Lam Research Corp (LRCX, A-, Halal) is a major global player in the supply of wafer fabrication equipment and services for making semiconductors (computer chips). They focus on the high-precision steps of plasma etching, thin film deposition, and wafer cleaning to help chip manufacturers produce smaller, faster, and more powerful electronic products. The current market capitalization is $293.23 billion, with the current Lam Research stock price at $212.2.

Shariah Status

For investors reviewing Shariah-compliant stocks, LRCX is considered halal, with an A rating under AAOIFI standards, as screened by Musaffa. The company's business activities were shariah-compliant, with 98.55% of revenue from halal activities and 1.45% from non-halal sources, including interest income and other income. Interest-bearing assets and debt accounted for 5.39% and 3.91%, respectively, which were below the 30% threshold considered shariah-compliant. More information is available here.

Business Analysis

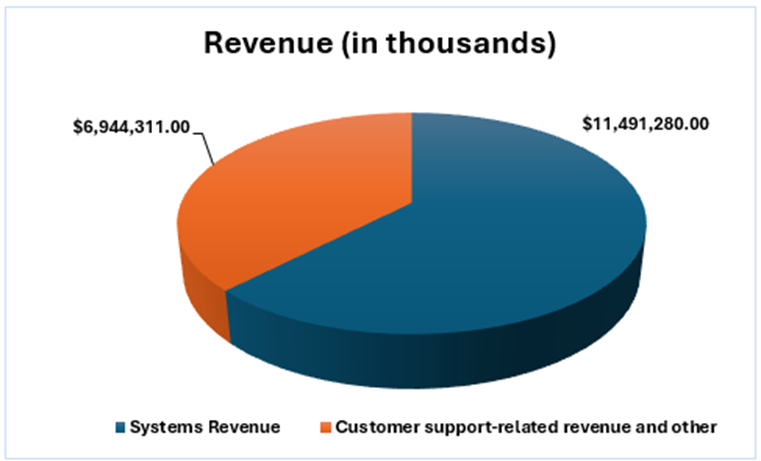

For FY 2025. The company recorded total revenue of $ 18.44 billion, a 24% increase over the previous fiscal year. The revenue came from two segments: Systems, which accounted for about 62% ($11.49 billion) of total sales, and the Customer Support Business Group (CSBG), which accounted for the remaining 38% ($6.94 billion). The overall revenue growth was mainly due to the boom in global AI infrastructure, which has created strong demand for High-Bandwidth Memory (HBM) and advanced logic chips. Revenue in the Systems segment was up, as Lam's etching and deposition tools are essential for building complex 3D structures used in AI processor designs and for developing next-generation Gate-All-Around (GAA) transistors (Yahoo Finance). Meanwhile, the company's CSBG segment hit record highs as its "installed base" exceeded 100,000 active machines, naturally leading to higher demand for replacement parts and upgrades.

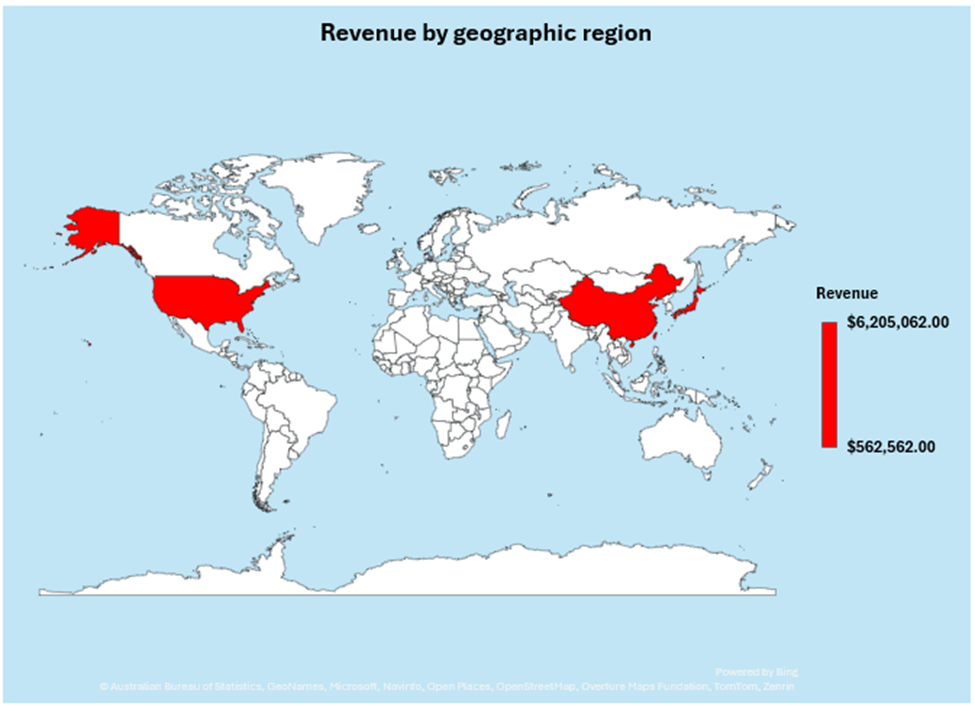

In fiscal year 2025, Lam Research derived about 94% of its revenue from international sales, with China again being its largest geographic segment at 34% ($6.21 billion) of total sales. This was due to its dominance in China, which was fueled by strong demand for "mature node" specialty chips in the automotive and industrial markets. Korea was the second-largest market at 22% ($4.13 billion), with a staggering 44% jump due to the memory giants Samsung and SK Hynix increasing their output of AI-critical High-Bandwidth Memory (Counterpoint). Taiwan was the third-largest market at 19% ($3.45 billion), with revenue more than doubling from the previous year, driven by strong investment in next-generation transistor technology by leading-edge foundries. Japan was the fourth-largest market at 10% ($1.88 billion). In comparison, the United States and Europe were smaller markets at 7% and 5%, respectively, as most of the physical chip manufacturing was still done in Asia.

Taiwan was the third-largest market at 19% ($3.45 billion), with revenue more than doubling from the previous year, driven by strong investment in next-generation transistor technology by leading-edge foundries. Japan was the fourth-largest market at 10% ($1.88 billion), while the United States and Europe were smaller markets at 7% and 5%, respectively, as most physical chip manufacturing was still in Asia.

Taiwan was the third-largest market at 19% ($3.45 billion), with revenue more than doubling from the previous year, driven by strong investment in next-generation transistor technology by leading-edge foundries. Japan was the fourth-largest market at 10% ($1.88 billion), while the United States and Europe were smaller markets at 7% and 5%, respectively, as most physical chip manufacturing was still in Asia.

Financial analysis

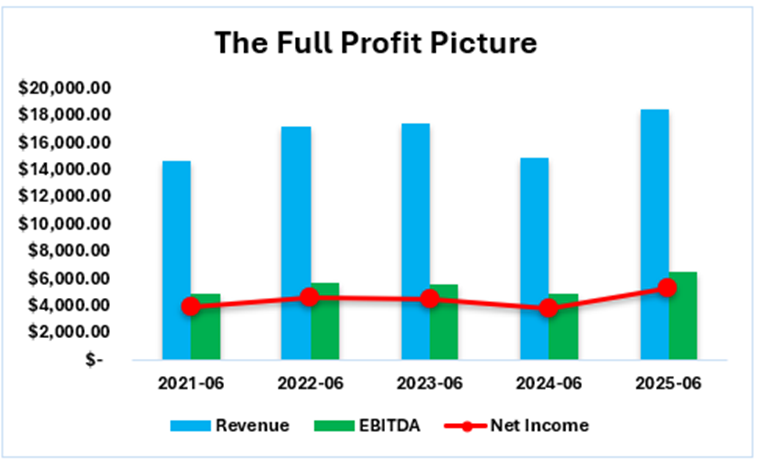

The company experienced a sharp revenue decline in 2024, followed by a record-breaking recovery in 2025. Its revenue was lower in 2024 chiefly due to a global semiconductor slump and a post-pandemic drop in demand for personal electronics. In addition, several factors affected the company's revenue, including the memory market crash, inventory buildup, and export restrictions. In 2024, increasing U.S. export controls led to limited sales of advanced systems to China, which had a huge impact on the company's revenue. In 2025, Lam Research saw a significant increase in revenue driven by high demand for AI & HBM, foundry technology transitions, and service growth. The huge demand for AI chips requires huge quantities of High Bandwidth Memory (HBM). Lam’s high-precision etch tools are the industry standard for manufacturing these complex 3D memory structures (MLQ).

Turning to the company's net income and EBITDA, they increased significantly due to strong revenue recovery. Net income rose to $5.36 billion in FY 2025, a 40% increase from $3.83 billion in FY 2024. The major causes of this profit surge were increased sales volume and effective cost management. EBITDA increased to $6.29 billion in FY2025, indicating a 36% increase compared to $4.63 billion in FY2024.

Earnings Analysis

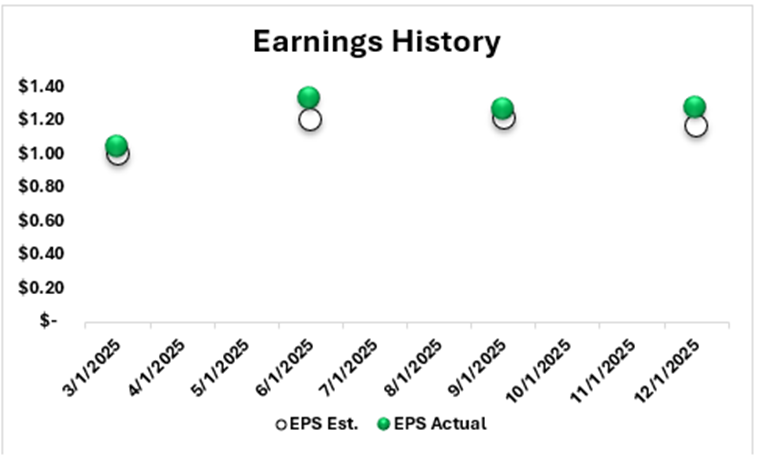

In its most recent earnings, Lam Research beat market expectations over the last four quarters, primarily due to a massive surge in AI-driven demand for High-Bandwidth Memory (HBM) (Counterpoint). The company’s specialized etching tools are essential for stacking these AI chips, leading to higher sales volumes than analysts initially projected.

Additionally, revenue remained surprisingly resilient in China, where customers invested heavily in mature-node technology despite U.S. export restrictions. Performance was further boosted by the Customer Support segment, which generated high-margin recurring revenue as its global footprint grew to over 100,000 active machines. Finally, a shift toward more complex Gate-All-Around (GAA) chip designs forced manufacturers to buy more of Lam's equipment per wafer, resulting in better-than-expected profit margins.

Valuation Analysis

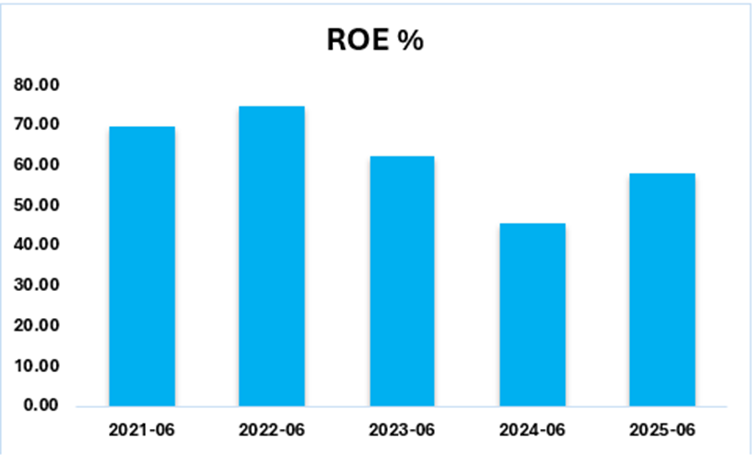

The Return on Equity for Lam Research declined in 2024 and rose considerably in 2025, mainly due to the cyclical nature of the semiconductor industry and the subsequent AI-driven recovery (MLQ). As mentioned above, the company’s net income decreased by roughly 15% because of a severe slump in memory spending by major customers in 2024. As a result, ROE also dropped. In 2025, the ROE rebounded to 58.2% as the company capitalized on several growth drivers, including a surge in profitability, demand for AI infrastructure, and capital returns.

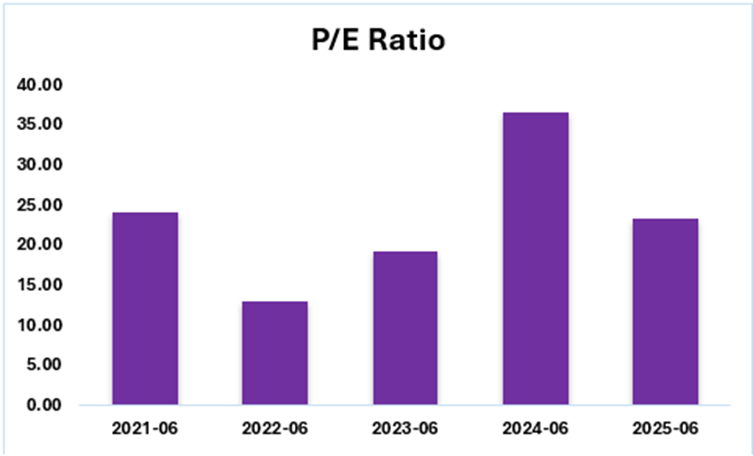

In 2024, Lam Research’s P/E ratio rose to around 36x because the company’s earnings declined more than its stock price. At this time, the semiconductor industry's decline caused the company’s net income to fall to 3.83 billion, but the anticipation of the AI boom kept its stock price high, thereby increasing its P/E ratio (VP Bank). In 2025, Lam Research’s P/E ratio declined to around 23x as earnings growth outpaced the company’s rising stock price. At this time, the company’s net income grew 40 percent to 5.36 billion due to the boom in High-Bandwidth Memory (HBM) and other chip designs, "normalizing" the company’s valuation so that its stock price appears relatively low compared to its earnings (Macrotrends).

In 2024, Lam Research’s P/E ratio rose to around 36x because the company’s earnings declined more than its stock price. At this time, the semiconductor industry's decline caused the company’s net income to fall to 3.83 billion, but the anticipation of the AI boom kept its stock price high, thereby increasing its P/E ratio (VP Bank). In 2025, Lam Research’s P/E ratio declined to around 23x as earnings growth outpaced the company’s rising stock price. At this time, the company’s net income grew 40 percent to 5.36 billion due to the boom in High-Bandwidth Memory (HBM) and other chip designs, "normalizing" the company’s valuation so that its stock price appears relatively low compared to its earnings (Macrotrends).

Risks

Several risks will affect the company's business activities. That is why they should be considered by investors when making investment decisions.

1. A major source of revenues comes from China, but export restrictions from the U.S. are limiting the sales of advanced technology to China. The company estimates that export restrictions could impact 2026 sales by $600 million.

2. Lam Research depends on a few large customers. The loss of a single major customer or a decrease in their spending can significantly impact the firm's total revenue (Tradingview).

3. The company also faces stiff competition from other global leaders like Applied Materials and Tokyo Electron. If a competitor develops a better product for etch or deposition tools, Lam might lose market share in those segments.

Conclusion

Lam Research is a leading semiconductor manufacturing equipment company with robust growth prospects due to increasing demand for AI Chips and High-Bandwidth Memory. The company has witnessed robust financial performance in FY 2025, with sharp increases in revenue, net income, and EBITDA, driven by the semiconductor market downturn in 2024. Furthermore, the company's business activities are in accordance with the AAOIFI Shariah Screening criteria. However, investors need to consider risks associated with the company, including export restrictions that may affect sales in China, dependence on a few major customers, and stiff competition from peers such as Applied Materials and Tokyo Electron. Nevertheless, Lam Research has robust prospects for tapping the global semiconductor and AI markets.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed