Company overview

When evaluating software stocks, Adobe is a software firm that prioritizes digital consumer experiences, productivity, and creativity. Its primary source of income is subscription fees, which provide a consistent, recurring revenue stream. The most significant aspect of the narrative at this point is how successfully Adobe is converting its AI drive into actual revenue growth while maintaining high profit margins.

What’s driving the story right now

On the surface, Adobe's Q1 results looked good. Subscription revenue remained robust, revenue and non-GAAP EPS exceeded projections, and AI-first ARR more than quadrupled from the previous year. This indicates to investors that the business is continuing to expand and that the market for its AI-related goods is improving.

However, the market's response indicates that a strong quarter is not the whole picture. Additionally, Adobe released a Q2 forecast that appears strong but falls short of expectations, and management announced that longtime CEO Shantanu Narayen will step down as soon as a replacement is selected. Therefore, the market is now more concerned with whether Adobe's AI momentum can remain strong enough to sustain the next phase of development than with whether the company had a successful quarter.

Financial story

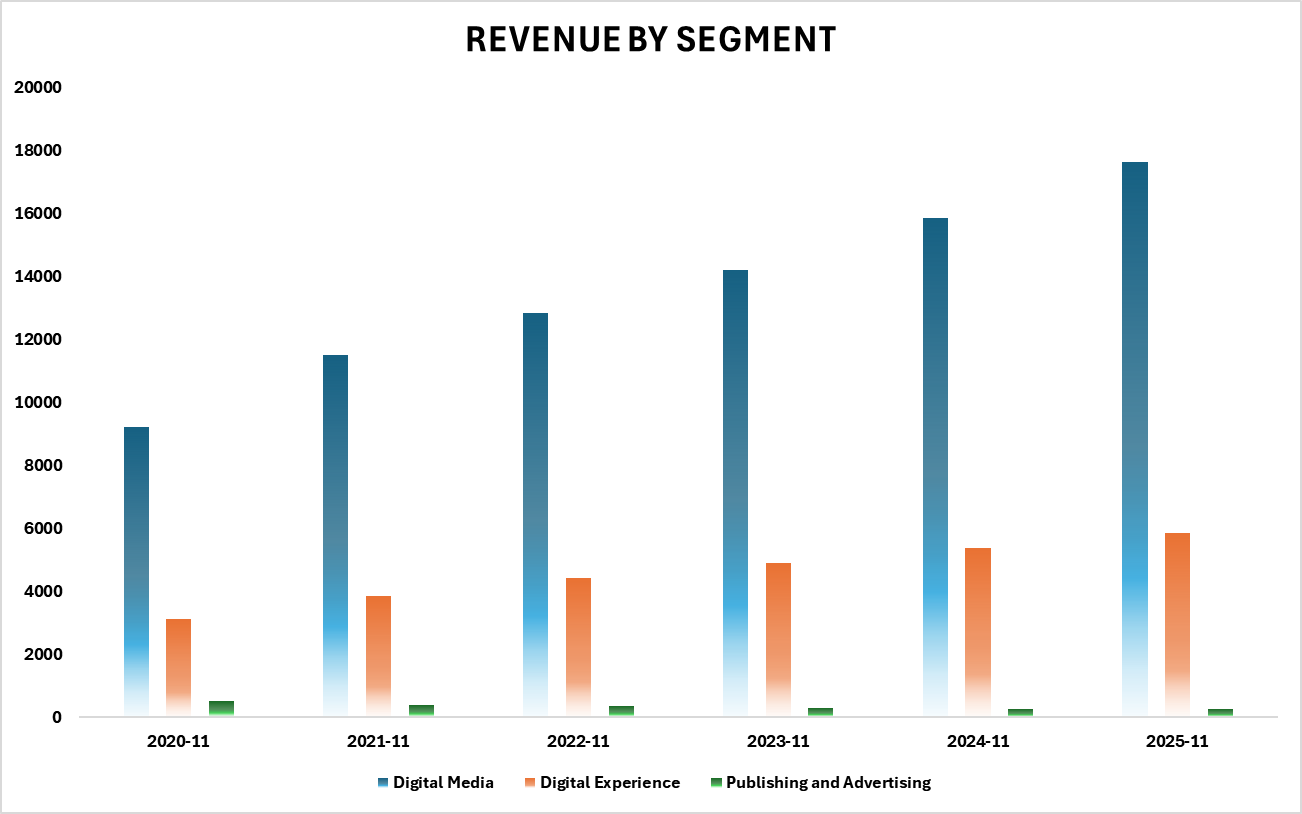

Detailing Adobe Q1 results, Adobe reported $6.40 billion in sales for the first quarter, a 12% increase over the same period last year. With subscription revenue accounting for $6.198 billion of total revenue, the company remains primarily subscription-driven. This is significant since recurring subscription revenues often increase the company's predictability and provide investors with greater insight into future performance.

Growth across the company was broad enough to sustain the quarter. Subscription income for the whole Customer Group increased by 13% to $6.17 billion. Creative & Marketing Professionals rose 12% to $4.39 billion, while Business Professionals & Consumers expanded 16% to $1.78 billion. Simply put, Adobe continues to expand both its core professional clientele and its broader user base, which is significant because it shows that demand is not dependent on a single, small segment of the company.

Additionally, profitability remained high. Operating income was $2.42 billion under GAAP and $3.04 billion under non-GAAP. While non-GAAP net income was $2.49 billion, GAAP net income was $1.89 billion. Additionally, Adobe generated a record $2.96 billion in operating cash flow during the quarter, indicating that the firm is translating its operations into cash in addition to reporting profitability.

Adobe's recurring revenue base was another significant component of the quarter. RPO was $22.22 billion, and total Adobe ARR ended the quarter at $26.06 billion. These numbers are important because they show how much money is already in the system. The financial tale, when combined with the company's statement that AI-first ARR more than tripled year over year, indicates a company that is still growing but that investors now anticipate will demonstrate AI's ability to become a significant and long-lasting earnings generator.

Quarter check

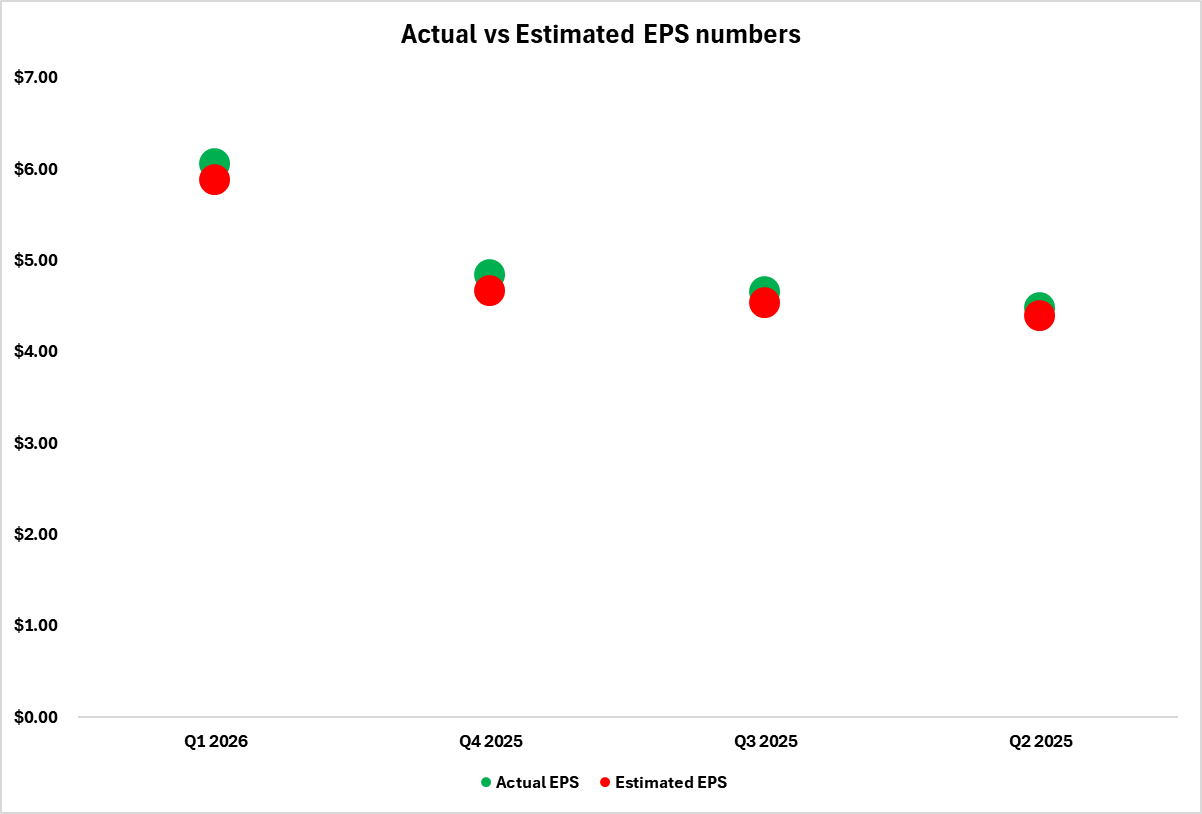

In the latest ADBE earnings, Adobe announced non-GAAP EPS of $6.06 compared to the estimate of $5.88 and Q1 revenue of $6.40 billion compared to the consensus of $6.28 billion. That clearly outperforms the company's top line and the primary earnings indicator the market is most interested in.

However, the stock does not always rise after a beat. The market seems to be looking beyond the quarter in Adobe's instance. Investors appear to be more interested in how much AI can contribute to future development, whether the near-term forecast is solid enough to raise expectations even more, and the potential long-term effects of the CEO change.

Outlook/guidance

Shaping the ADBE stock forecast, Adobe estimates $6.43 billion to $6.48 billion in sales, $5.80 to $5.85 in non-GAAP EPS, and $4.35 to $4.40 in GAAP EPS for the second quarter of FY2026. Additionally, a non-GAAP operating margin of roughly 44.5% is assumed in the Q2 objective.

Management is targeting non-GAAP EPS of $23.30 to $23.50 and sales of $25.9 billion to $26.1 billion for the full year. Additionally, it anticipates a non-GAAP operating margin of roughly 45% and a total Adobe ARR growth of roughly 10.2%. To put it simply, Adobe is informing investors that while it is currently investing to support its AI effort, they should anticipate ongoing growth and solid profitability. That is why the key question is not whether the business is growing, but whether AI-related investment can lead to even stronger monetization over time.

Price and valuation context

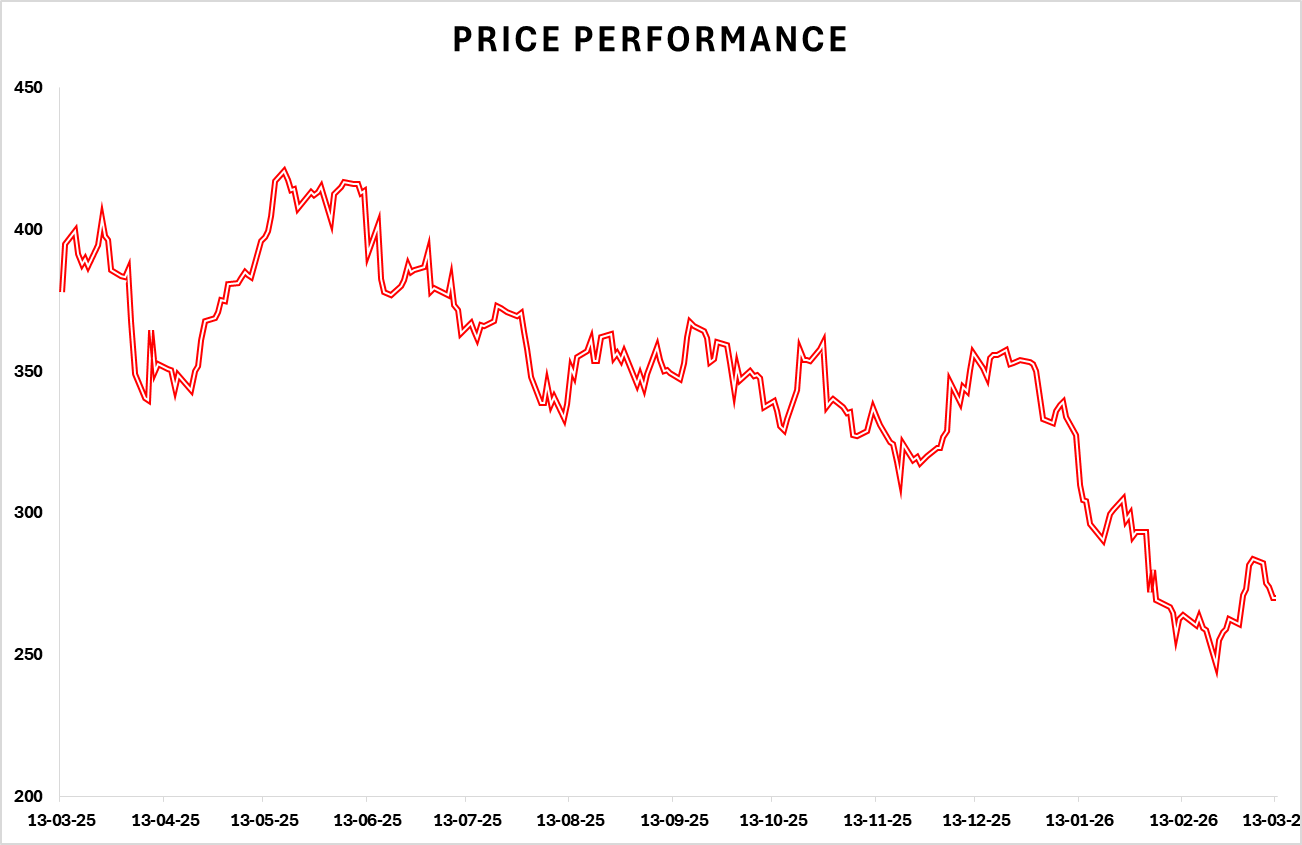

Adobe ended the day at $269.78. The stock was up 1.93% over a month, but it was down 1.44% on the day and 4.25% over five days. The situation is worse over a longer time frame: the stock has gone down 19.06% so far this year and 21.65% over the last three months. Additionally, it remains well below its 52-week high of $422.95 and slightly above its 52-week low of $244.28.

Around the outcomes, trading activity increased. Compared to a 20-day average of 5.18 million shares, volume was 7.69 million, indicating that investors were aggressively reevaluating the story following earnings.

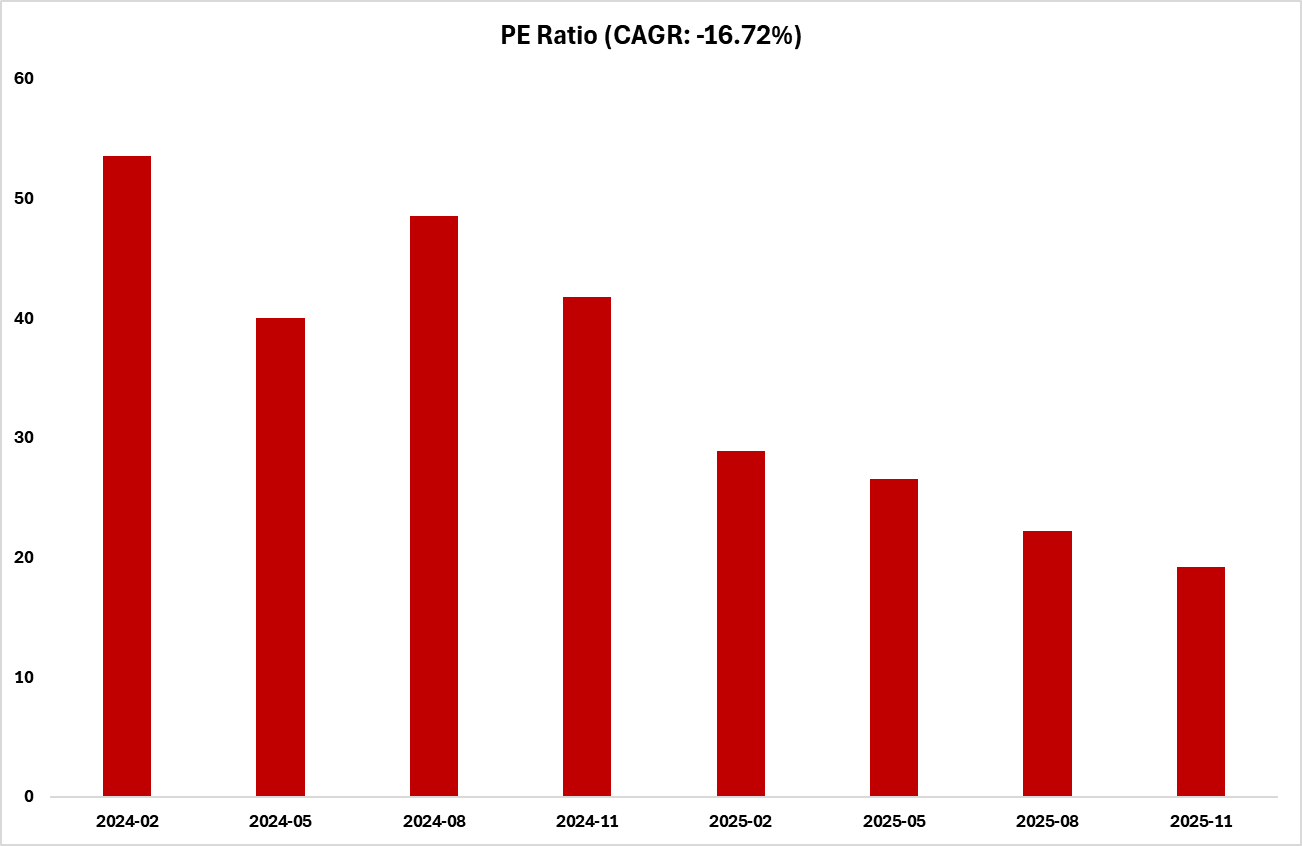

Adobe is valued at 16.13x trailing profits and 11.63x forward earnings, with EV/Sales at 4.43x and EV/EBITDA at 11.40x. The fact that the forward multiple is less than the trailing multiple indicates that the market is still anticipating future earnings growth. With an enterprise value of $111.63 billion and nearly neutral net debt of $0.04 billion, the balance sheet snapshot is generally reasonable. Overall, assuming Adobe can continue to develop, the valuation does not appear stretched, but it also suggests the market is looking for more convincing evidence that AI can drive greater future upside.

Risks

Regarding ADOBE AI monetization, the greatest concern is that Adobe's AI momentum might not generate sufficient revenue to meet market demand. The company is investing in AI infrastructure, which could put pressure on margins if growth does not pick up enough speed to cover that expenditure. The upcoming CEO change carries execution risk as well, particularly as Adobe is attempting to demonstrate a significant new growth story at the same time. Additionally, investors may be less inclined to pay even today's lower value multiples if enterprise clients grow more wary or if competition in creative and productivity software intensifies.

Shariah Compliance

For investors reviewing Shariah-compliant stocks, ADBE, as of January 2026, Adobe (ADBE) is classified as Shariah-compliant (Halal) with an A- Musaffa rating based on the Shariah Screening results at Musaffa. ADBE’s 2025 Annual Report was used to conduct the screening analysis in line with the AAOIFI methodology. ADBE passed all three required screening thresholds, with 98.42% of its business activity meeting the permissible (Halal) threshold (0.00% doubtful and 1.58% not Halal). Both interest-bearing securities (3.40%) and interest-bearing debt (3.07%) remain below 30% of the 36-month average market capitalization.

Conclusion

Adobe had a successful quarter. Cash flow was excellent, revenue and earnings above expectations, and the enthusiasm surrounding AI is still growing. However, it is evident that the market is requesting many reliable reports. Whether Adobe can continue to turn its AI drive into growth significant enough to alter the stock's longer-term trajectory is now the crucial question.

Sources

- Adobe Inc. Stock Analysis

- Adobe Inc

- Adobe Inc Stock News from GuruFocus

- Adobe Delivers Record Q1 Results

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed