Company overview

Amphenol is a worldwide provider of specialized cable, antennas, sensors, interconnect systems, and electronic connectors. To put it simply, it provides the components that enable electronic systems across a variety of sectors to connect, transmit data, and operate reliably. The most significant aspect of the narrative at the moment is that Amphenol is benefiting from broad-based demand across a variety of end markets, particularly in the IT and communications sectors, while simultaneously generating new growth through acquisitions.

What’s driving the story right now

The story of Amphenol is mostly driven by widespread demand. Strong performance in almost every end market contributed to Q4 growth, according to management, with particularly strong organic growth in IT datacom demand.. This is significant because it implies that the business is not dependent on a single, limited range of products or a single, transient subject. It is expanding across a wide range of clients.

Acquisitions are the second main motivator. Amphenol completed the Amphenol CCS acquisition in January 2026, following five acquisitions in 2025. The purchase is significant because management anticipates that CCS will increase sales by approximately $4.1 billion and adjusted EPS by around $0.15 in 2026. To put it another way, the business is not simply expanding naturally. Additionally, it is strengthening its position in important areas and broadening its revenue base through acquisitions.

Financial story

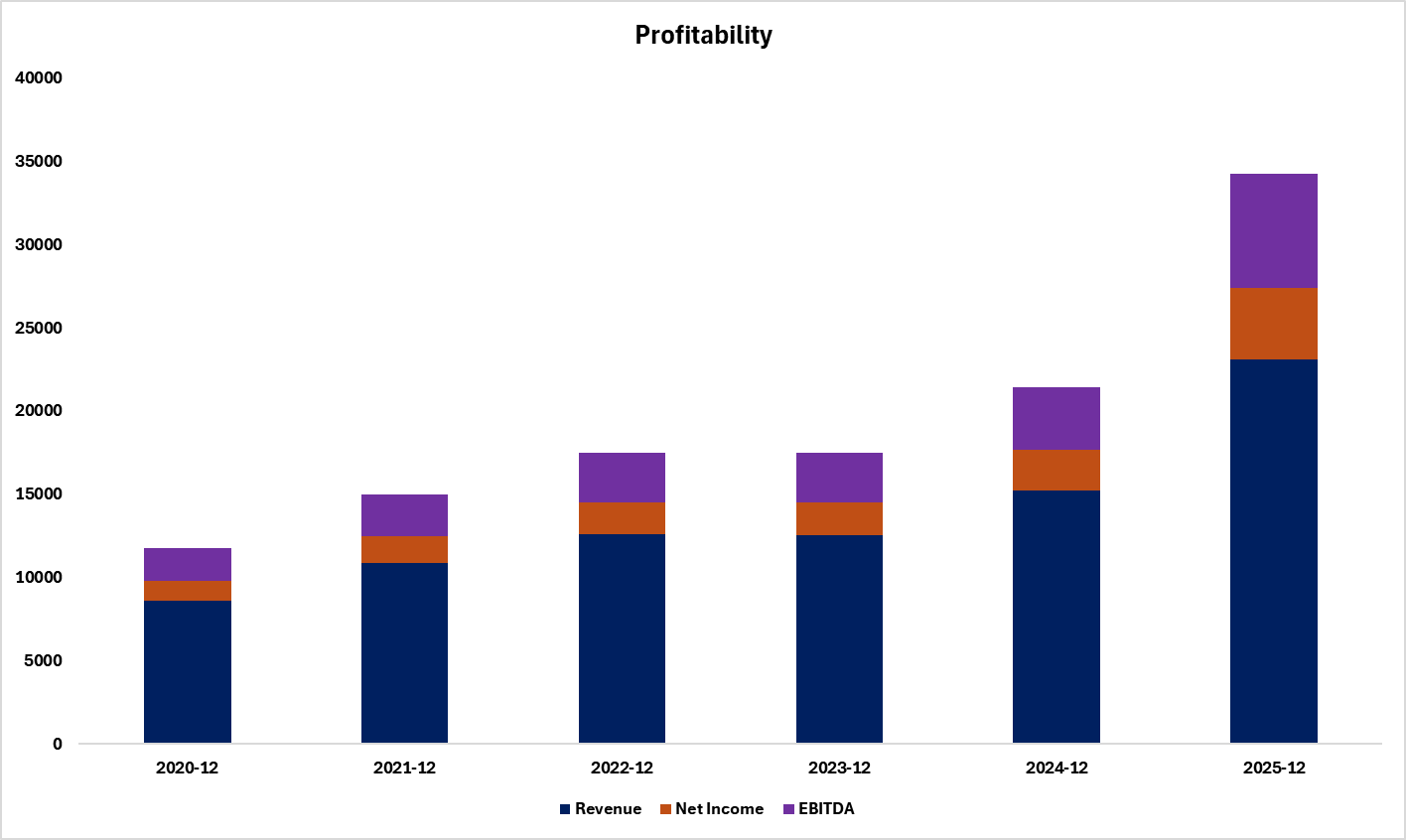

Amphenol reported $6.44 billion in revenue for the fourth quarter, up 49% from the same period last year, with 37% organic growth. That is a crucial distinction for novice investors. Acquisitions are included in reported growth, whereas organic growth reflects the underlying business's expansion. A 37% organic growth is still rather impressive and indicates that the company had significant momentum prior to the addition of acquisition advantages.

Additionally, profitability remained high. The adjusted operating margin for the fourth quarter was 27.5%, while the GAAP operating margin was 26.8%. Free cash flow was $1.5 billion, while operating cash flow was $1.7 billion. Thus, Amphenol's revenue growth was not only rapid. Additionally, it converted a significant portion of those sales into cash while maintaining good margins.

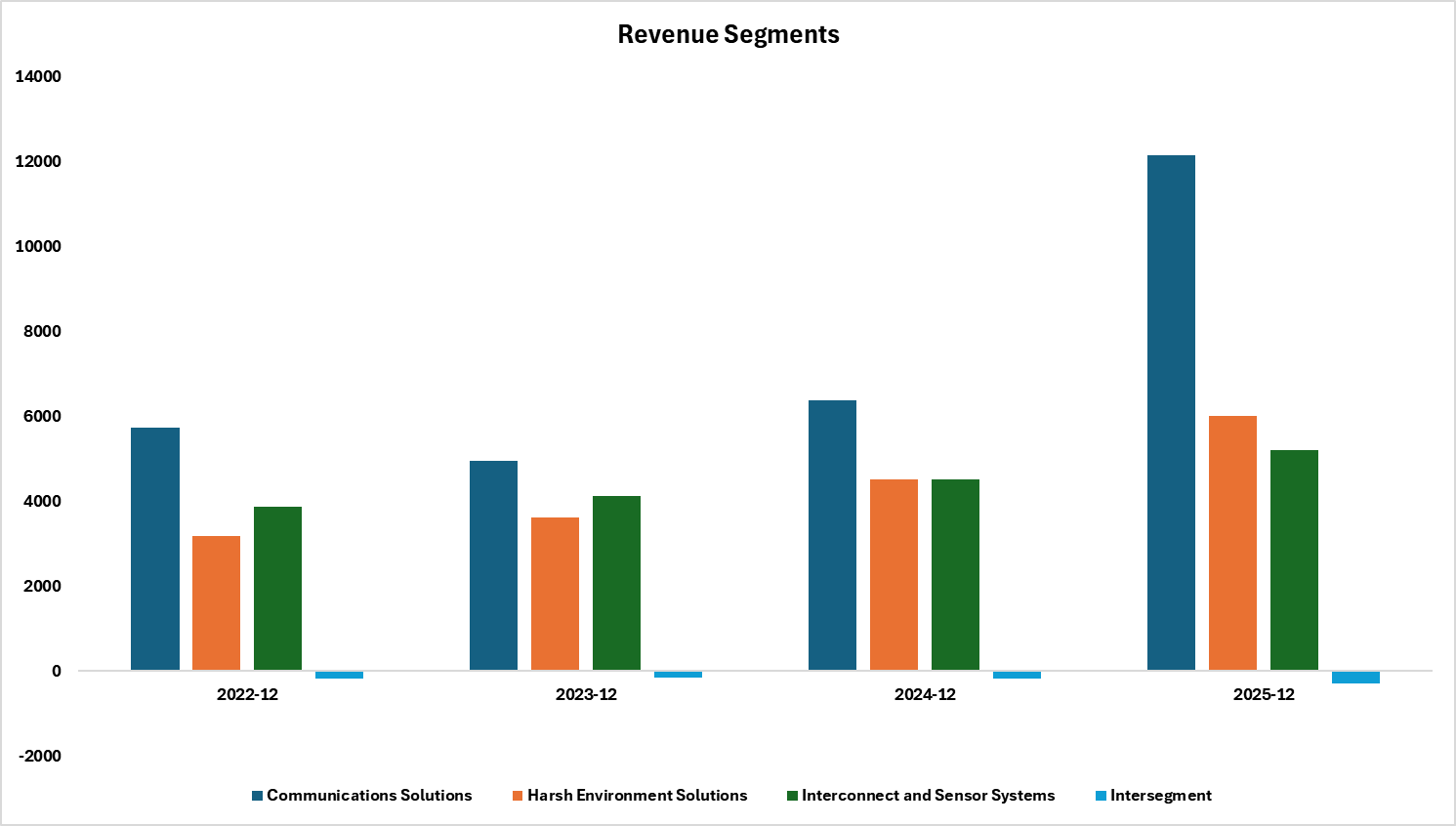

The section breakdown clarifies the source of the strength. With $3.42 billion in revenue and an operating margin of 32.5%, Communications Solutions was the biggest company during the quarter. Interconnect and Sensor Systems provided $1.36 billion with a 20.1% operating margin, while Harsh Environment Solutions brought in $1.65 billion with a 27.6% operating margin. It is evident that communications solutions remain the largest source of earnings, consistent with management's remarks on the high demand for IT datacom.

Furthermore, the full-year outlook is promising. In 2025, Amphenol reported $23.1 billion in revenue, a 52% increase over the previous year. Operating cash flow for the entire year was $5.4 billion, free cash flow was $4.4 billion, and the adjusted operating margin was 26.2%. This type of cash flow allows the business to continue making growth investments, pursuing acquisitions, and returning capital to shareholders.

Read More:

- The Rise of DoorDash: Q4 Results, Expansion, And Challenges

- Moody’s 2026 Guidance Highlights AI Tailwinds—and the Real-Time Credit Cycle

- EQIX Q4 Earnings: Revenue, EBITDA Beat? AI Hyperscale & 2026 Outlook

Quarter check

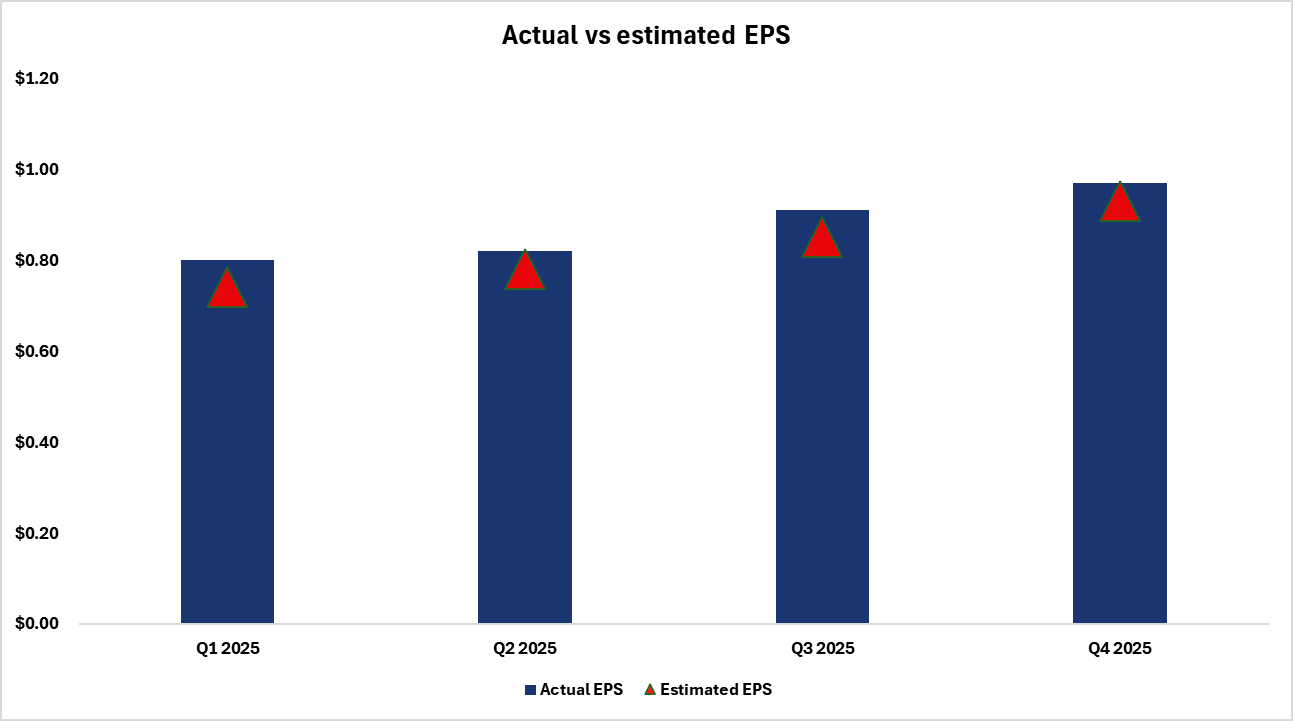

Amphenol reported adjusted EPS of $0.97 compared to the expectation of $0.93 and Q4 sales of $6.44 billion compared to the consensus of $6.19 billion. Both sales and profitability have increased.

What matters more is that the beat was accompanied by healthy margins and extremely strong organic growth. Because of this, the quarter feels more resilient than a result that is solely influenced by one-time events. The arrangement implies that the market views Amphenol as a business with both strong demand and strong performance, rather than merely benefiting from acquisitions.

Outlook

Amphenol projects $6.90 billion to $7.00 billion in sales and $0.91 to $0.93 in adjusted EPS for the first quarter of 2026. The target range for GAAP EPS is $0.81 to $0.83. Additionally, management stated that the CCS business generates around $900 million in sales and $0.02 in adjusted EPS.

Put simply, management is aiming for another quarter of robust year-over-year growth while beginning to factor in the effects of its most recent significant purchase. The important thing to remember is that the corporation is starting 2026 with both underlying momentum and an additional contribution from CCS.

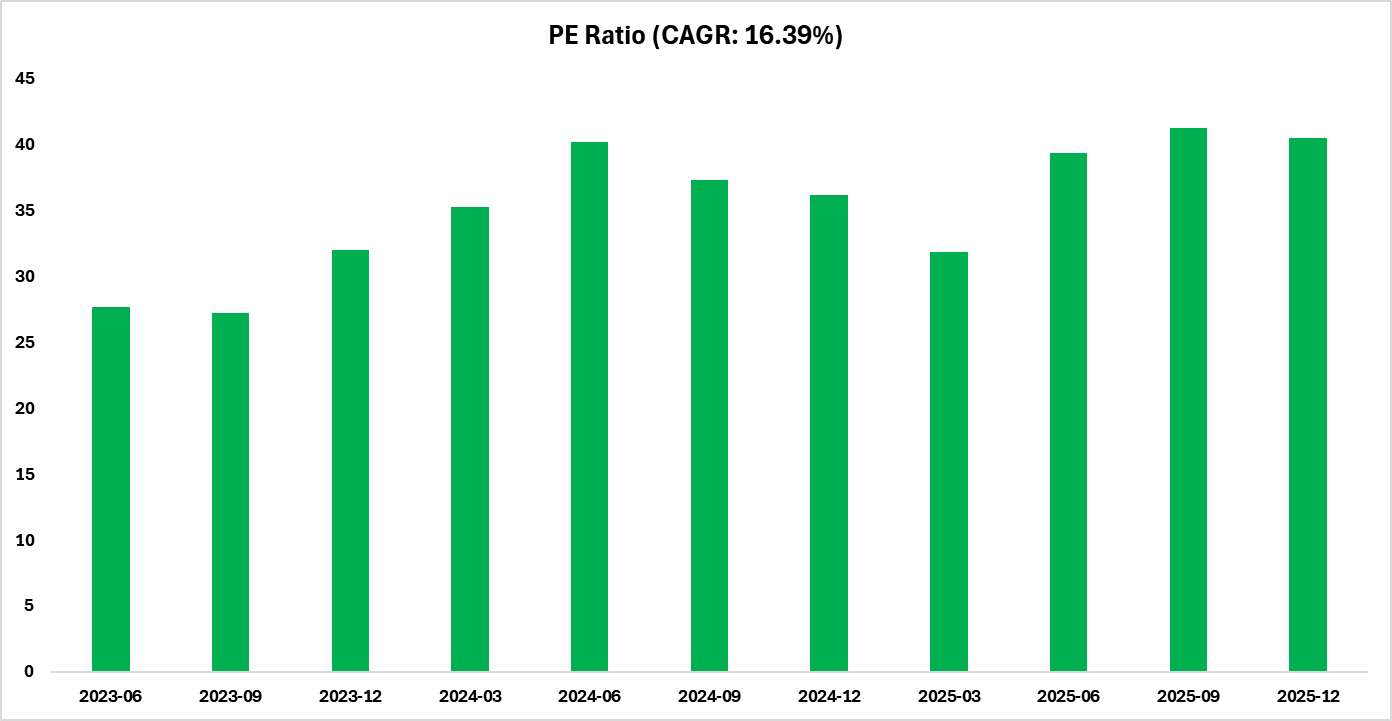

Price and valuation context

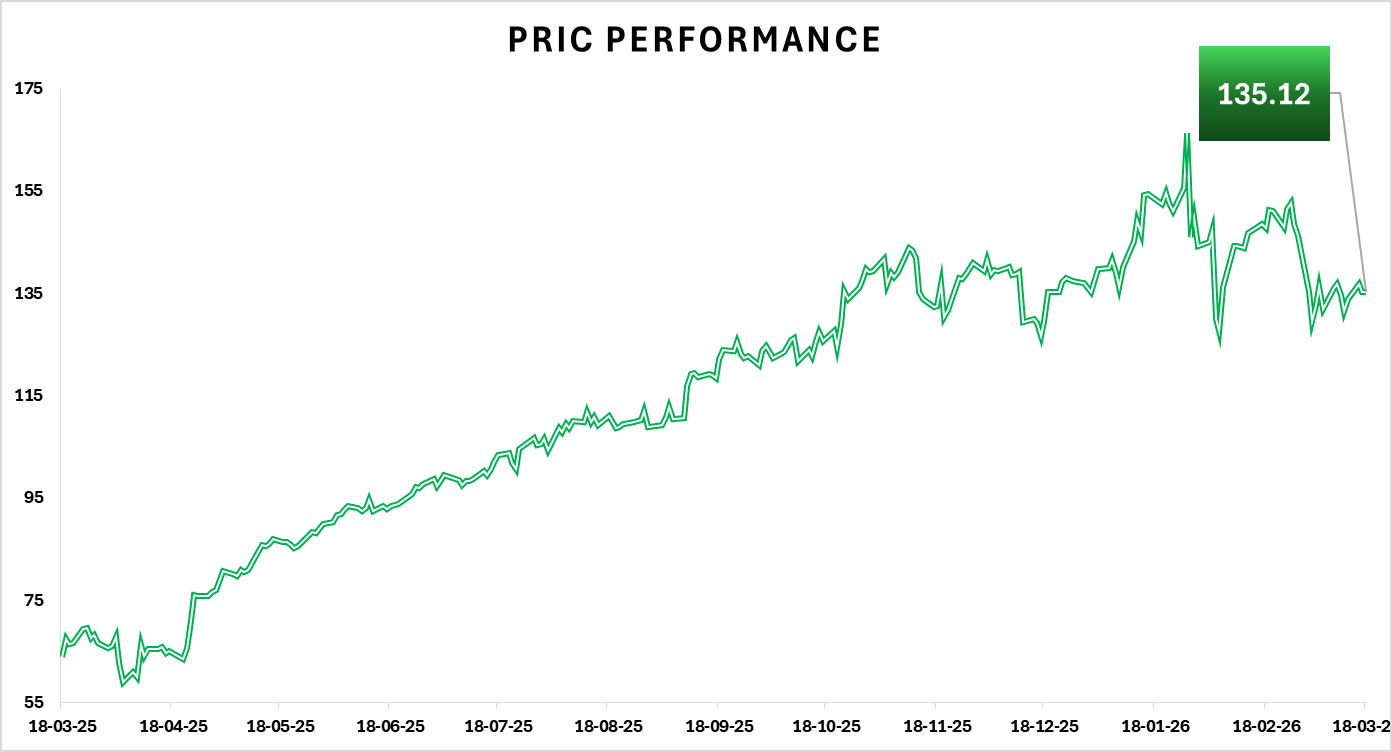

Amphenol stock ended the day at $135.12. The stock saw daily losses of 1.23%, five-day losses of 1.18%, and monthly losses of 7.91%. Although it was down 3.29% year to date, it was still up 4.55% over a longer time frame. Therefore, the operating performance appears more robust than the recent price movement.

The shares are still well above the 52-week low of $56.45 but below the 52-week high of $167.04. Additionally, the volume of 12.69 million was higher than the 20-day average of around 9.86 million, indicating that the stock has been actively traded during this recent decline.

Amphenol is valued at 40.46x trailing earnings and 26.31x projected earnings, with P/FCF at 37.94x and EV/Sales at 7.40x. On straightforward headline multiples, that stock is not inexpensive. The lower forward P/E indicates that investors are already paying for a high-quality company, but it also indicates that the market still anticipates future profit growth. The picture appears to be controllable rather than net cash positive on the balance sheet. Your estimated net debt of approximately $4.37 billion is consistent with the filing's total cash, cash equivalents, and short-term investments of around $11.43 billion versus approximately $15.50 billion in debt.

Risks

The most significant risk is that, although diversified across several sectors, Amphenol remains dependent on end-market demand cycles. Growth may decelerate from its current extremely high level if consumers in the communications, industrial, aerospace, and other industries reduce their expenditure. Additionally, there is acquisition risk, particularly for a company like Amphenol that actively purchases and integrates new businesses. Furthermore, the corporation itself identifies risks related to export restrictions, tariffs, raw material costs, cybersecurity, the state of the global economy, and the difficulty of sustaining growth and profit margins across its broad worldwide presence.

Shariah Compliance Lens

As of February 2026, Amphenol (APH) is classified as Shariah-compliant (Halal) with a C+ Musaffa rating based on the Shariah Screening results at Musaffa. APH’s 2025 Annual Report was used to conduct the screening analysis in line with the AAOIFI methodology. APH passed all three required screening thresholds, with 98.71% of its business activity meeting the permissible (Halal) threshold (0.00% doubtful and 1.29% not Halal). Both interest-bearing securities and assets (13.18%) and interest-bearing debt (17.86%) remain below 30% of the 36-month average market capitalization.

Conclusion

Amphenol had an excellent quarter. Earnings exceeded revenue; organic growth was remarkable; and cash creation remained robust. In 2026, the corporation will experience additional growth thanks to the CCS transaction. Whether Amphenol can continue to translate this broad demand strength and acquisition momentum into steady profit growth sufficient to justify its premium value is now the crucial question.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed

Musaffa Marketing

Musaffa Marketing