Company overview

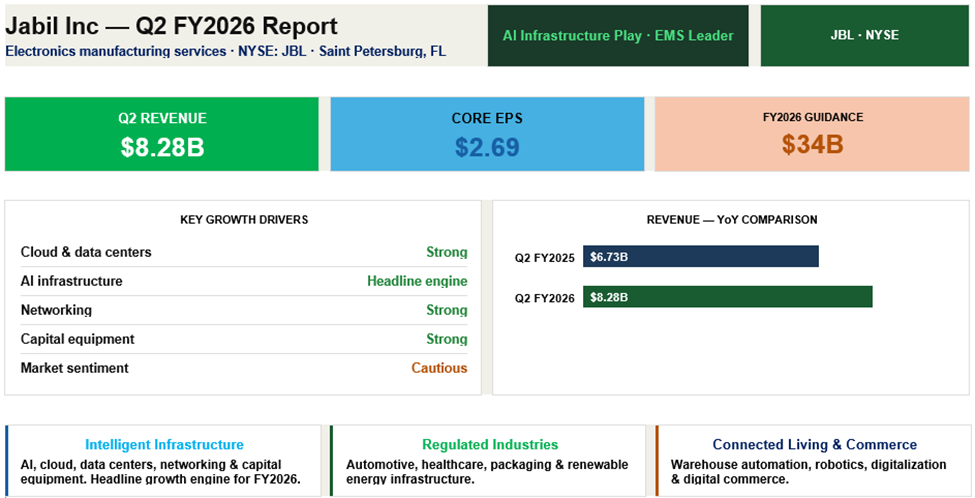

Jabil is a manufacturing and supply chain partner that assists big businesses with product design, production, and delivery. Instead of selling consumer goods under its own brand, it operates in the background as one of the world's largest electronics manufacturing services (EMS) providers. The business generates revenue by offering engineering, production, and associated services in a variety of sectors. The most significant aspect of the tale at this time is that Jabil is witnessing strong demand across infrastructure domains, including cloud, data centers, networking, and capital equipment. For investors tracking AI infrastructure stocks, JBL stock has become a key name to watch in 2026.

What’s driving the story right now

Strong execution and a more cautious market response are currently driving Jabil's story. In addition to raising its full-year FY2026 sales forecast to $34 billion and demonstrating strong demand going into Q3, the business produced a strong Q2 beat. This lends credence to the idea that Jabil is benefiting from increased activity in networking, cloud computing, data centers, and broader infrastructure initiatives. Jabil AI data center demand, in particular, continues to be the headline growth engine behind the Intelligent Infrastructure segment.

However, the latest news flow indicates that investors are not only responding to the beat. The market is assessing whether there is still sufficient upside following the company's impressive run, and the tone surrounding the stock has become more cautious. Because of this, the narrative goes beyond "good quarter, stock up." It is more concerning whether Jabil can continue to convert this momentum into long-term growth robust enough to meet current expectations.

Financial story

Jabil reported a robust fiscal Q2, with core EPS climbing to $2.69 and sales increasing to $8.28 billion from around $6.73 billion a year earlier. The Jabil Q2 FY2026 earnings report showed demand was strong throughout the quarter, with management highlighting the strength of Intelligent Infrastructure in particular. This is significant since cloud, data center, networking, and capital equipment spending—all of which are now among the market's strongest sectors—are intimately linked to this aspect of the business.

The business did more than simply report increased revenue. Better earnings power was also demonstrated. Core operating income was $436 million, while GAAP operating income was $374 million. This indicates to investors that Jabil is reaping the benefits of both volume growth and an improved business mix. The automotive and renewable energy sectors helped Regulated Industries perform better than anticipated, according to management, supporting the idea that Jabil revenue growth growth is not coming from a single sector.

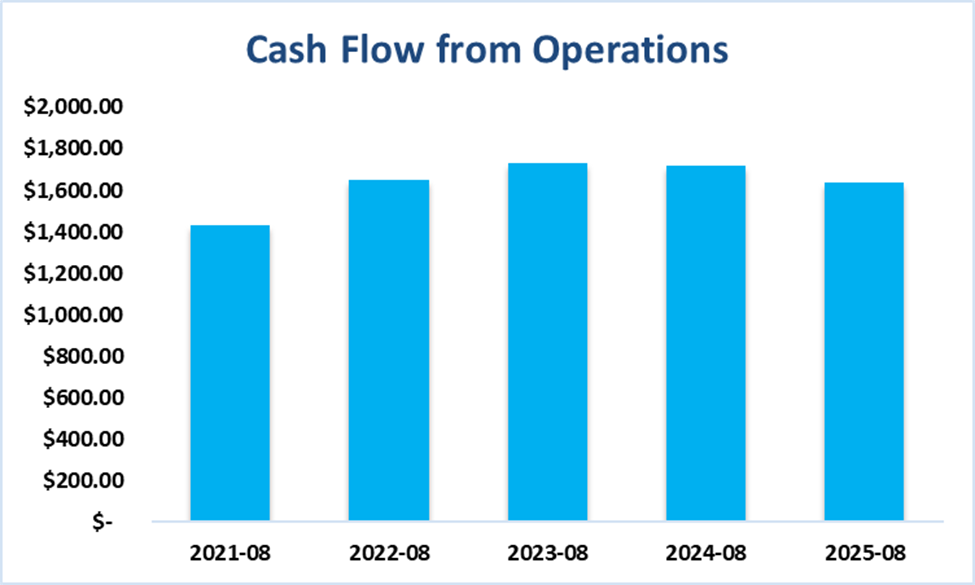

Cash generation continues to play a significant role in the narrative. Jabil produced $734 million in operational cash flow and $632 million in adjusted free cash flow during the first half of the 2026 fiscal year. Management is now aiming for an adjusted free cash flow of more than $1.3 billion for the full year. To put it simply, Jabil is demonstrating how increased demand translates into actual cash, sales, and profitability.

Confidence was the quarter's main takeaway. Jabil increased its full-year FY2026 estimate to $34.0 billion in sales and $12.25 in core EPS following the Q2 beat. That implies that management believes the company is strong enough to sustain the momentum. The assumption that Jabil is getting closer to infrastructure initiatives that still have capacity to develop is further supported by the current news flow about AI data center photonics and higher Q3 projections.

Read more:

- Lam Research Stock Analysis: The Engine Behind AI Semiconductors

- GE Vernova Stock Analysis: GEV Earnings & Q4 Results Driven by Power and Grid Demand

- Adobe Stock Analysis: ADBE Earnings & Q1 Results Tempered by AI Concerns

Quarter check

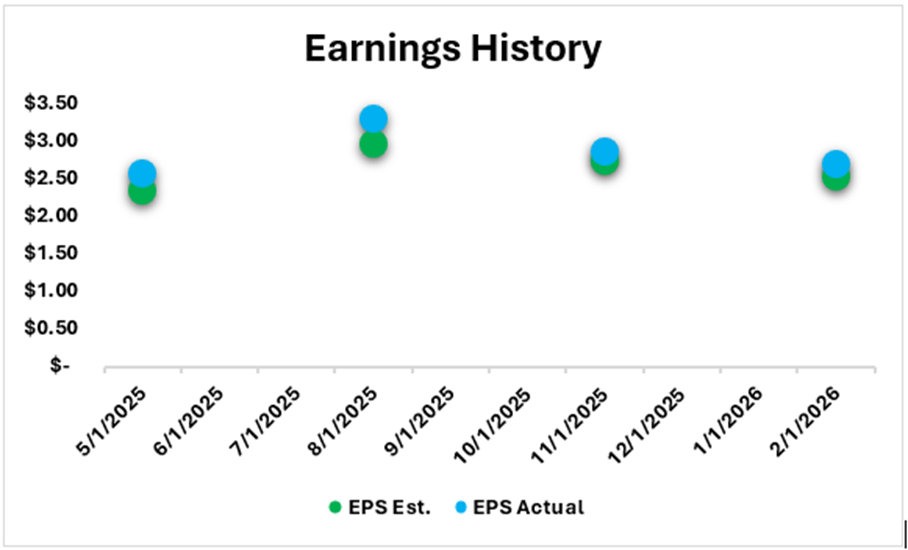

Jabil announced core EPS of $2.69, compared with an estimate of around $2.5, and Q2 sales of $8.28 billion, compared with a consensus of roughly $7.75 billion. This indicates that the company's revenue and profitability exceeded forecasts.

However, the stock market responds to more than simply the last quarter. In this instance, the business also increased its full-year outlook, but following the release, the shares continued to decline. The most straightforward argument is that, following the stock's incredible climb over the previous year, investors may have already priced in a great deal of hope. Therefore, the beat was important, but it might not have been sufficient to raise expectations further in the near future.

Outlook

Jabil projects core EPS of $2.83 to $3.23 and sales of $8.1 billion to $8.9 billion for the third quarter of FY2026. Additionally, it led to GAAP EPS of $2.36 to $2.76.

Management now projects $34.0 billion in sales, a core operating margin of 5.7%, a core EPS of $12.25, and more than $1.3 billion in adjusted free cash flow for the whole year. According to the source pack, core EPS increased from $11.55, and revenue projection increased from $32.4 billion. Put simply, the Jabil FY2026 guidance is informing investors that business conditions are stronger than it had anticipated at the beginning of the year and that this strength should persist into the second half.

Price and valuation context

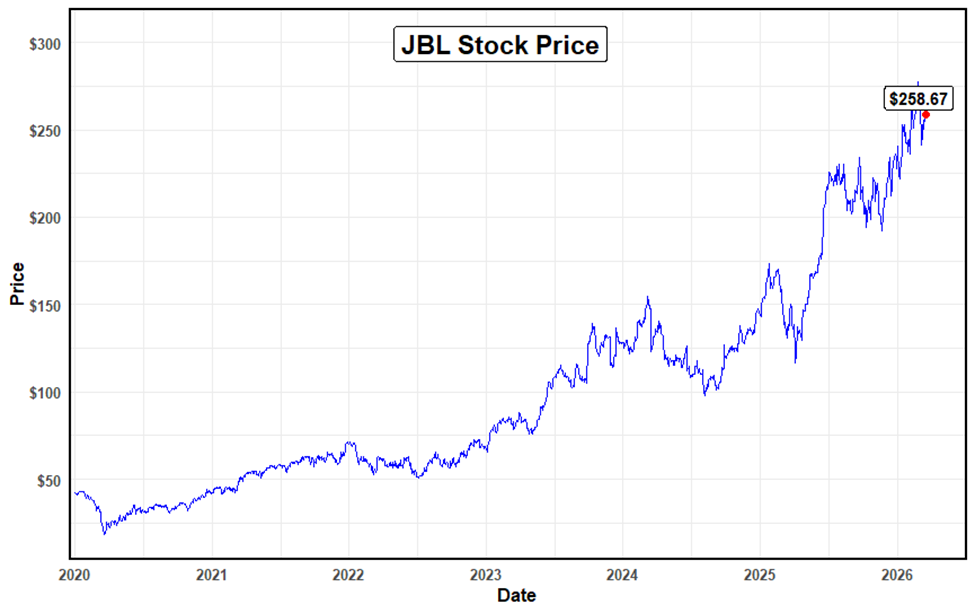

Jabil closed up at $258.67. The JBL stock price stock was up 1.26% over five days, 10.33% over three months, and 9.55% year to date, despite a 0.96% decline on the most recent day. It is still well above the 52-week low of $108.66 but below the 52-week high of $281.37. Even if the current response has been muted, this indicates that the stock has already had a fairly strong increase over the last year.

On valuation, the shares trade at about 40.23x trailing earnings and about 21.1x forward earnings, with EV/Sales at 0.86x and EV/EBITDA at 12.7x. The lower forward P/E suggests the market expects stronger earnings ahead, which fits with the raised FY2026 outlook. The balance sheet, however, is not a net-cash story. Quarter-end cash was $1.83 billion, while total debt was about $3.88 billion, so the company still carries meaningful leverage despite generating solid cash flow.

Risks

Jabil's reliance on client demand cycles in rapidly changing areas poses the greatest risk. Production scheduling, manufacturing capacity, customer concentration, component sourcing, supplier dependency, acquisitions, foreign operations, rivalry, transportation, cybersecurity, regulation, and financial market volatility are among the issues that management itself highlights. Another less complicated market risk is that, following a robust share-price run, investors may have such high expectations that they are not entirely satisfied by even a beat-and-raise quarter.

Shariah Compliance lens

For investors evaluating Shariah compliant stocks JBL, as of January 2026, Jabil (JBL) is classified as Shariah-compliant (Halal) with a B- Musaffa rating based on the Shariah Screening results at Musaffa. JBL’s 2026 1st Quarter Report was used to conduct the screening analysis in line with the AAOIFI methodology. JBL passed all three required screening thresholds, with 99.78% of its business activity meeting the permissible (Halal) threshold (0.00% doubtful and 0.22% not Halal). Both interest-bearing securities and assets (9.62%) and interest-bearing debt (17.66%) remain below 30% of the 36-month average market capitalization.

Conclusion

Jabil's good quarter and improved full-year forecast support the view that demand in its major infrastructure markets remains robust. The company is exhibiting improved profitability, better revenue growth, and more management confidence. The crucial question is whether Jabil can continue to translate this enthusiasm into steady growth, particularly as the market grows more cautious following the stock's impressive surge.

Sources

- Jabil Inc. Stock Analysis

- Jabil Inc Stock News from GuruFocus

- Jabil Inc

- Jabil Posts Second Quarter Results

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.