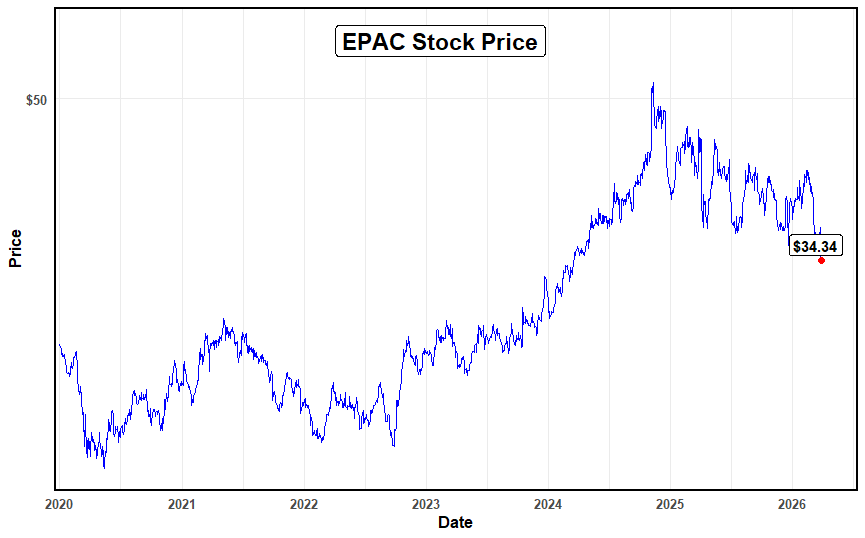

Enerpac Tool Group Corp (EPAC, B+, Halal) is a world leader in high-pressure hydraulic tools, controlled force tools, and heavy-lift solutions. Based in Milwaukee, the company provides tools for the infrastructure, energy, mining, and other industries, helping them efficiently, safely, and accurately move heavy objects. The company’s tools include cylinders, pumps, and bolting tools. The current market value of the company is 2.13 billion, with a current share price of $33.82.

Shariah Status

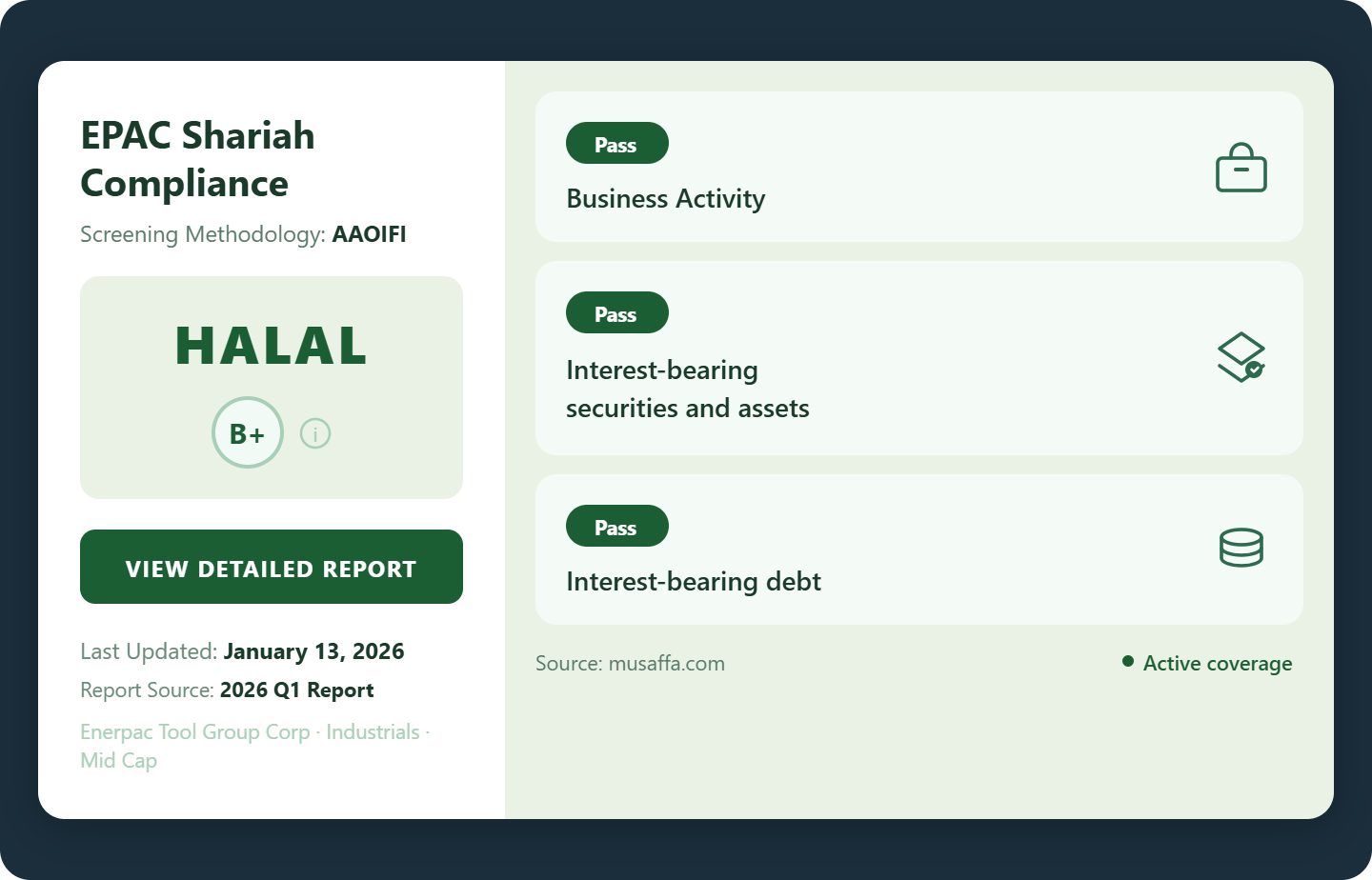

For those evaluating Shariah compliance of EPAC, the status of the company is considered halal, with a ranking of B+ according to the AAOIFI screening methodology by Musaffa. According to the screening results, 98.95% of its business activity is recorded as Shariah-compliant, while 1.05% is not halal due to interest income. Interest-bearing securities and debt account for 7.11% and 9.63% of their assets and liabilities, respectively.

Business analysis

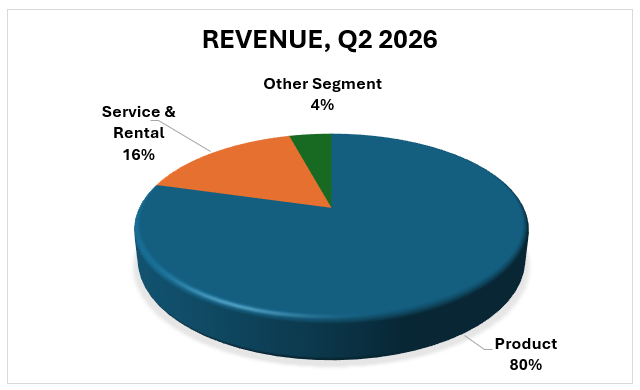

The major factors in the second quarter of fiscal 2026 for the revenue results of Enerpac Tool Group were the divergence in the company's product sales and its international service operations. The Enerpac product revenue of $237,425.00, as represented by year-to-date figures in the table you have provided, received a boost from the 6% organic increase in the second quarter of the year, which was the best product performance in ten quarters. This is attributed to the high demand for the company's products in the infrastructure and power generation industries, especially after the launch of several new 'smart' hydraulic systems at major industrial trade shows.

The Service & Rental revenue of $49,023.00 represents a more challenging period for the company's field operations, which experienced a double-digit decline in the second quarter. The main reason for the decline is the macroeconomic weakness in the EMEA region (Europe, Middle East, and Africa), where major maintenance projects in the oil and gas sector were delayed, and the company had to implement a $3.3 million restructuring plan to right-size its workforce in the region. The Other Segment revenue of $12,567.00, which includes the Cortland Biomedical business, again was a high-growth "bright spot" for the company, growing 27% during the quarter. This was the result of new project wins for specialized medical fibers for advanced surgical techniques, causing this "niche" to outperform the company's overall industrial average.

Financial analysis

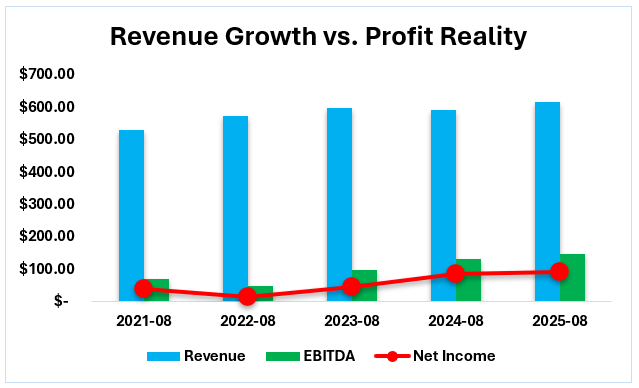

In the fiscal year 2024, the revenue generated by Enerpac Tool Group was recorded at $589.5 million, representing a small reduction from the previous year due to the strategic sales of its Cortland Industrial business. However, the company’s EBITDA increased to $132.3 million due to the "Enerpac ASCEND program" transformation program, which sought to enhance product pricing and reduce operational waste (Enerpac). The program, therefore, led to a huge increase in the company’s net income by 53%, reaching $85.8 million, as the company successfully transitioned into a more profitable "pure-play industrial tool company."

As the company moved into fiscal 2025, it recorded the highest revenue in its history, reaching $616.9 million, representing an increase of 4.6% over the previous year’s revenue. The growth was attributed to the acquisition of DTA, a Spanish company specializing in heavy-load transporters, coupled with a 15% organic growth in the Cortland Biomedical segment (Enerpac). The company, therefore, recorded an increased EBITDA of $146.3 million, driven by the growth in sales volumes across the globe, despite the initial expenses associated with integrating the new businesses into Enerpac Tool Group.

Net income for the year 2025 increased even more, registering $92.8 million, which indicated an improvement of 8.2% over the year 2024. The consistent growth in the bottom line was driven by the company’s ability to sustain high profit margins while venturing into new markets like wind energy and defense. The transition from 2024 to 2025 indicated a clear shift from internal restructuring activities to inorganic growth through smart acquisitions and innovation.

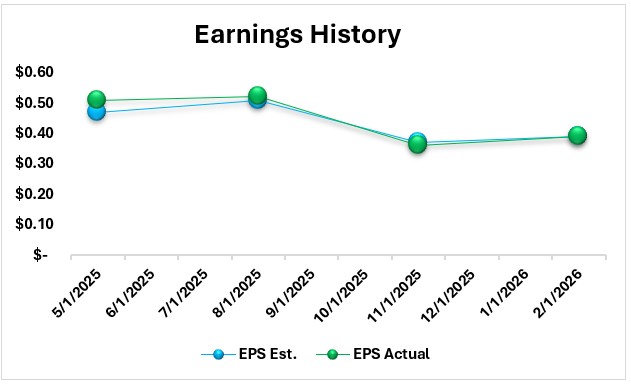

Earnings Analysis

Enerpac also managed to outperform expectations in the second half of its 2025 financial year by surpassing earnings estimates in May and August due to high demand for infrastructure and the successful integration of the DTA acquisition. However, the company has experienced headwinds in its 2026 financial year by failing to meet the November target and only meeting the February target, as the 21% decline in European service revenue outweighed the strong sales of its products. As tool orders have been maintained at record levels, the company has initiated a restructuring plan of $3.3 million to stabilize its profit margins due to delays in international services.

Valuation Analysis

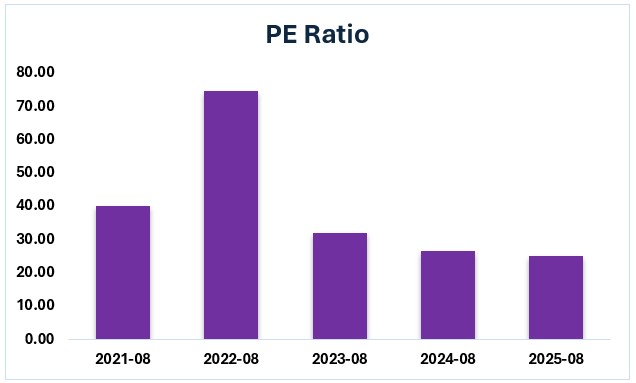

The following chart shows that the P/E ratio of Enerpac has decreased steadily from its peak of 74.6x in August 2022. This was a result of the limited profitability of the company at the time, making the stock expensive relative to its earnings. However, with the introduction of the ASCEND program, the earnings of the company increased in 2023 and 2024. This caused the P/E ratio to fall rapidly to 32x and 26x, respectively. In August 2025, the P/E ratio fell to 25.2x, making the stock more attractive from a general perspective and showing that the company was achieving profitability. Therefore, from the above chart, it is clear that the company has become more stable and attractive from an economic point of view over the past few years.

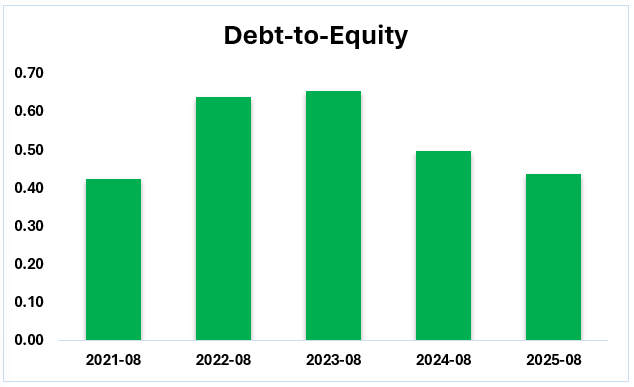

The following table compares the company’s debt levels with its intrinsic value, which demonstrates the company’s journey of taking more risks in the form of debt while expanding its operations and then trying to reduce its debt levels. The debt-to-equity ratio for the company rose from 0.43 in 2021 to 0.66 in 2023 due to the debt levels the company incurred to fund its extensive restructuring under the ASCEND program and to acquire more businesses. However, the debt-to-equity ratio then reduced to 0.50 in 2024 and to 0.44 by August 2025. This demonstrates that the company is using its record profits to pay off debt and strengthen its balance sheet. In conclusion, the debt-to-equity ratio is currently the same as in 2021, and the company has managed its debt levels well to reduce the risk profile to a much lower level for its investors.

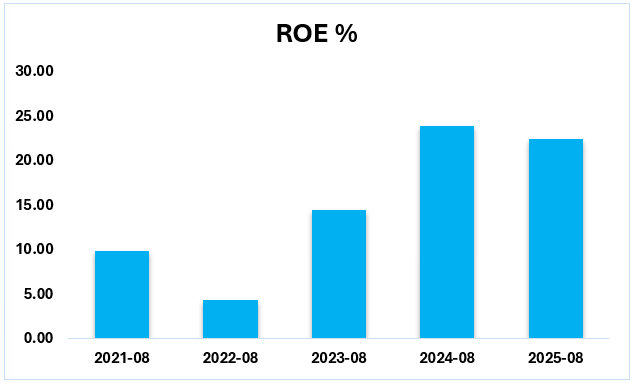

The following table shows Enerpac’s Return on Equity (ROE %), which represents “the profit generated relative to shareholders’ invested capital.” The ROE decreased to 4.29% in August 2022, which marked the end of an expensive restructuring process in which the company’s profits were low. The company’s ROE has improved significantly over the last few years, reaching 14.43% in 2023 and increasing to a high of 23.87% in August 2024, coinciding with the start of the ASCEND program and its associated profitability. In August 2025, the ROE decreased slightly to 22.47%, but this figure is still over five times what it was a few years ago, signifying a tremendous improvement in the company’s ability to leverage its equity base to drive growth and make it more attractive to investors.

Risks

There are several risks which should be considered while making decisions.

- The company's service segments, especially the Europe, Middle East, and Africa (EMEA) region, have experienced a sharp decline in business, with the most recent quarter experiencing a 21% decline. This macroeconomic weakness has forced the company to invest heavily in restructuring costs and layoffs to match the reduced customer demand with its workforce (Yahoo Finance).

- Political unrest in the Middle East is a major cause of concern for the company, as the region accounts for 10% of the total revenue generated by the company. This unrest has resulted in restricted access to facilities in the region and the shutdown of facilities. This has also led to overall economic uncertainty, global inflation, and supply chain disruptions (Marketbeta).

- While the product segment is on an upward trend, the company's overall gross profit margin has recently increased by more than 400 basis points. This compression is due to the decline in the company's service segment, increased costs due to global tariffs estimated at $12 million, and costs incurred in the integration of new acquisitions.

Conclusion

Enerpac Tool Group has shown significant growth in terms of profitability, financial performance, and debt management, thereby becoming more attractive for investments. Although the service segment has shown difficulties and the existence of macroeconomic risks, the strong product demand and expansion strategy ensure the company's potential for growth in the future. The company's focus on innovation and efficiency is also expected to maintain its competitive advantage in the industry. Overall, the company is a stable and promising option for investments with relatively low risks.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed

Musaffa Marketing

Musaffa Marketing

Foziljon Kamolitdinov

Foziljon Kamolitdinov