Company overview

Among biopharmaceutical stocks, Gilead develops therapies for conditions such as inflammation, cancer, liver disease, and HIV. HIV remains the company's principal source of income. The most crucial aspect of the tale at this point is whether the firm can continue to develop while some cancer and cell therapy sectors remain uneven, driven by significant growth in HIV, new preventive and treatment launches, and improving momentum in liver disease.

What’s driving the story right now

The current narrative around Gilead is rather obvious. The majority of the work is still being done by its core HIV business, and this strength was evident once more during the quarter. Descovy expanded far more quickly than Biktarvy, and management also cited the favorable Phase 3 findings for the daily oral BIC/LEN HIV regimen and the successful U.S. introduction of Yeztugo. This gives investors the impression that Gilead is working to develop the next level of HIV treatment rather than merely relying on existing medications.

However, the narrative is not flawless. As COVID-related demand returns to normal and oncology remains inconsistent, Veklury continues to decline. Trodelvy expanded, but it also revealed that the STAR-221 trial was halted and that the Phase 3 ASCENT-07 study failed to meet its primary endpoint. Therefore, the market is likely viewing Gilead as a firm with a solid, reliable core business but still needing more consistent support from the rest of the portfolio.

GILD Financial story

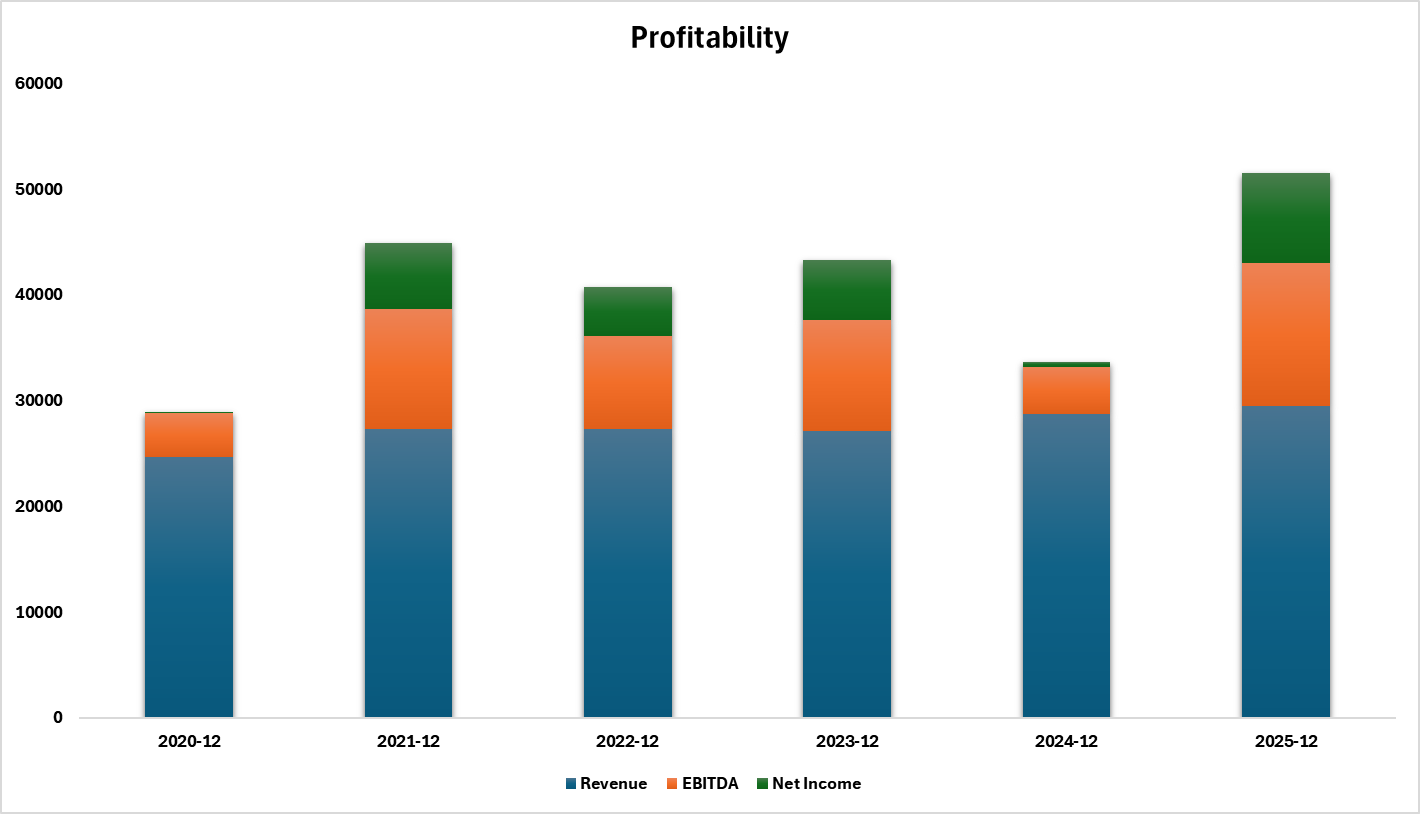

Detailing the GILD earnings, Gilead reported $7.93 billion in sales for the fourth quarter, a 5% increase over the same period last year. That looks like a good outcome, but the more important information is hidden beneath. Because Veklury is now a declining COVID-era revenue stream rather than a long-term growth engine, product sales minus Veklury increased by 7%, providing a better view of the core company.

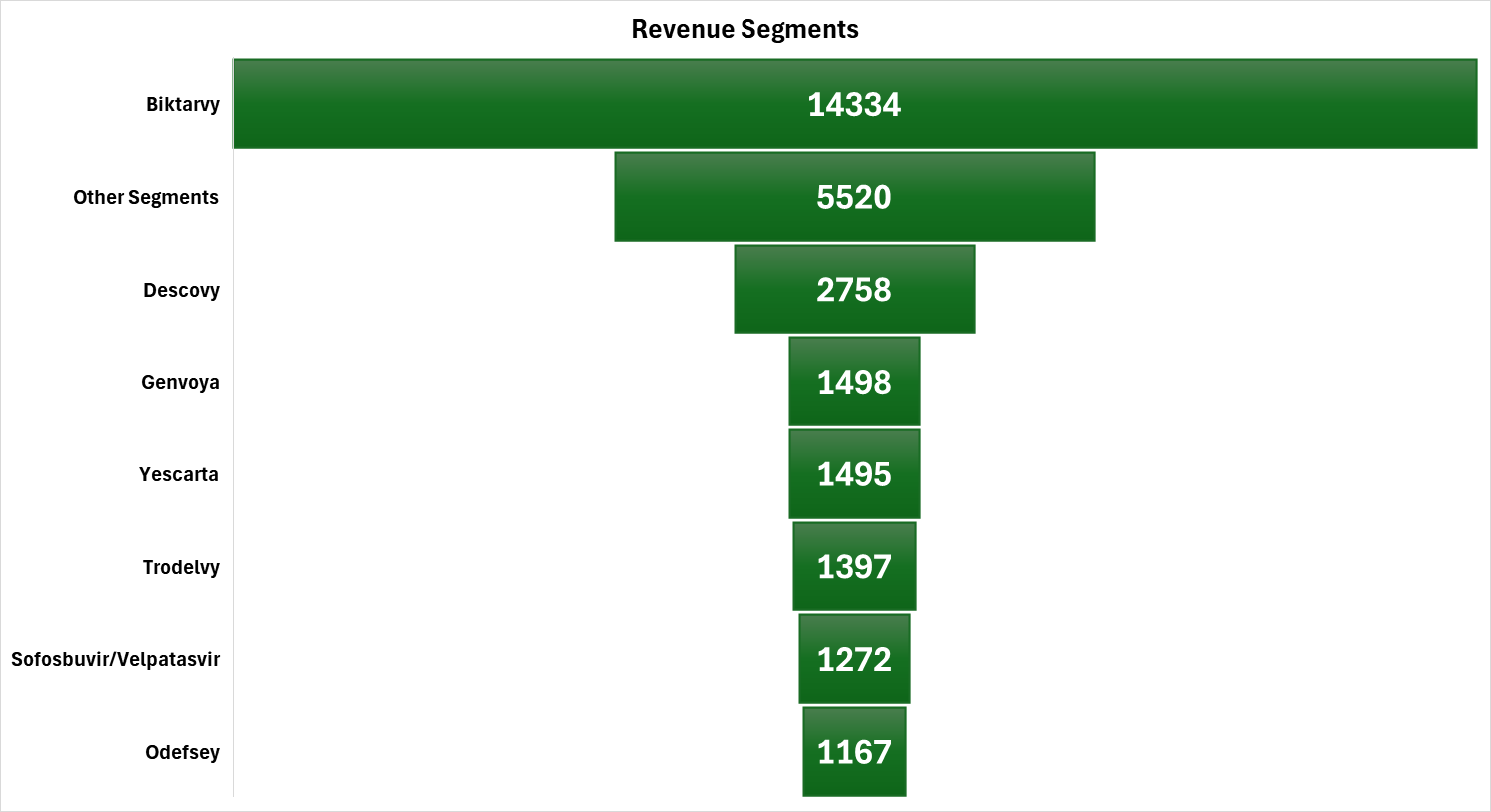

HIV and liver disorders dominated the period. With Biktarvy at $3.97 billion and Descovy at $819 million, HIV revenues increased 6% to $5.80 billion. Demand for Livdelzi contributed to a 17% increase in liver disease revenues to $844 million. In short, Gilead's core business continues to see strong demand where it matters most. This is significant because these companies are big enough to influence the financial course of the entire organization.

The portfolio's other sections were less encouraging. At $842 million, Gilead Oncology's revenue was essentially stagnant. Trodelvy increased by 8% to $384 million during that period, while cell therapy sales decreased by 6% to $458 million, as Yescarta and Tecartus were under pressure from competitors. Given the lower number of COVID-related hospitalizations, Veklury's 37% decline to $212 million was anticipated. Therefore, the financial situation is not a universal strength. Stronger performance in liver disease and HIV helps counteract weaker regions in other areas.

Cash generation and profitability remained robust. Operating cash flow was $3.33 billion, net income was $2.18 billion, and operating income was $1.98 billion in Q4. Gilead reported $29.44 billion in sales, $10.02 billion in operating income, $8.51 billion in net income, $10.02 billion in operating cash flow, and $9.46 billion in free cash flow for the year. This provides the business with strong funding for dividends, buybacks, and ongoing pipeline investments.

Read more:

- Lam Research Stock Analysis: The Engine Behind AI Semiconductors

- GE Vernova Stock Analysis: GEV Earnings & Q4 Results Driven by Power and Grid Demand

- Adobe Stock Analysis: ADBE Earnings & Q1 Results Tempered by AI Concerns

Gilead Quarter check

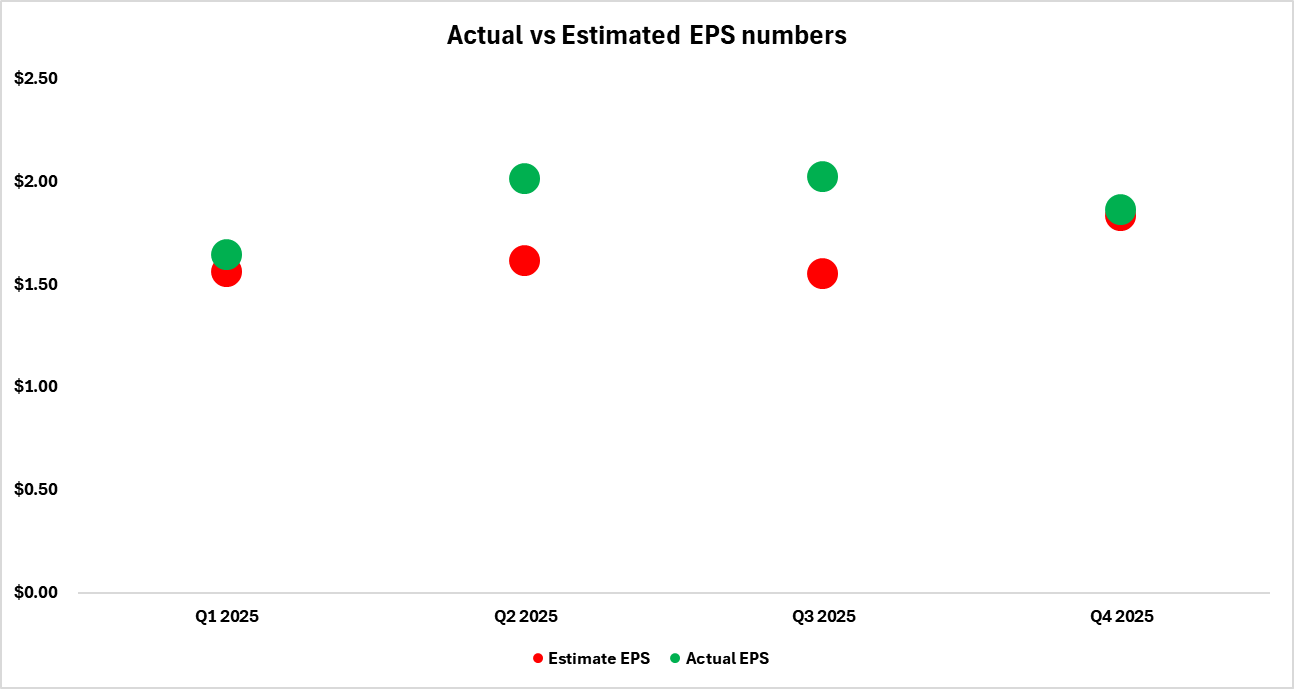

Gilead reported non-GAAP EPS of $1.86 compared to the estimate of $1.83 and Q4 sales of $7.93 billion compared to the consensus of $7.68 billion. This indicates that the company's revenue and profitability exceeded forecasts.

The subtle difference is that non-GAAP EPS was actually somewhat lower than the $1.90 recorded a year earlier, and the profit beat was minimal. Stronger product sales and reduced SG&A partially offset the reduction, according to the business, which was mostly caused by increased acquired IPR&D spending. This was a beat, but it wasn't the type that instantly altered the plot. Rather than demonstrating a significant shift in trajectory, the quarter largely confirmed that Gilead's core business remains steady and continues to expand.

Outlook

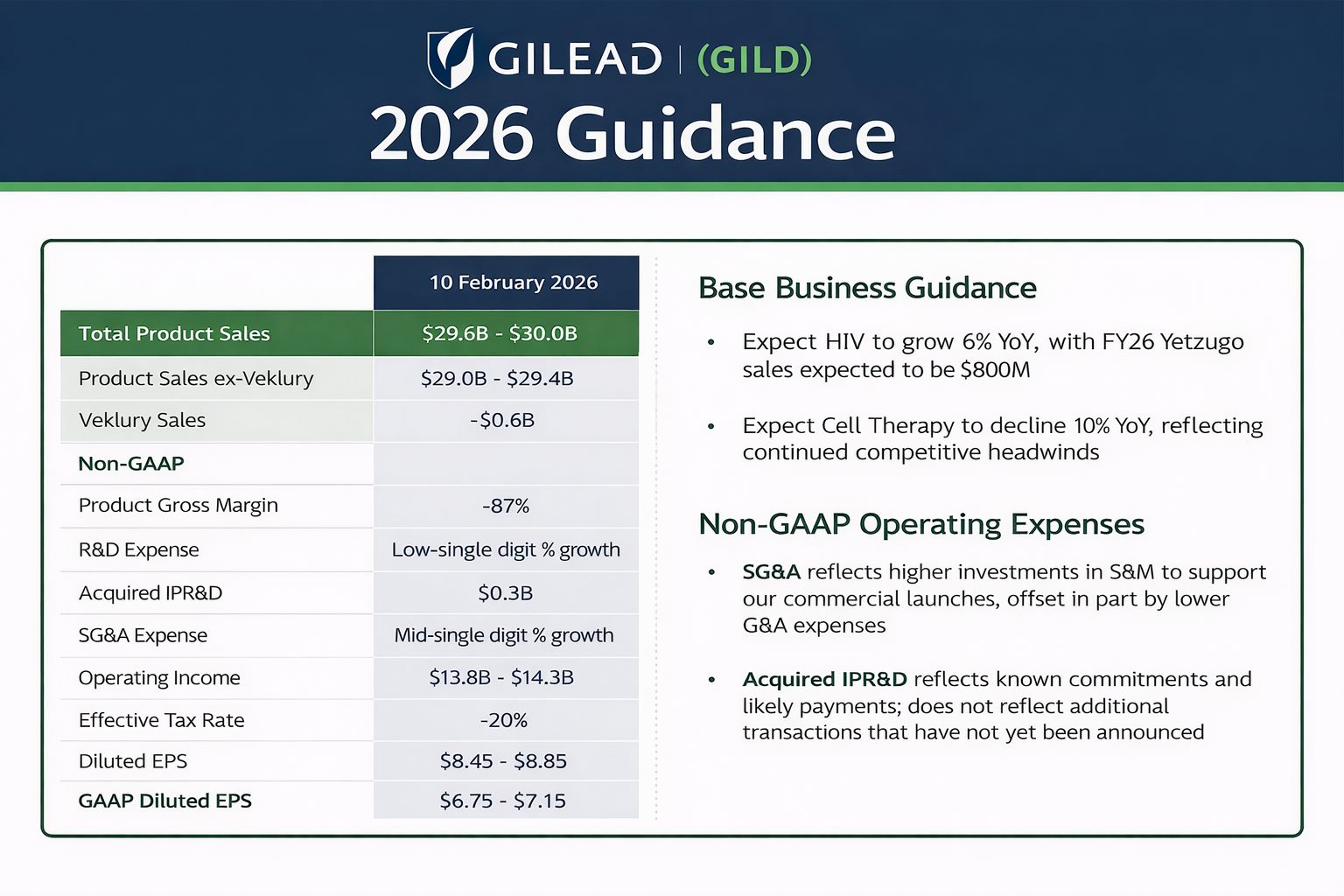

Gilead projects $29.6 billion to $30.0 billion in product sales, $29.0 billion to $29.4 billion in product sales minus Veklury, $600 million in Veklury revenues, $6.75 to $7.15 in GAAP diluted EPS, and $8.45 to $8.85 in non-GAAP diluted EPS for the entire year 2026.

To put it simply, management is encouraging steady growth rather than a sudden surge. While the market continues to monitor whether additional HIV launches and pipeline advancements may add more impetus over time, the firm seems to be telling investors that the core business should continue to go forward, especially outside Veklury.

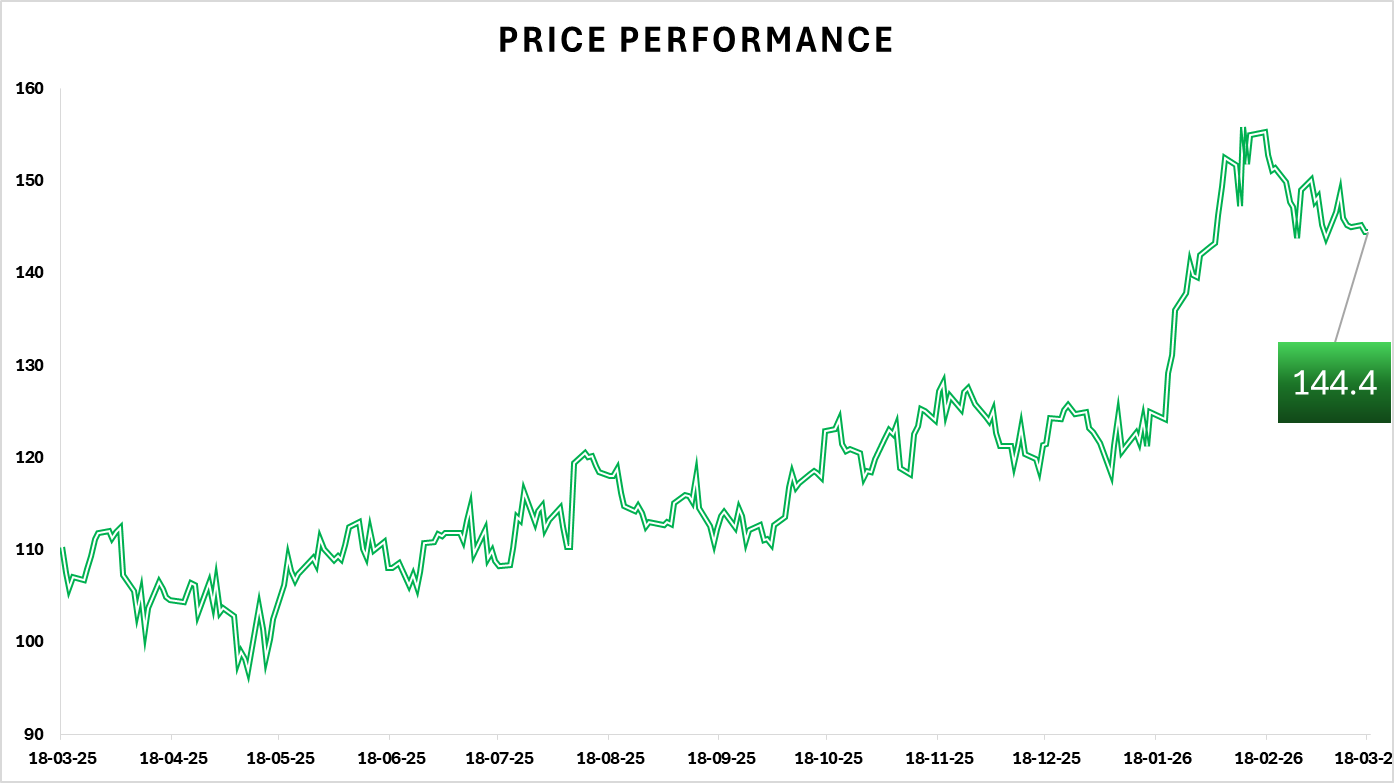

Price and valuation context

At $144.40, Gilead closed. Over the course of the day and the five days, the stock fell 0.56%. While it was up 18.98% over three months, it was down 7.0% over one month. This implies that before dropping off more recently, the stock enjoyed a robust run.

The shares are still well above the 52-week low of $93.37 and below the 52-week high of $157.29. Additionally, the volume of 3.83 million was below the 20-day average of 7.53 million, indicating that exceptionally high trading was not the cause of the most recent rise.

Gilead is valued at 21.11x trailing earnings and 16.61x projected earnings, with P/FCF at 23.77x and EV/Sales at 6.84x. The lower forward P/E indicates that the market anticipates future improvements in profits. This is not a cash-rich business like some of its major pharmaceutical counterparts, as the balance sheet picture, based on the value snapshot you supplied, indicates significant net debt of around $22.13 billion. Strong cash creation, however, allows the business to continue investing in its pipeline while supporting capital returns and dividends.

Risks

The most important concern is that Gilead's development narrative is still largely reliant on HIV. Although the company is doing well now, focus is always important. Additionally, oncology remains uneven, with conflicting trial outcomes and pressure in cell therapy, which may limit the company's ability to benefit from a broader portfolio. Additionally, the corporation itself identifies risks related to generic competition, payer mix, trade policy, legislation, price pressure, product commercialization, and the difficulty of converting clinical projects into successful launches.

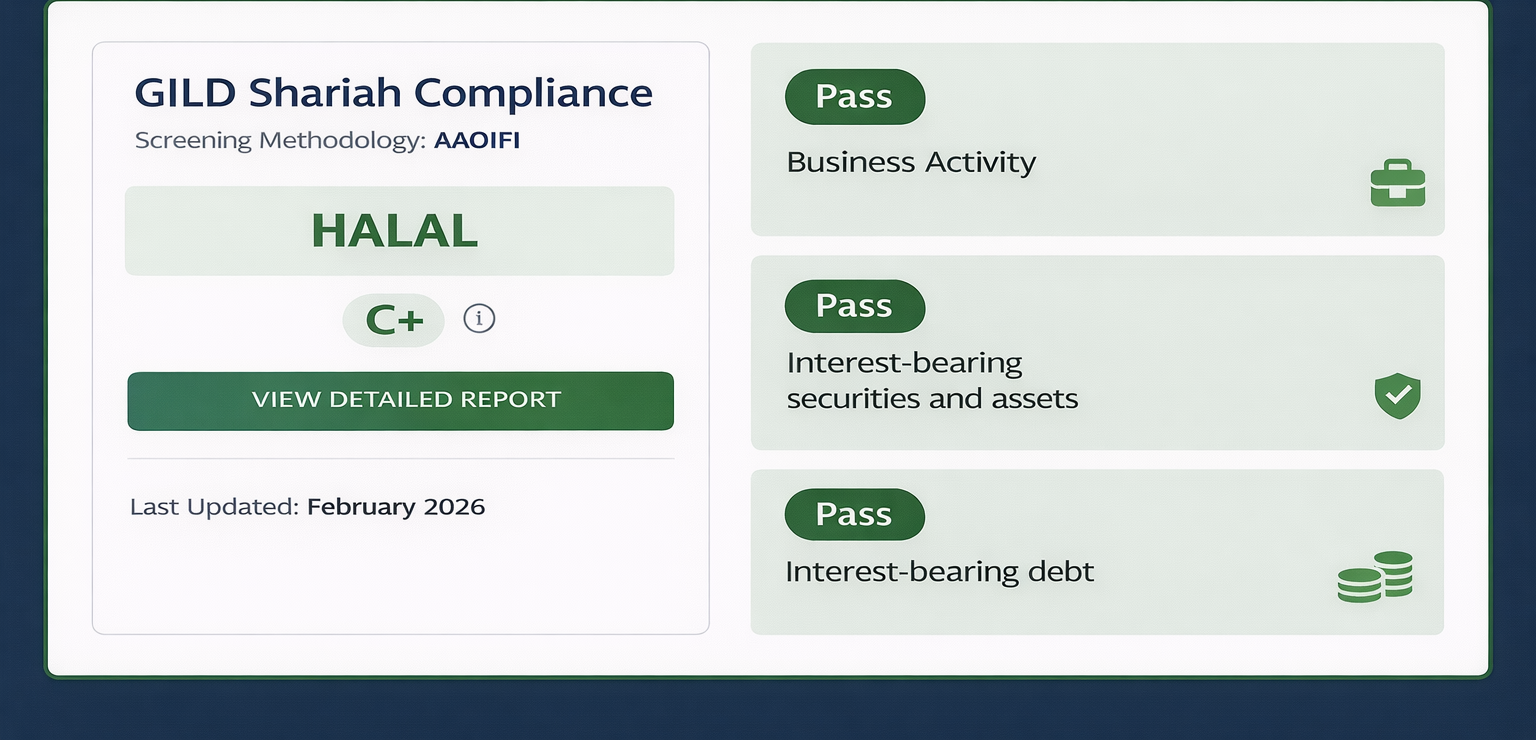

Shariah Compliance Lens

As of February 2026, Gilead Sciences (GILD) is classified as Shariah-compliant (Halal) with a C+ Musaffa rating, based on Shariah Screening results from Musaffa. GILD’s 2025 Annual Report was used to conduct the screening analysis in line with the AAOIFI methodology. GILD passed all three required screening thresholds, with 98.85% of its business activity meeting the permissible (Halal) threshold (0.00% doubtful and 1.15% not Halal). Both interest-bearing securities and assets (9.25%) and interest-bearing debt (21.75%) remain below 30% of the 36-month average market capitalization.

Conclusion

Gilead had a strong quarter. The non-GAAP EPS beat, the revenue beat, and the core business outside Veklury continued to expand. Liver illness is assisting, HIV is still the major focus of the narrative, and 2026 projections indicate another year of consistent advancement. The crucial question at hand is whether Gilead can generate enough growth from its expanded pipeline and more recent products to lessen its reliance on HIV alone.

Sources

- Gilead Sciences Inc. Stock Analysis

- Gilead Sciences Inc Stock News from GuruFocus

- Gilead Sciences Inc

- Press Release

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Suhail Patel

Suhail Patel