Company overview

KLA is a semiconductor equipment firm that primarily assists chipmakers in measuring, inspecting, and improving the production of sophisticated devices. That may sound scientific, but the business is fairly simple to understand: KLA makes a lot of money because manufacturers require better control tools as chip production becomes more sophisticated. The most significant aspect of the narrative at the moment is the growing demand for better process control in the manufacturing of AI-related chips, particularly in foundry, logic, memory, advanced packaging, and services.

What’s driving the story right now

The main factor influencing KLA's narrative is its location in a crucial area of the semiconductor supply chain. The final chips are not directly sold by it. Rather, it offers the equipment that enables clients to make such chips more precisely and in larger quantities. Spending on KLA's AI infrastructure is increasing, exposing KLA to some of the best semiconductor investment opportunities.

The current news flow also supports that concept. During its investor day, KLA reaffirmed its outlook, announced a new repurchase program, and increased its dividend. This combination typically suggests that management remains optimistic about cash generation and demand. The market is focused on whether KLA can continue to turn that demand backdrop into durable earnings growth, especially after a strong run in the KLA Corp stock over the last few months.

Financial story

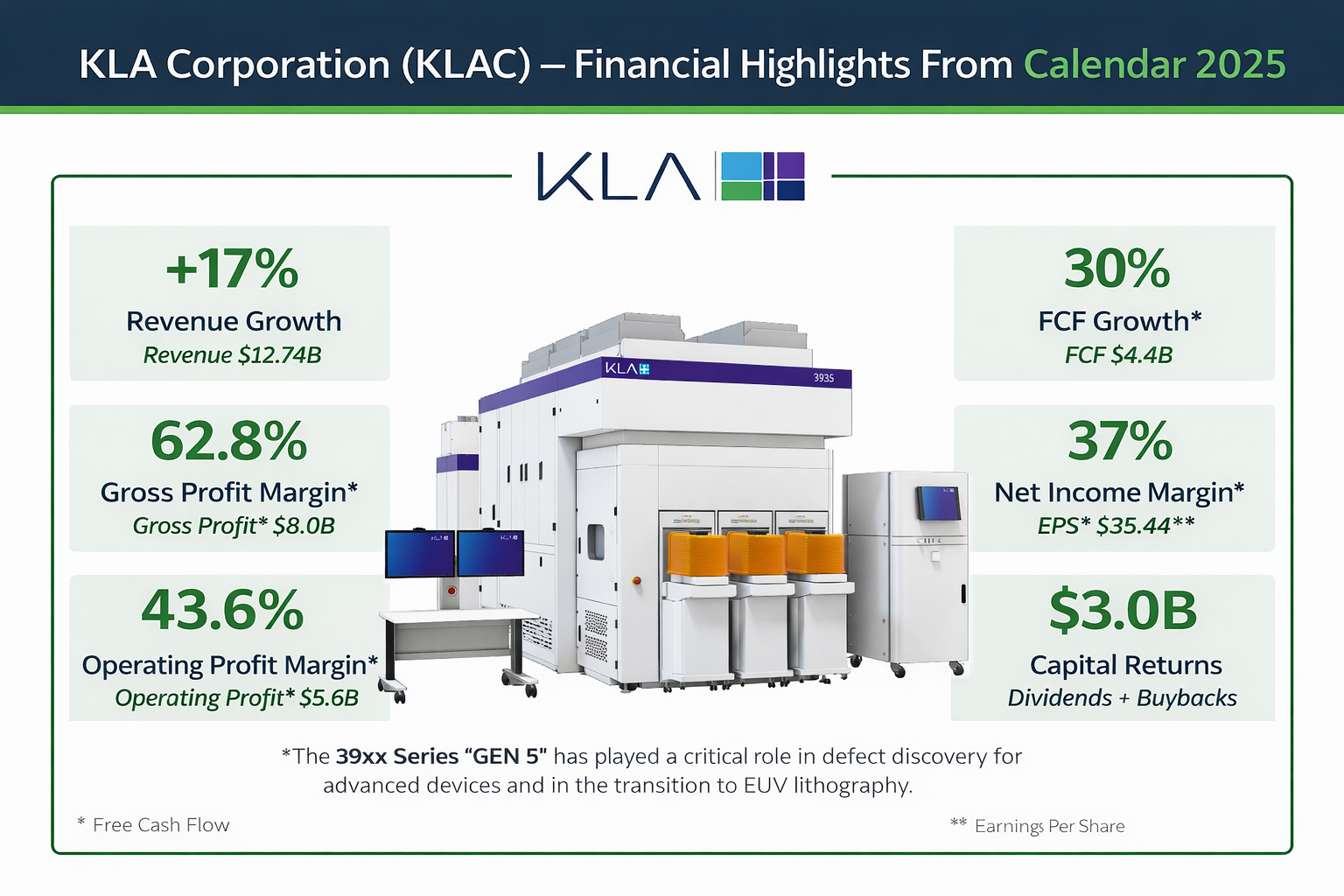

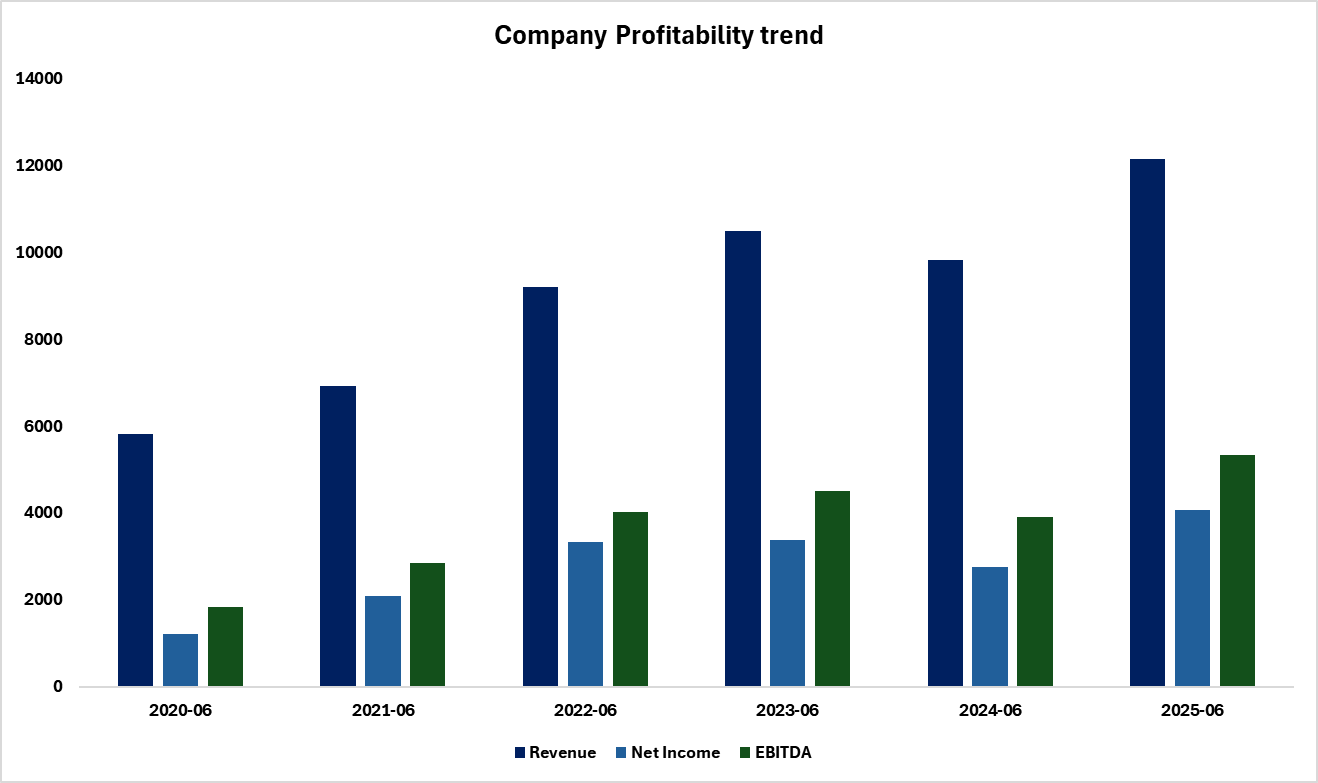

Highlighting the KLA Q2 FY26 results, KLA's fiscal Q2 2026 revenue increased from $3.08 billion to $3.30 billion. Additionally, the business recorded $1.15 billion in GAAP net income and $1.17 billion in non-GAAP net income. That suggests a quarter with both strong profitability and revenue growth.

The business's focus on its primary franchise remains evident in the revenue mix. Compared with Specialty Semiconductor Process, which generated approximately $141 million, and PCB and Component Inspection, which generated about $152 million, Semiconductor Process Control generated nearly $3.00 billion in quarterly sales. To put it another way, the majority of the work is still being done by the core process control industry, which is significant since it is the area most directly related to the need for advanced chip fabrication.

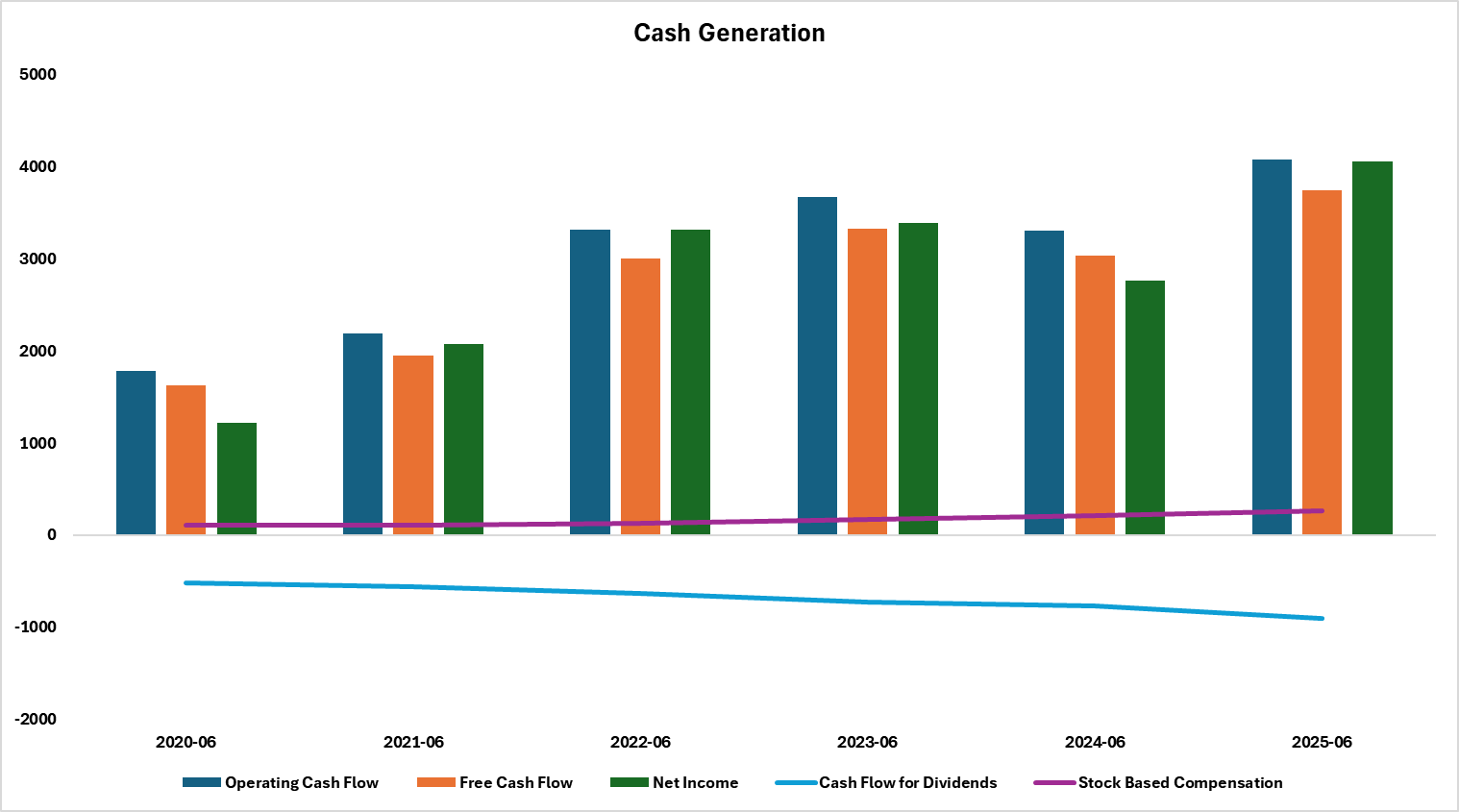

KLA is still making a lot of money. Free cash flow was $1.26 billion for the quarter, while operating cash flow was $1.37 billion. These amounts were $4.77 billion and $4.38 billion during the previous 12 months. This is significant because it demonstrates that the business is reporting more than simply accounting profits. Additionally, it is turning a sizable portion of its operations into actual cash to fund dividends and buybacks.

The terminology used by the corporation during the quarter was also noteworthy. The business is reaping the benefits of AI infrastructure buildout across foundry/logic, memory, advanced packaging, and services, according to management, who also said that KLA produced a record quarter and calendar year for revenue, non-GAAP operating income, and free cash flow. This provides investors with a clear picture of what management thinks is driving the company at the moment.

Quarter check

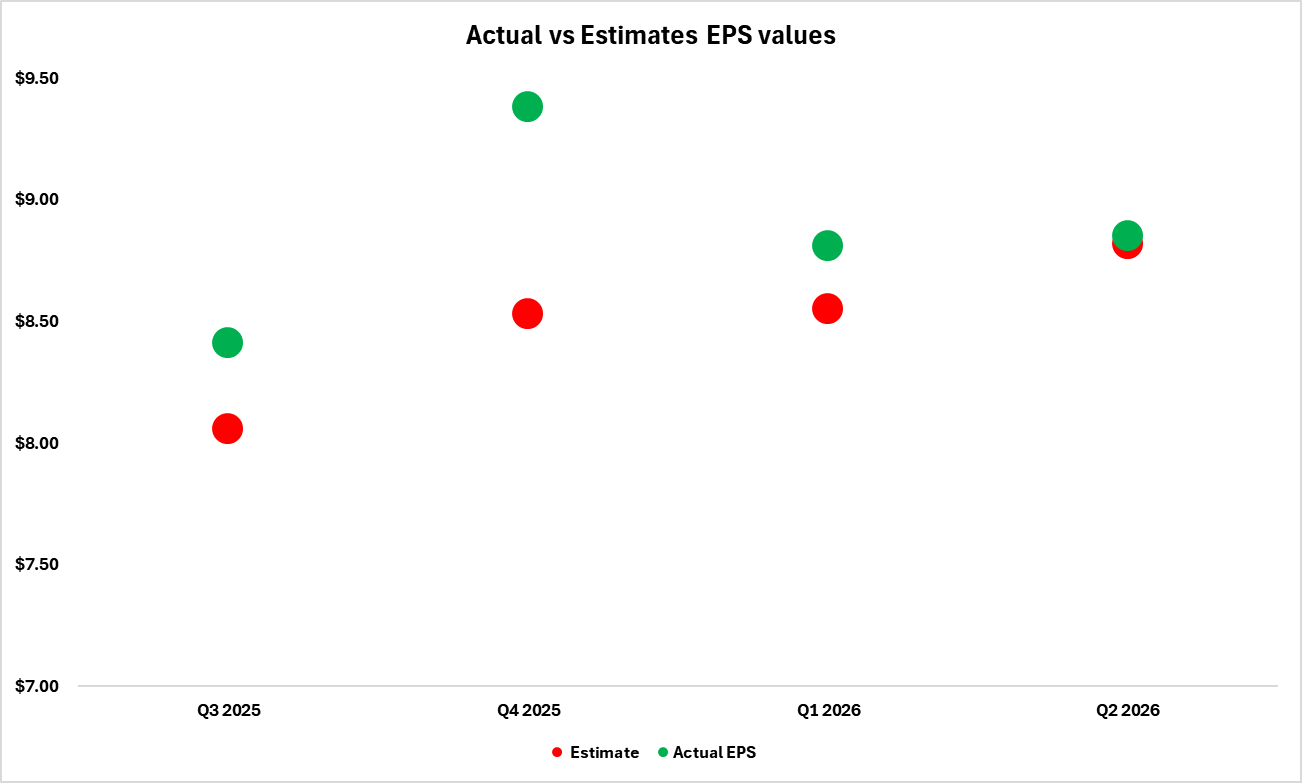

In the recent KLAC earnings report, KLA's Q2 sales were $3.30 billion, above the $3.25 billion estimate, and its non-GAAP EPS was $8.85, above the $8.82 consensus estimate. Both sales and profitability have increased.

Even though the EPS beat was not very significant, it is nonetheless significant because KLA is already a well-known semiconductor brand with high expectations. Investors often seek evidence that a company's growth and margins are sustainable when it trades at a premium value. That was accomplished this quarter. The fact that the business combined the outcome with consistent direction rather than a cautious message is also beneficial.

Outlook

KLA projects $3.35 billion in revenue for fiscal Q3 2026, with a $150 million margin of error. Additionally, it led to a non-GAAP gross margin of 61.75% plus or minus 1 percentage point, GAAP EPS of $8.85 plus or minus $0.78, and non-GAAP EPS of $9.08 plus or minus $0.78.

To put it simply, the forecast indicates that management continues to anticipate strong profitability and steady demand for the upcoming quarter. Because it demonstrates that KLA still anticipates keeping a sizable portion of each revenue dollar after direct expenditures, the gross margin estimate is very helpful. This bolsters the idea that, despite the semiconductor industry's regular cycles, the company's business model remains solid.

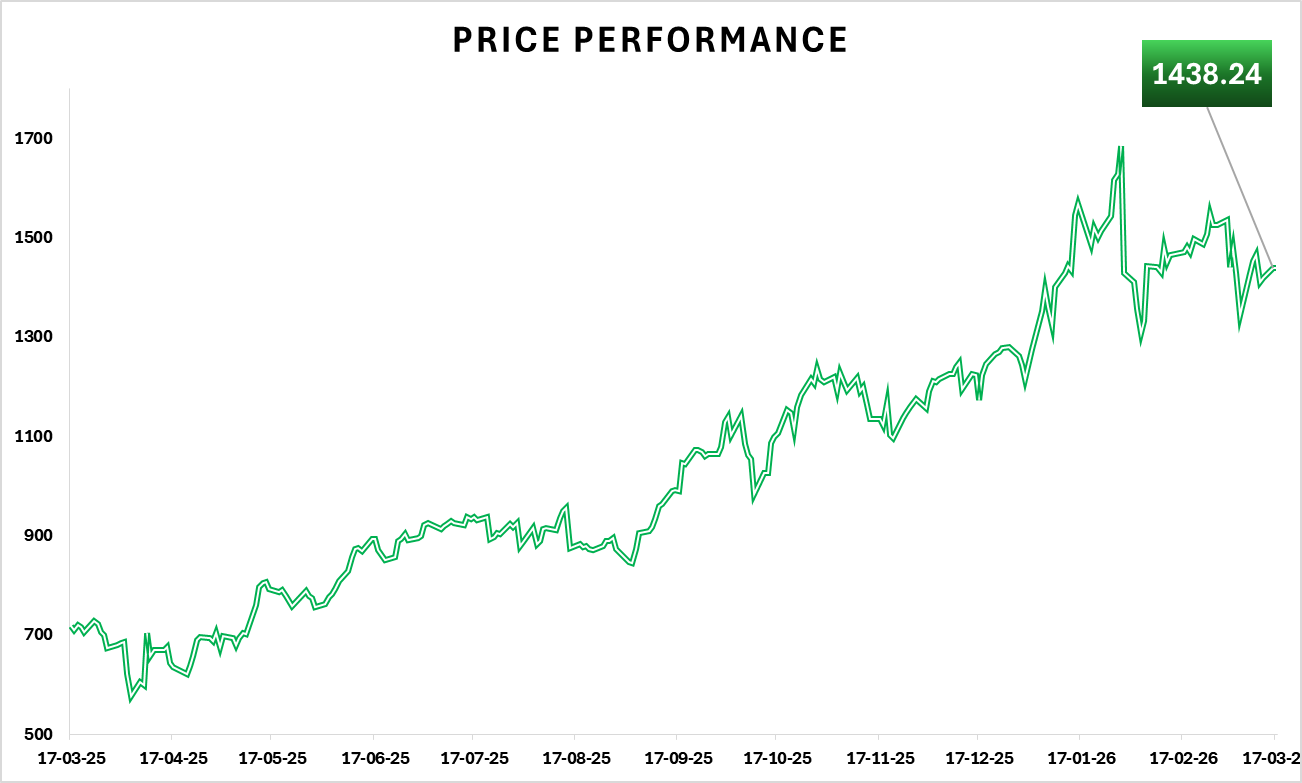

Price and valuation context

KLA ended the day at $1,438.24. The stock was up 15.85% over three months and 18.37% year to date, but it was up 1.38% on the most recent day, up 0.64% over five days, and down 1.77% over a month. That indicates that, despite a recent slight decline, the stock has already seen a significant shift.

The shares are well above the 52-week low of $551.33 but still below the 52-week high of $1,693.35. 954,922 shares were traded, slightly below the 20-day average of 1,091,012. So there is no sign here of unusual panic or euphoria in the most recent session.

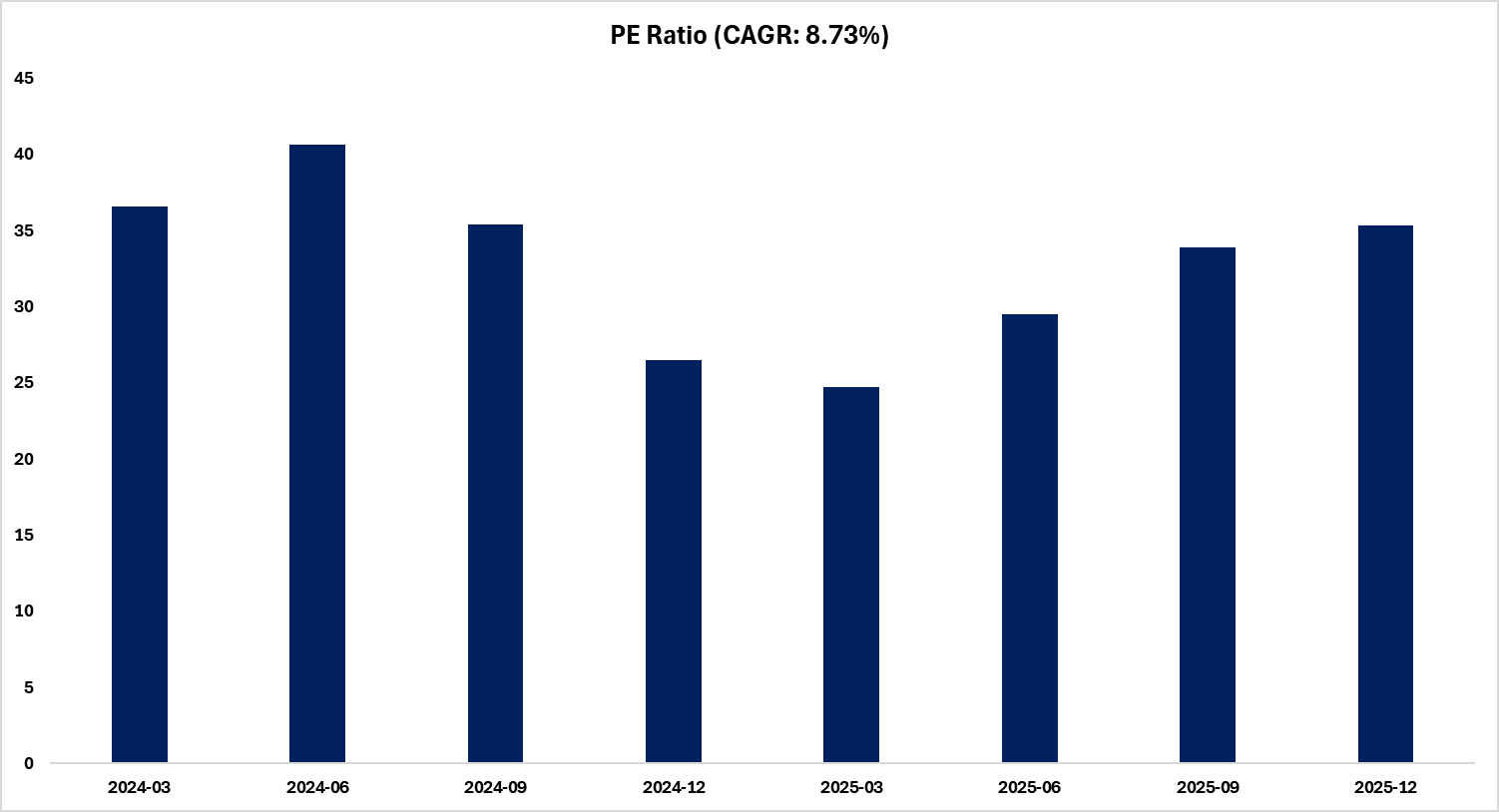

With EV/Sales at 14.66x and P/FCF at around 42.7x, KLA is valued at 41.85x trailing profits and 30.67x prospective earnings. That setup on basic multiples is not inexpensive. In addition to indicating that investors are already paying for a robust company, the lower forward P/E relative to the trailing P/E suggests that the market still anticipates future profit growth. With around $2.45 billion in cash, $2.76 billion in marketable securities, and $5.89 billion in long-term debt in the quarterly report, the balance sheet appears reasonable rather than cash-rich. However, your value summary places net debt at about $0.90 billion.

Risks

The primary concern is that KLA remains dependent on semiconductor capital expenditures, which can fluctuate even when long-term demand appears robust. KLA may rapidly see a slowdown in client expenditure on sophisticated production capabilities. The results announcement also discusses company-specific risks connected to trade regulations, China-related constraints, concentrated clients, and wider fluctuations in technology demand. Furthermore, even a strong quarter might not be sufficient if investors begin to fear that future growth would decelerate due to the stock's premium valuation.

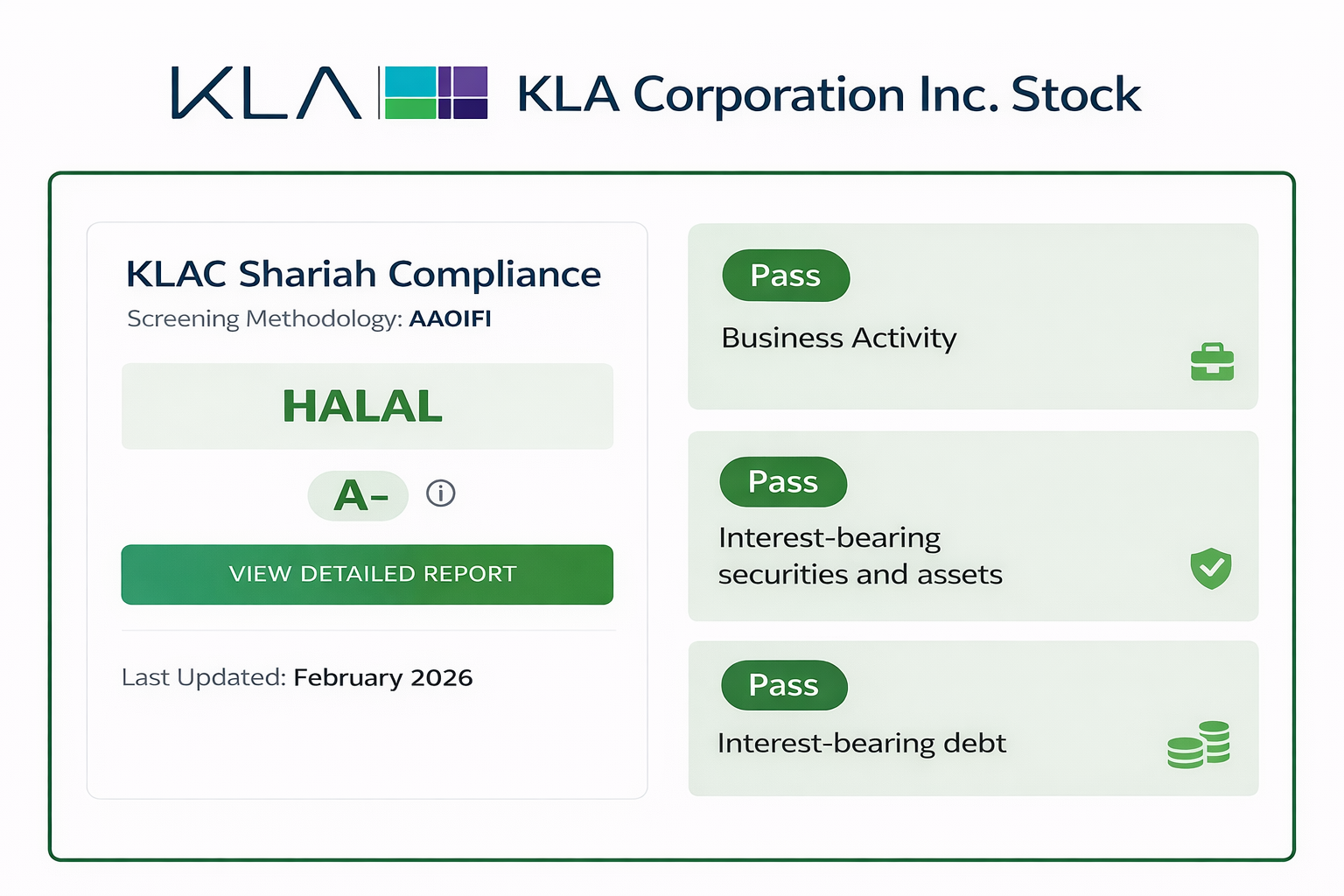

Shariah Compliance Lens

For investors reviewing Shariah-compliant stocks KLAC, as of February 2026, KLA (KLAC) is classified as Shariah-compliant (Halal) with an A- Musaffa rating based on the Shariah Screening results at Musaffa. KLAC’s 2026 2nd Quarter Report was used to conduct the screening analysis in line with the AAOIFI methodology. KLAC passed all three required screening thresholds, with 98.83% of its business activity meeting the permissible (Halal) threshold (0.00% doubtful and 1.17% not Halal). Both interest-bearing securities (5.79%) and interest-bearing debt (6.13%) remain below 30% of the 36-month average market capitalization.

Conclusion

The notion that KLA is still one of the more obvious infrastructure options in the semiconductor business is supported by the company's most recent quarter. Earnings exceeded revenue, cash creation remained robust, and the projection was consistent. Now, the crucial question is whether the business can continue to generate enough steady growth from AI-driven semiconductor investment to support a still-demanding price.

Sources

- KLA Corp. Stock Analysis

- KLA Corp Stock News from GuruFocus

- KLA Corp

- KLA Corporation Reports Fiscal 2026 Second Quarter Results

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed