Company overview

GE Vernova is an energy and electrification firm that offers grid infrastructure, wind, and power generation equipment and services. To put it simply, it facilitates the production and transportation of power across the system. Both equipment sales and long-term services provide revenue for the company. Currently, the most significant aspects of the narrative are Power and Electrification, where demand is being sustained by grid upgrades, industrial power requirements, and data center expansion.

What’s driving the story right now

Investors are closely watching GE Vernova because it is in the midst of a massive electrical buildout. According to the corporation, this is a long-term change driven by electrification, grid modernization, industrial demand, and the power requirements of data centers and artificial intelligence. This is significant because GE Vernova is simultaneously exposed to multiple market segments rather than just one.

The more immediate narrative is that Wind remains the weaker component of the portfolio; GE Vernova Power and Electrification are driving the business. The notion that the corporation remains focused on the strongest segments of the market is supported by recent updates on nuclear cooperation, gas turbine activity, and grid-related demand. The market now appears more concerned with whether GE Vernova can continue to translate demand into long-term earnings growth than with whether demand exists, as GE Vernova stock has already had a successful run over the last three months and year to date.

Financial story

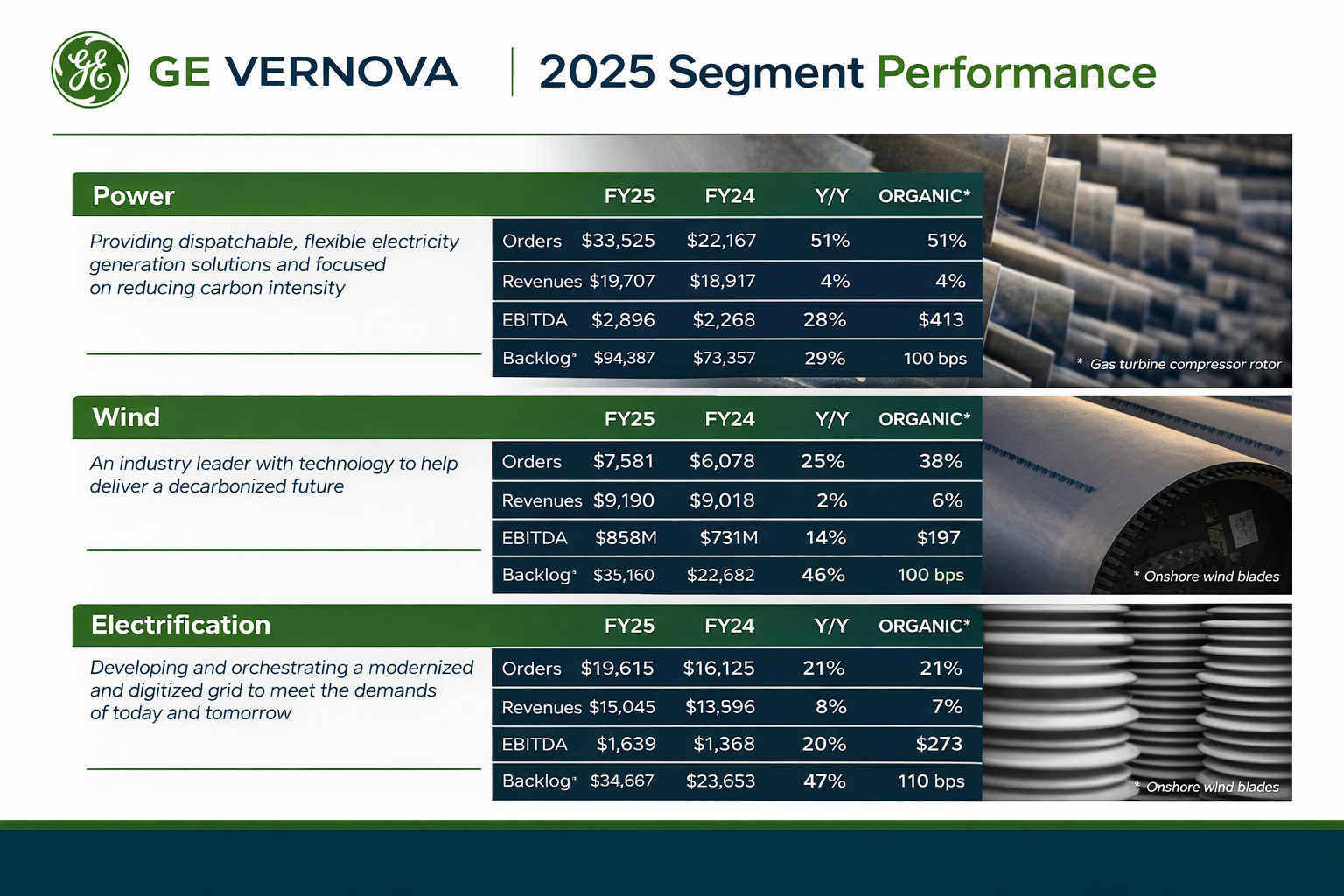

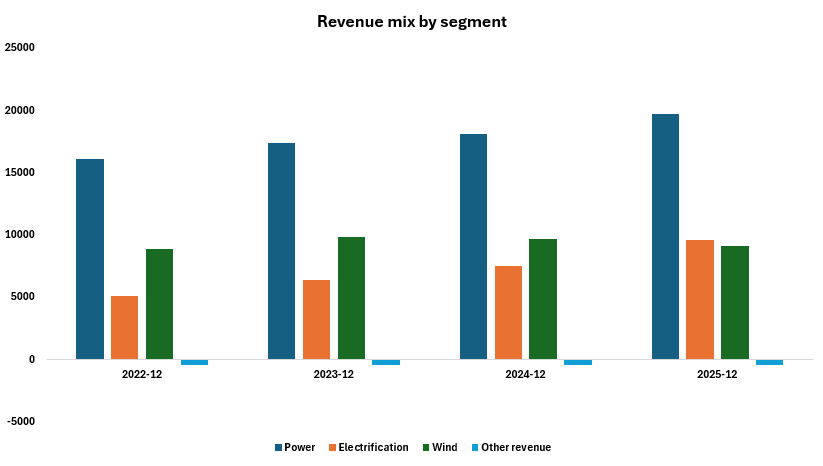

The best-performing areas were Power and Electrification. Power generated $19.77 billion of revenue with $2.90 billion of EBITDA and a backlog of $94.39 billion. Electrification generated $9.64 billion in revenue, $1.43 billion in EBITDA, and a backlog of $34.67 billion. In plain language, that means GE Vernova is benefiting from both sides of the electricity chain: it is selling generation equipment and systems needed to move and manage power across the grid.

The most significant story is what transpired throughout 2025, even though the most recent quarter appears to be good. GE Vernova produced operating cash flow of $4.99 billion, free cash flow of $3.71 billion, net income of $4.88 billion, and sales of $38.07 billion. The GE Vernova backlog reached $150.24 billion, a significant amount. This backlog is significant because it reflects a significant amount of work that has been scheduled but not yet completed, providing investors with greater insight into future earnings.

The company's own analysis is consistent with this. Demand for gas turbines is high, orders for grid equipment are expanding rapidly, and Electrification experienced its highest quarter of direct hyperscaler orders in Q4 2025. Additionally, it stated that in just four years, the backlog of electrification equipment had more than doubled to about $35 billion. This helps explain why this industry is receiving so much attention from the market.

The weak point is the wind. EBITDA remained negative at a $598 million loss, full-year Wind revenue dropped 6% to $9.11 billion, and backlog decreased 5% to $21.63 billion. The annual report makes it clear that this aspect of the business remains affected by offshore execution pressure, policy uncertainty, and a weaker U.S. onshore market. Therefore, the financial narrative does not show that things are getting better all at once. Power and Electrification dominate the current story, while investors will continue to look for improvements in Wind.

Read More:

- The Rise of DoorDash: Q4 Results, Expansion, And Challenges

- Moody’s 2026 Guidance Highlights AI Tailwinds—and the Real-Time Credit Cycle

- EQIX Q4 Earnings: Revenue, EBITDA Beat? AI Hyperscale & 2026 Outlook

Quarter check

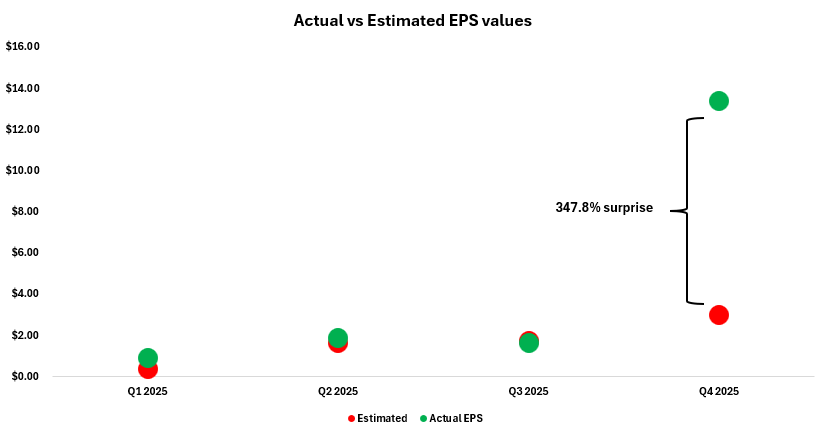

In contrast to the $10.21 billion estimate, GE Vernova reported Q4 revenue of $11.0 billion. Additionally, it reported Q4 non-GAAP EPS of $13.39, versus the $2.99 consensus. Both the top line and the primary profit figure that investors typically pay attention to have greatly outperformed.

The most significant takeaway is that GE Vernova ended the year far stronger than the market anticipated. However, a significant beat by itself does not resolve the entire stock discussion. Given that Wind is still under pressure and that some aspects of the company are far stronger than others, investors will still want to know how repeatable that level of earnings is.

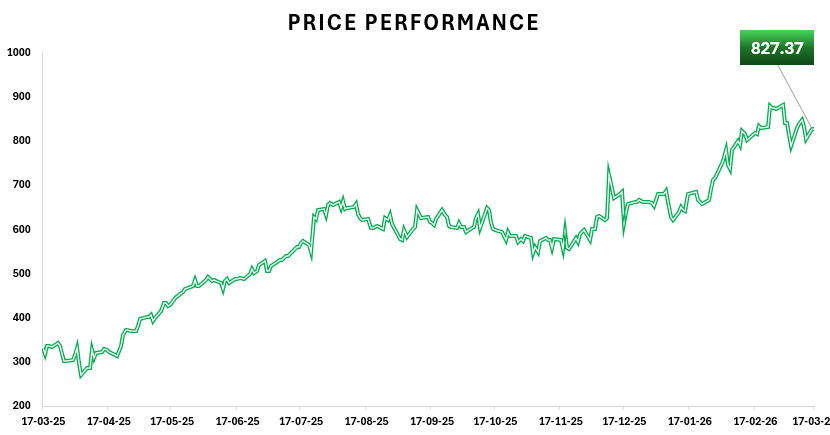

Price and valuation context

GE Vernova ended the day at $805.02. The stock was up 17.31% over three months and roughly 28.4% year to date, but it was down 3.26% on the day and 5.03% over five days. That indicates that despite a recent decline, the stock has already experienced a strong run. Additionally, compared to its 52-week low of $252.25, it is trading substantially closer to its 52-week high of $894.93.

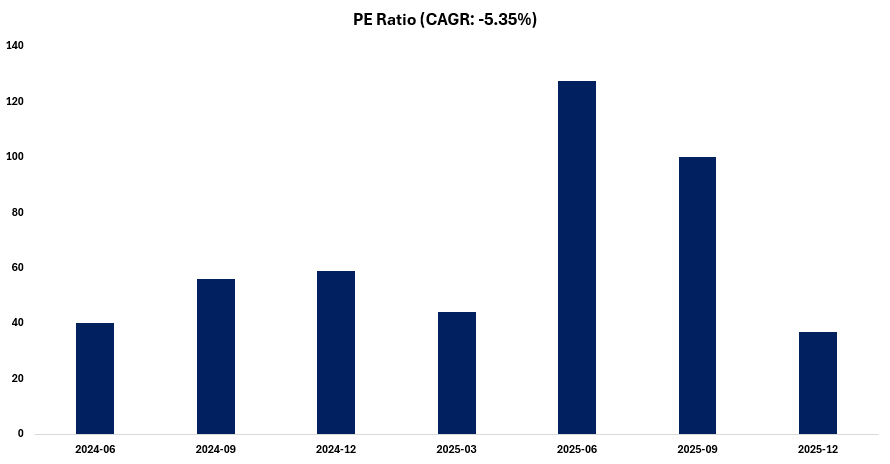

With EV/Sales at 7.02x and P/FCF at 41.11x, the shares are valued at 45.19x trailing earnings and 56.82x forward earnings. The most crucial thing for a novice investor to remember is that this is not a cheap company on basic headline multiples. Additionally, the fact that forward P/E is higher than trailing P/E indicates that the market does not anticipate the most recent earnings level to continue in the same manner in the future.

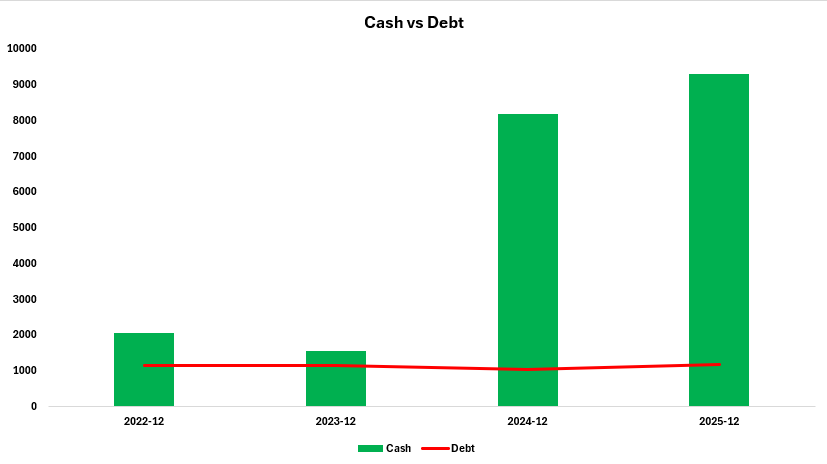

The company's large cash balance and extremely low debt position ensure strong liquidity. The fact that the company has $8.85 billion in cash and no stated long-term debt lends credence to the notion that it has space for investments, growth funding, and capital returns. Because GE Vernova is increasing capacity and attempting to capture a very large demand cycle, that financial position is important.

Risks

Since power and electrification are doing most of the heavy lifting, the most obvious commercial risk is that wind remains poor. Overall profitability may continue to be hampered by slower segments of the wind market, regulatory uncertainty, and offshore implementation challenges. Beyond that, the annual report identifies well-known but significant concerns for a business like this: competition, supply chain pressure, tariffs, large-project execution, manufacturing capacity limitations, and financing conditions. Strong demand does not always translate into seamless delivery, which is a real concern, particularly for companies with lengthy project timeframes and intricate client contracts.

Shariah Compliance Lens

For investors reviewing Shariah-compliant stocks GEV, as of January 2026, GE Vernova (GEV) is classified as Shariah-compliant (Halal) with a B Musaffa rating based on the Shariah Screening results at Musaffa. GEV’s 2025 Annual Report was used to conduct the screening analysis in line with the AAOIFI methodology. GEV passed all three required screening thresholds, with 97.10% of its business activity meeting the permissible (Halal) threshold (0.68% doubtful and 2.22% not Halal). Both interest-bearing securities and assets (9.37%) and interest-bearing debt (0.31%) remain below 30% of the 36-month average market capitalization.

Conclusion

Power generation and grid infrastructure, rather than wind, are increasingly driving GE Vernova's current narrative. The company appears well-positioned to profit from growing electricity demand, the Q4 beat was quite solid, and the full-year cash generation and backlog were remarkable. The key challenge is whether GE Vernova can continue to stabilize the portfolio's weaker segments and convert that broad demand backdrop into consistent profitability growth.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed