Company overview

Broadcom is a technology company specializing in infrastructure software and chips. Infrastructure software accounted for $6.796 billion (35% of revenue) in the most recent quarter, while semiconductors accounted for $12.515 billion (65% of revenue). This balance is important because the demand for AI is most evident in the semiconductor industry.

What’s driving the story right now

Whether Broadcom can continue to ride the AI buildout is the market's main concern regarding Broadcom stock. AI chip revenue is expected to increase to $10.7 billion in Q2, according to management, which highlighted Q1 AI revenue of $8.4 billion driven by Broadcom AI chips. The stock responds to the prognosis, not simply the reported quarter, mostly because of that anticipated step-up. Capital return is another motivator; management approved a fresh $10 billion share repurchase program, indicating a persistent focus on shareholder returns.

Financial analysis

Highlighting the Broadcom Q1 results, revenue increased 29.5% year over year to $19.31 billion. Infrastructure software contributed $6.8B (35%) and grew 1%, indicating that the chip industry is the primary engine, with semiconductors accounting for $12.5B (65% of revenue) and 52% growth.

Despite the quick expansion, profitability stayed remarkably high. The management anticipates that adjusted EBITDA margins would remain approximately 68%, demonstrating Broadcom's continued strong pricing power, scale benefits, and strict cost control.

In Q1, free cash flow was $8.01 billion, or around 41% of revenue. Without primarily relying on new debt, this robust cash conversion offers flexibility to support shareholder returns, fund growth, and fund operations.

Broadcom approved a fresh $10 billion share repurchase program. Buybacks boost per-share performance and demonstrate management's faith in the company's ability to generate cash going forward, even while they do not replace growth.

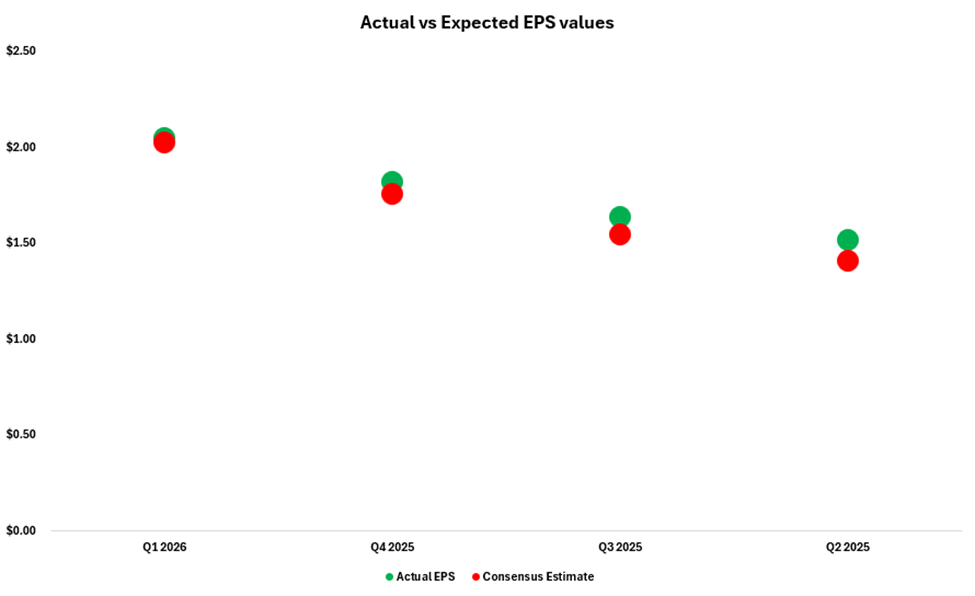

Quarter check

Revenue: $19.31B vs $19.10B expected (beat; +29.5% YoY).

Non-GAAP EPS: $2.05 vs $2.03 expected (beat; +$0.02 surprise).

The stock frequently responds more to the "beat vs. expected" and the next-quarter projection than to the raw data alone when a firm is priced for rapid development. The market's focus inevitably shifts to whether the upcoming quarter shows AI momentum is still increasing, given that this beat was small.

Outlook

Management guided Q2 revenue to nearly $22.0 billion, up from the anticipated $20.4 billion, indicating a 47% year-over-year increase. Additionally, they anticipate continued strong profitability, with adjusted EBITDA remaining close to 68% of revenue. They anticipate $10.7 billion in AI semiconductor sales in Q2, up from $8.4 billion in Q1. Investors want to see that AI-driven growth is not just robust but continues to accelerate, which is the primary short-term stimulus.

Read More:

- The Rise of DoorDash: Q4 Results, Expansion, And Challenges

- Moody’s 2026 Guidance Highlights AI Tailwinds—and the Real-Time Credit Cycle

- EQIX Q4 Earnings: Revenue, EBITDA Beat? AI Hyperscale & 2026 Outlook

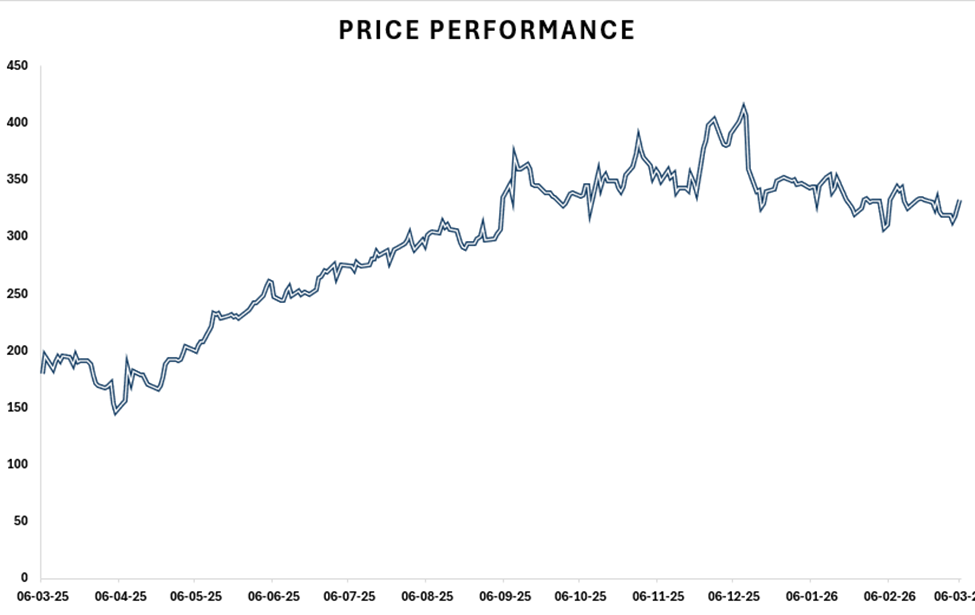

Price and valuation context

Price and value context (including the balance sheet context)

The stock closed at $317.53 on March 4, 2026. With a 52-week range of $138.10 to $414.61, recent performance indicates pressure over longer time periods: 3-month performance is -16.67%, and YTD is -8.25%.

The valuation is still high: trailing P/E is 66.7x, forward P/E is 59.0x, EV/Sales is 23.1x, EV/EBITDA is 44.4x, and P/FCF is 57.7x. In other words, the market continues to pay a premium for growth connected to AI and anticipates that Broadcom will continue to deliver.

Based on $16.18 billion in cash and $65.14 billion in total debt, the company's net debt position on the balance sheet is around $48.96 billion. When cash flow is robust, leverage is manageable, but if growth slows or the cycle weakens, it may become more significant. The company's cash flow lessens this worry, and buybacks - including the recently authorized $10 billion - can eventually boost per-share performance.

Risks

The largest danger is that there isn't much space for disappointment in the current pricing. Even if the company is doing well, the stock may decline if AI expenditure stops, customer orders change, or AI semiconductor growth falls short of projections, because investors may pay a lower multiple. Another risk is that the company's growth narrative is closely linked to AI; if attitudes toward AI infrastructure decline, the price may fluctuate more than the fundamentals would support. Leverage is another important factor to consider: even for a strong cash producer, a net-debt position might limit flexibility during a downturn.

Shariah Compliance

For investors reviewing Shariah compliant stocks AVGO, according to the Shariah Screening findings of Musaffa, Broadcom (AVGO) has an A-Musaffa grade as of December 2025 and is categorized as Shariah-compliant (Halal). The screening analysis was conducted in accordance with the AAOIFI methodology, using AVGO's 2025 Annual Report. With 99.14% of its commercial activity reaching the permitted (Halal) criterion (0.00% uncertain and 0.86% not Halal), AVGO cleared all three necessary screening requirements. Interest-bearing debt (8.57%) and securities and assets (2.13%) both stay below 30% of the 36-month average market capitalization.

Conclusion

With sales forecast to reach around $22.0 billion and AI semiconductor revenue predicted to increase to $10.7 billion, Broadcom reported a great Q1 beat and, more significantly, guided to a higher Q2. AI momentum and ongoing margin discipline are obviously linked to the setup. Price is the primary trade-off for investors mapping the AVGO stock forecast; premium multiples indicate that the stock tends to reward sustained growth and penalize even slight slowdowns.

Sources

- Broadcom Inc. Stock Analysis

- Broadcom Inc

- Broadcom Inc Stock News from GuruFocus

- Broadcom Inc. Announces First Quarter Fiscal Year 2026 Financial Results

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed