The Smart Way to Build Halal Wealth

Learn the basics, understand Shariah compliance, start investing with confidence

Align your

Wealth

Wealth

Build investments that match your Islamic values.

Understand Compliance

Learn what makes investments halal or not-halal.

Start

Confidently

Confidently

Apply principles immediately with clear guidance.

2-3 Hours per Course

Transform how you invest through focused lessons.

Certified Courses

Structured, self-paced programs with shareable certificates.

Coming Soon

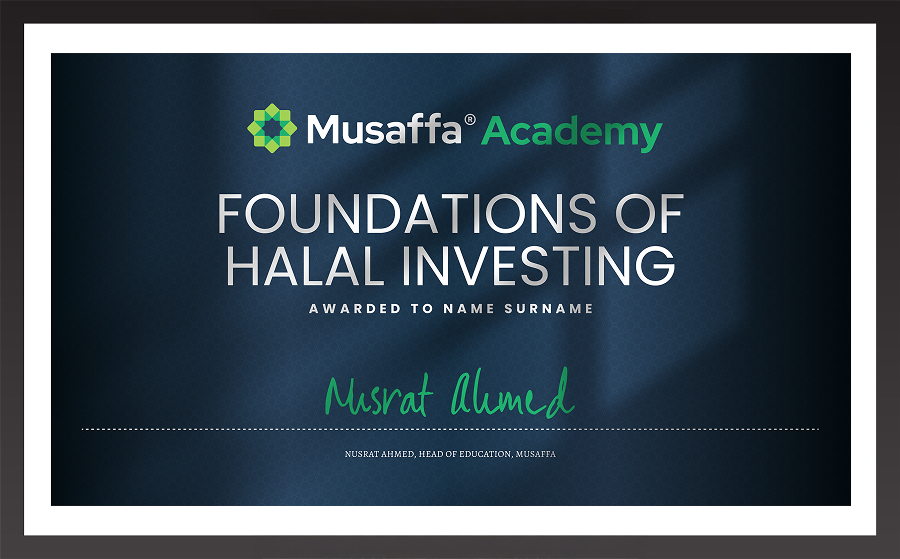

Foundations of Halal Investing

Understand investing essentials through an Islamic finance lens.

2 hours

Coming Soon

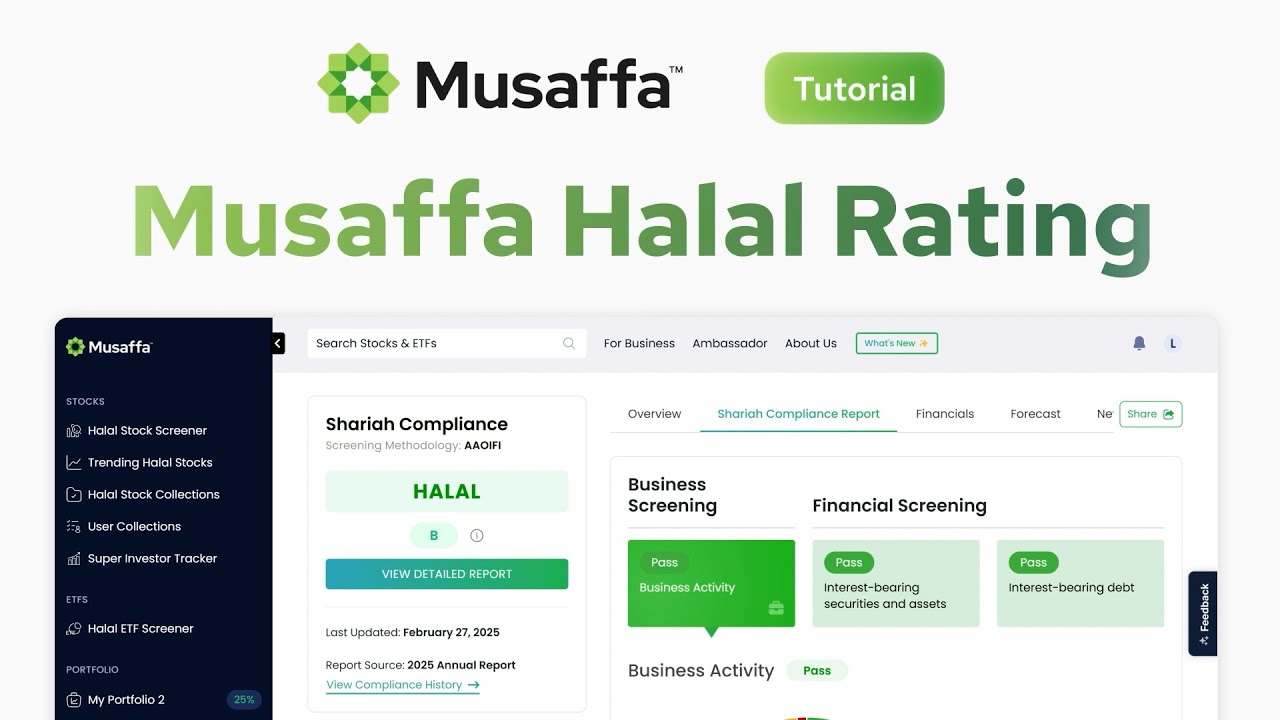

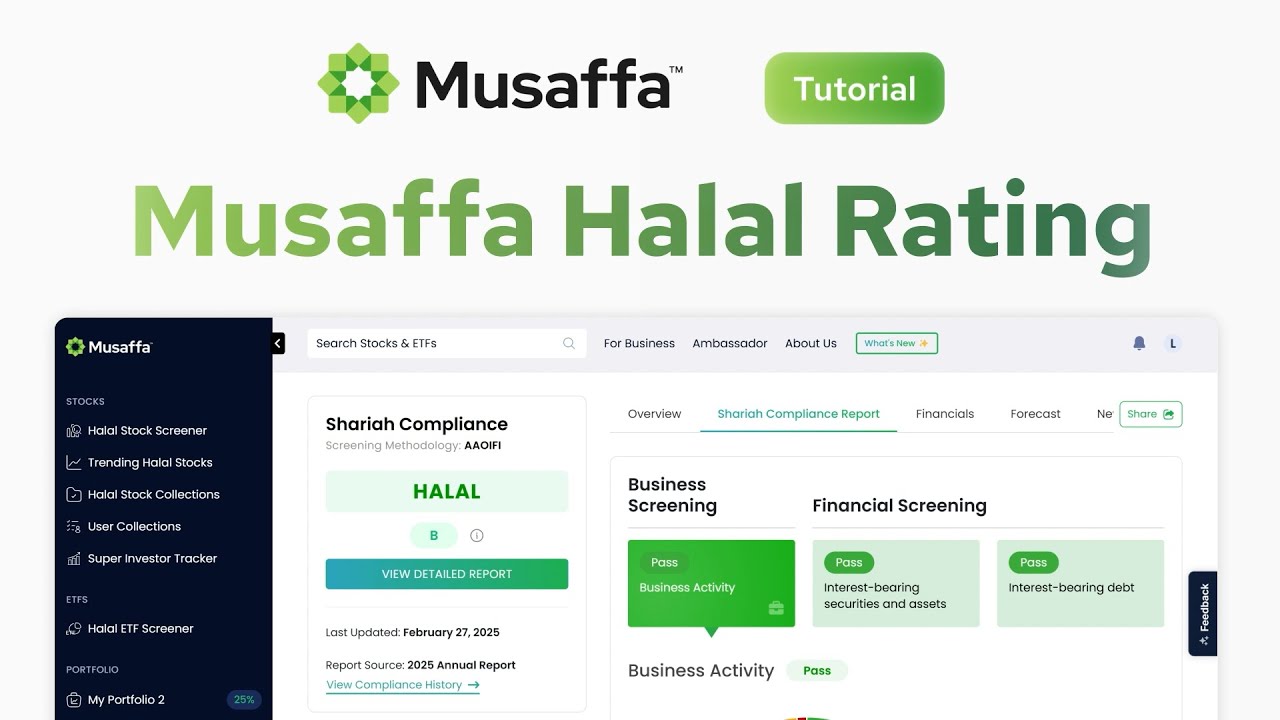

How to Screen Stocks for Halal Compliance

How to evaluate equities for halal compliance.

2 hours

Coming Soon

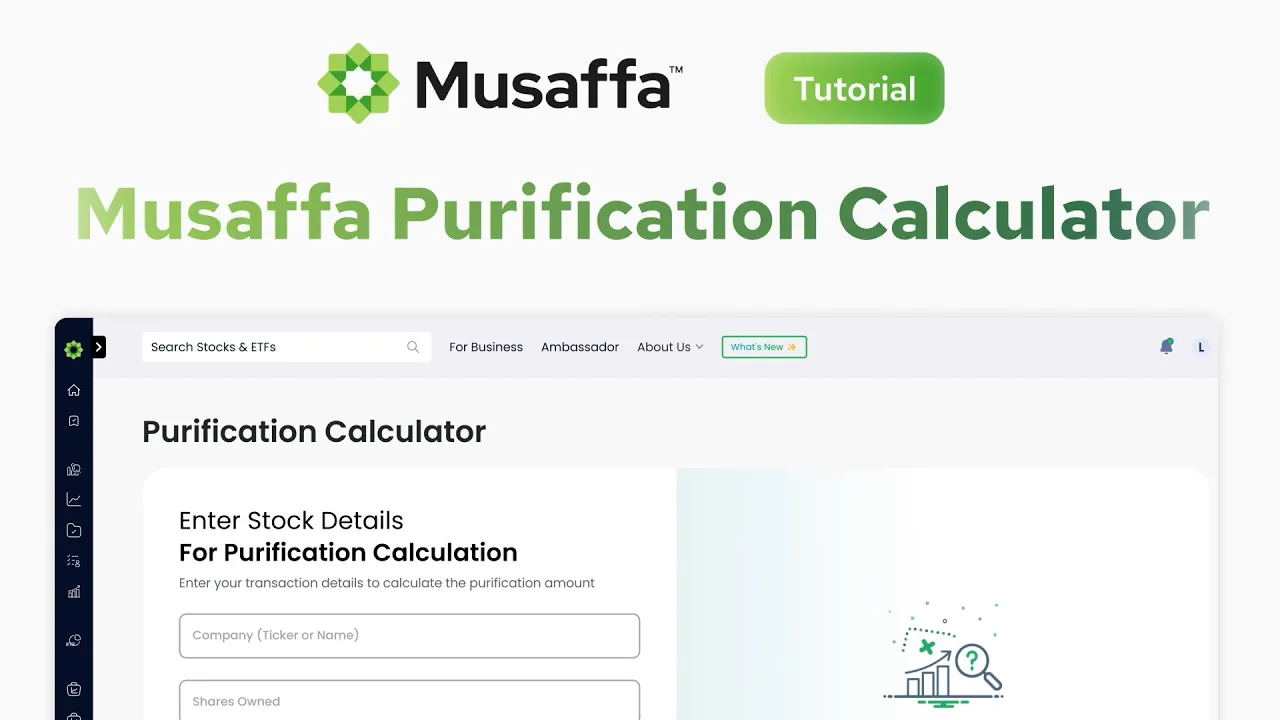

Purifying Your Halal Investments

How to remove non-halal earnings and keep your portfolio compliant.

2 hours

Official Recognition of Your Expertise

Musaffa Learn - Halal Trading

Fast, simple mini-courses to help you prepare for trading.

What Is Zakat on Investments?

Passive vs. Active Investing

What Is a REIT?

What Are Other Methodologies?

What Learners Are Saying

Musaffa Learn’s mini-courses made everything feel simple and approachable. Each lesson is short enough to finish in minutes, and I finally understand the basics without feeling overwhelmed.

Marketing Manager

The mini-courses are perfectly designed. They are quick, direct, and practical. I went through several finance and trading basics in one weekend and immediately felt more confident.

Business Owner

The market basics were helpful, but the bite-sized Shariah lessons were exactly what I needed. Now I understand not only which investments are halal, but why they’re screened that way.

Teacher

Get Your Questions Answered

Coming Soon

Ask a Shariah Scholar

Have a question about Halal investing or Islamic finance? Our shariah scholars provide clear, trustworthy answers.

Coming Soon

Ask Ai

Need instant answers? Use our AI assistant to quickly clarify concepts, tools, and strategies anytime.

Coming Soon

Ask an Analyst

Curious about finance? Our finance analysts answer your questions with context, examples, and step-by-step explanations — no matter how basic.

Past Live Sessions

View recordings of past webinars.

Beyond ESG and Shariah Screens: Introducing MISRI – Live Webinar

15 days ago

Musaffa Fintech

YouTube

Understanding Zakat with Mufti Mirza-Zain Baig - Live Webinar

18 days ago

Musaffa Fintech

YouTube

Investing and Crypto Halal Portfolio – Live Webinar with Fasset!

1 months ago

Musaffa Fintech

YouTube

Preparing for Ramadan: A Budgeting Workshop with Sister Fatimah Jangana

1 months ago

Musaffa Fintech

YouTube

Foundations of Islamic Wealth Management Live Webinar with Br. Abdul Basith

1 months ago

Musaffa Fintech

YouTube

The X-Curve for Muslim Families: Wealth, Security & Stability with Br. Areeb Khawaja

2 months ago

Musaffa Fintech

YouTube

Money with Meaning | Musaffa & Crescent Private Wealth

3 months ago

Musaffa Fintech

YouTube

Rethinking Wealth: Halal Investing & the Myths Holding Muslim Women Back

4 months ago

Musaffa Fintech

YouTube

Biggest Musaffa Launch Yet: CEO Reveals Game-Changing Investment Product

5 months ago

Musaffa Fintech

YouTube

Halal Investing 101 with Nisba

7 months ago

Musaffa Fintech

YouTube

How to Start Halal Investing | Live Q&A with Mufti Faraz Adam & Musaffa CEO

8 months ago

Musaffa Fintech

YouTube

Investing with Barakah – A Guide to Ethical Wealth Building with Yasmeen Khan

9 months ago

Musaffa Fintech

YouTube

Zakat Workshop with Sheikh Ibraheem Ahmad from Musaffa Academy

11 months ago

Musaffa Fintech

YouTube

Musaffa: Office Hours with David Meltzer

1 year ago

Musaffa Fintech

YouTube

Live Q&A: Last Chance to Invest Before Our Crowdfunding Closes. November 6th, 2024

1 year ago

Musaffa Fintech

YouTube

Introducing Musaffa's All-New Website and Revolutionary Halal Trading Functionality

1 year ago

Musaffa Fintech

YouTube

Invest in Musaffa and Own a Part of a Leading US-based Islamic Fintech Company!

1 year ago

Musaffa Fintech

YouTube

How-To Videos

Not All “Halal Stocks” Are 100% Halal — Here’s What You Need to Know

9 months ago

Musaffa Fintech

YouTube

Discover How to Find the Right Halal ETFs with Musaffa!

10 months ago

Musaffa Fintech

YouTube

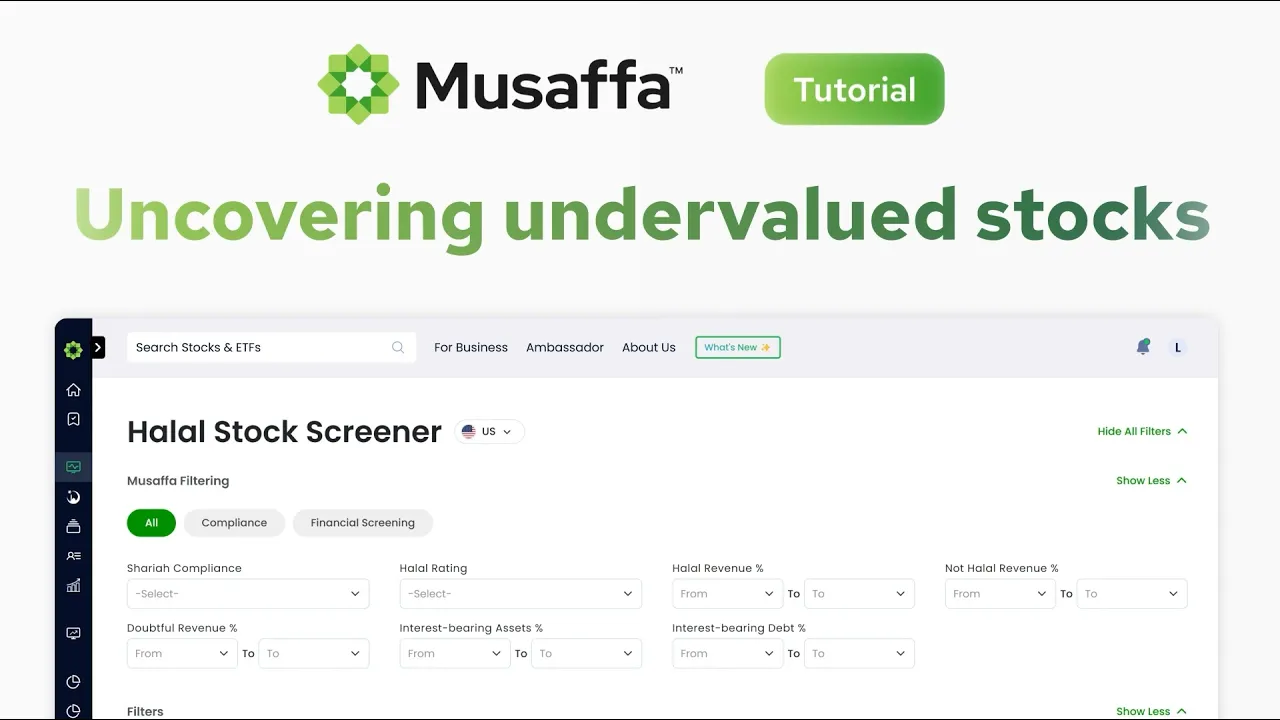

How to Find Undervalued Stocks with the Halal Stock Screener

11 months ago

Musaffa Fintech

YouTube

How to Find Stable & Halal Healthcare Stocks | Halal Investing with Musaffa

11 months ago

Musaffa Fintech

YouTube

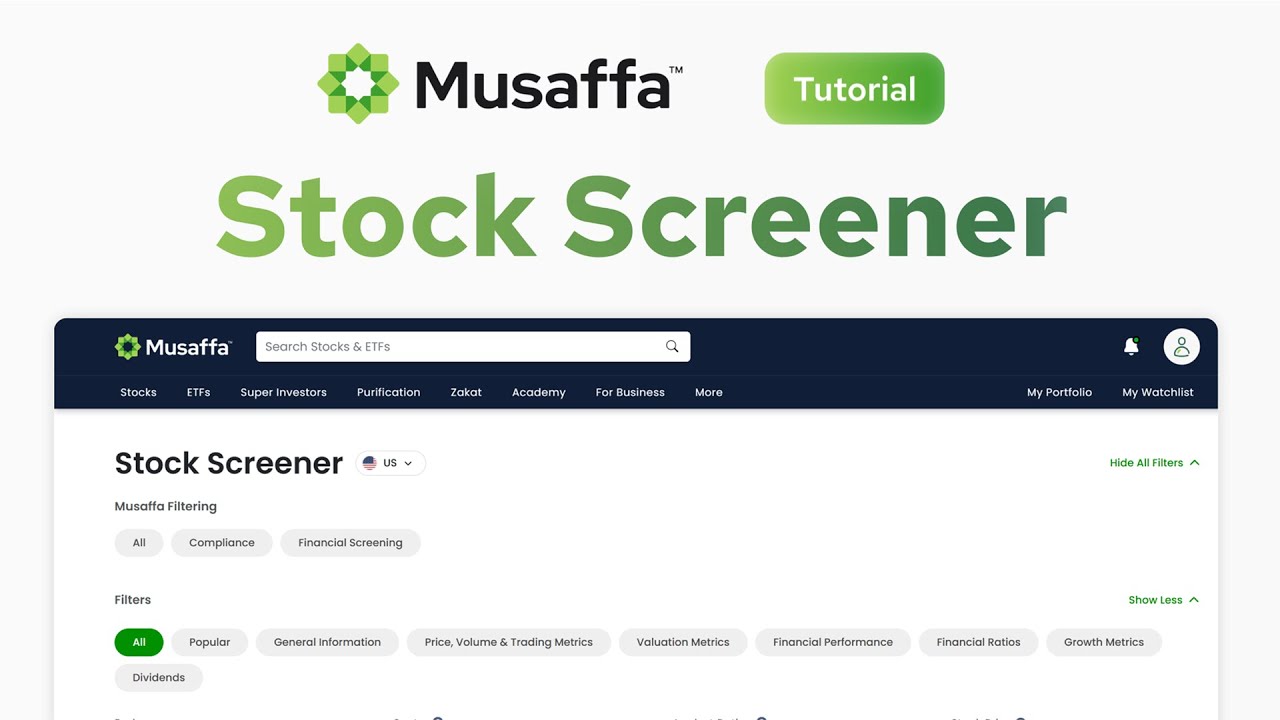

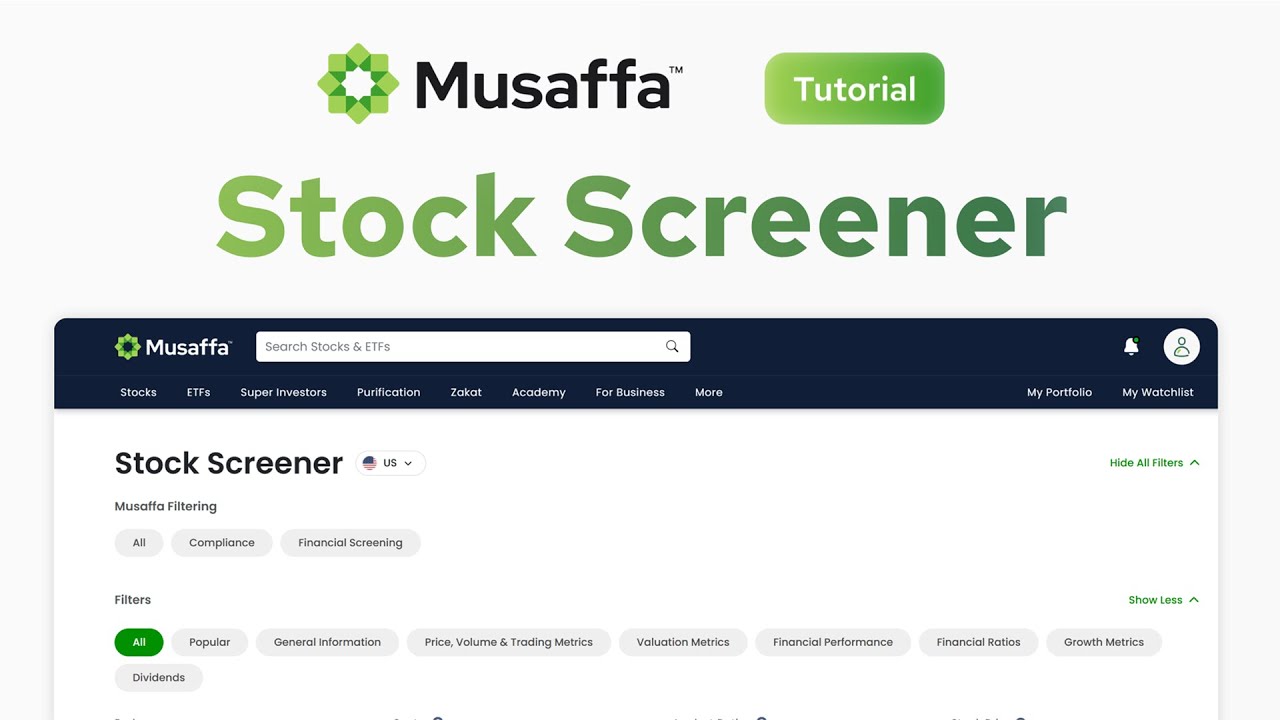

How to Use Musaffa’s Halal Stock Screener | Find Shariah-Compliant Stocks That Match Your Strategy

11 months ago

Musaffa Fintech

YouTube

How to Calculate Your Zakat with Musaffa | Step-by-Step Guide Using Our Zakat Calculator

11 months ago

Musaffa Fintech

YouTube

How Does Musaffa's Halal Rating Work?

11 months ago

Musaffa Fintech

YouTube

Simplify Your Zakat Calculation with Musaffa!

11 months ago

Musaffa Fintech

YouTube

How to Find Undervalued Stocks with the Halal Stock Screener

1 year ago

Musaffa Fintech

YouTube

How to Find Stable Healthcare Stocks with the Halal Stock Screener

1 year ago

Musaffa Fintech

YouTube

How to Use the Halal Stock Screener: A Step-by-Step Guide

1 year ago

Musaffa Fintech

YouTube

How to Use Musaffa's Halal Stock Screening System | Filter Stocks the Right Way!

1 year ago

Musaffa Fintech

YouTube

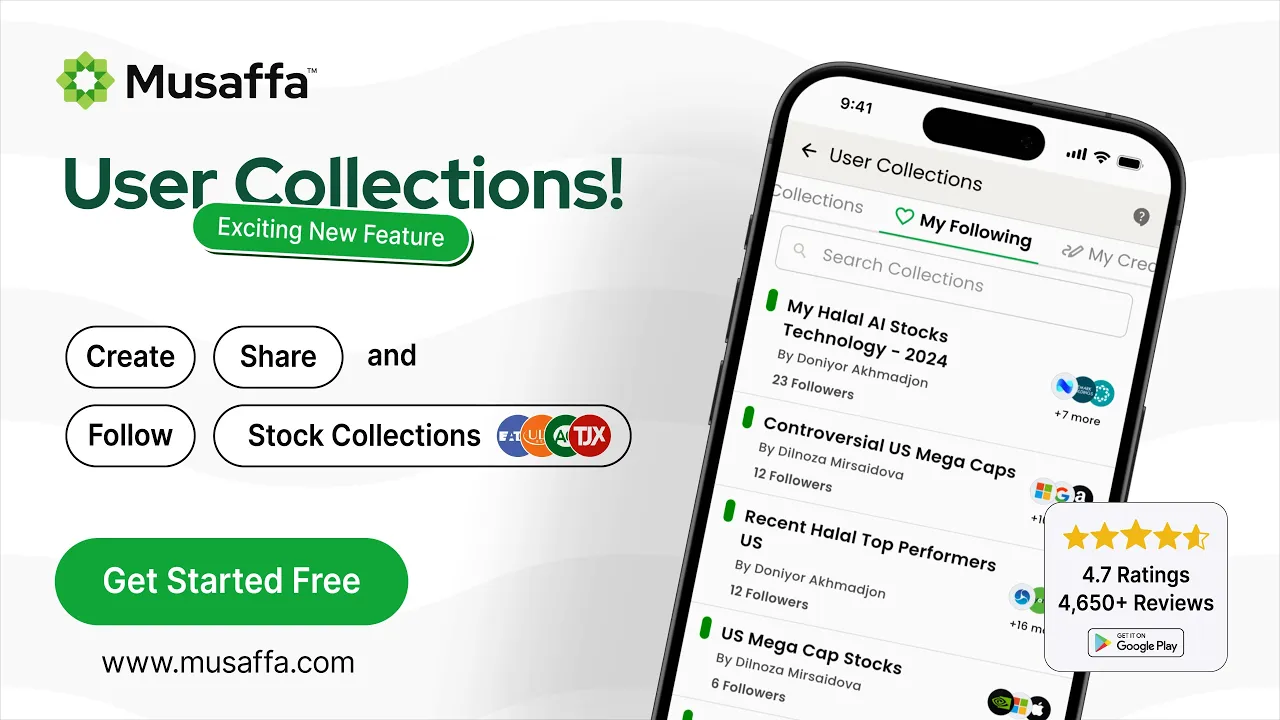

User Collection Feature - #musaffa

1 year ago

Musaffa Fintech

YouTube

7 Features of Musaffa Premium plan

4 year ago

Musaffa Fintech

YouTube

Musaffa Academy Articles

THE BARAKAH BRIEF

Your Daily Dose of Halal Wealth Wisdom

Join 100,000+ readers for bite-sized, faith-aligned financial insights

Frequently Asked Questions

What is Musaffa Academy?

Musaffa Academy is an online learning platform that teaches you how to invest in a halal, ethical, and confident way — from the basics to more advanced topics.

Do I need to know anything about investing before I start?

No! Our beginner courses teach you everything from the basics.

Will I get a certificate after finishing a course?

Yes! Many courses include a Musaffa Academy certificate you can download and share.

How long do the courses take?

Most courses are short and self-paced, so you can learn anytime that works for you.

Can I ask questions to scholars or analysts?

Yes! You can ask our scholars, analysts, or use Ask AI for quick help.

Are the courses free?

Many courses are free. Some advanced content is included with specific membership plans.

When will I get my investment back?

Invest in startups to promote new businesses, to prevent monopolies, and to create competition within the global markets.

Is halal investing only for Muslims?

No! Anyone who wants ethical investing can benefit from it.

How often do you add new lessons or videos?

We add new courses, articles, and webinars regularly.

Will these courses help me start investing?

Yes! They give you the knowledge and confidence to begin investing the right way.