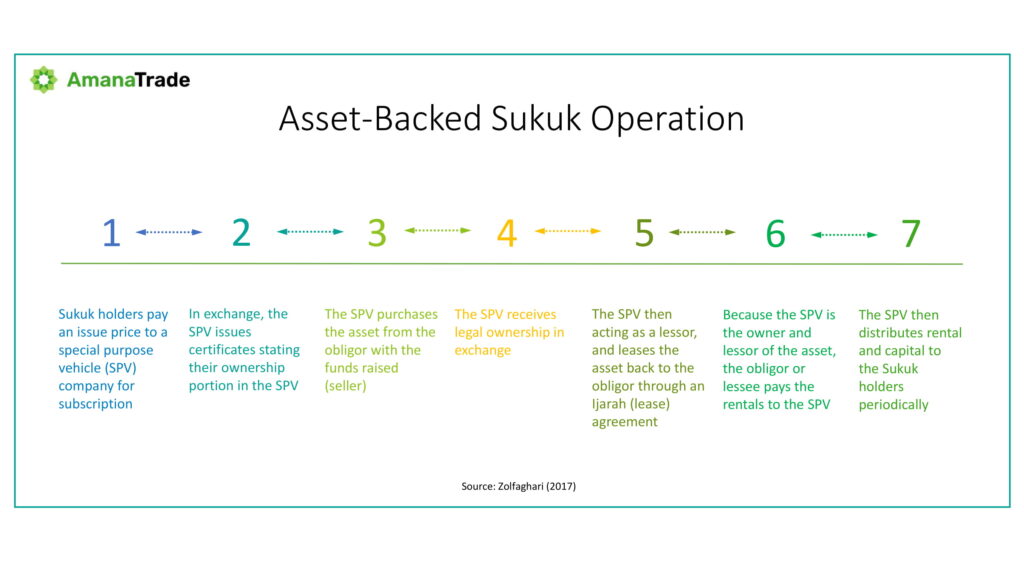

Asset-Backed Sukuk

In Asset-backed Sukuk, the investors receive a share of a tangible asset or business venture, along with its total risk. Furthermore, this transaction entails the asset's sale and the transfer of legal ownership from the originator to a Special Purpose Vehicle (SPV). The SPV is then an explicit trustee of the Sukuk holders, receiving fees as the Sukuk issuer. While the Sukuk holders are legal part-owners of the underlying asset, receiving a return on investment based on the underlying asset’s performance. To put it another way, Sukuk holders rely only on the underlying asset for payment because the asset has already been detached from the originator’s books, and there will be no appeal to the originator.

In addition, Asset-backed Sukuk has the characteristics of equity financing where the SPV owns the asset. Therefore, The SPV takes all of the risks and advantages of ownership. If the underlying asset does not raise the return, the Sukuk holders will suffer losses.

5 Differences Between Asset-Based and Asset-Backed Sukuk

Based on the definitions mentioned above, we can summarize the difference between Asset-Backed and Asset-Based Sukuk as follow:

| No | Categories | Asset-Based | Asset-Backed |

| 1 | Source of Payment | Originator/obligor's cash flows. | Revenue generated by the underlying asset. |

| 2 | Presentation/disclosure of the asset | The asset remains on the originator’s/obligor’s balance sheet. | The asset is separated from the originator's book. |

| 3 | Type of Sukuk holders' Ownership | Beneficial ownership with no right to dispose of the asset. | Legal ownership with the right to dispose of assets. |

| 4 | Recourse | Purchase undertaking at par from obligor is the ultimate recourse. Therefore, the recourse is only to the obligor and not the asset. | Sukuk holders only have recourse to the asset. Thus, asset plays a genuine role in defaults |

| 5 | Shariah Nomination | This structure involves both ba'i al-dayn and ba'i al-inah. | Because of its equity-like nature, this structure is considered shari'a-compliant |

The illustrations below describe the difference between Asset-Based and Asset-Backed Sukuk operations:

The structure of asset-based Sukuk is almost similar to debt instruments. Moreover, this type of Sukuk is what investors were seeking and what the market wanted. This is because the issuers want to raise funds without having to sell any assets. On the other hand, Investors did not want to become asset owners and take on the associated risks. Therefore, this Sukuk type replicated debt-like instruments.

To read more about Islamic Finance related topics, please click here and visit our academy.

Besides, feel free to sign up for our free stock screening services at musaffa.com.

Musaffa

Musaffa