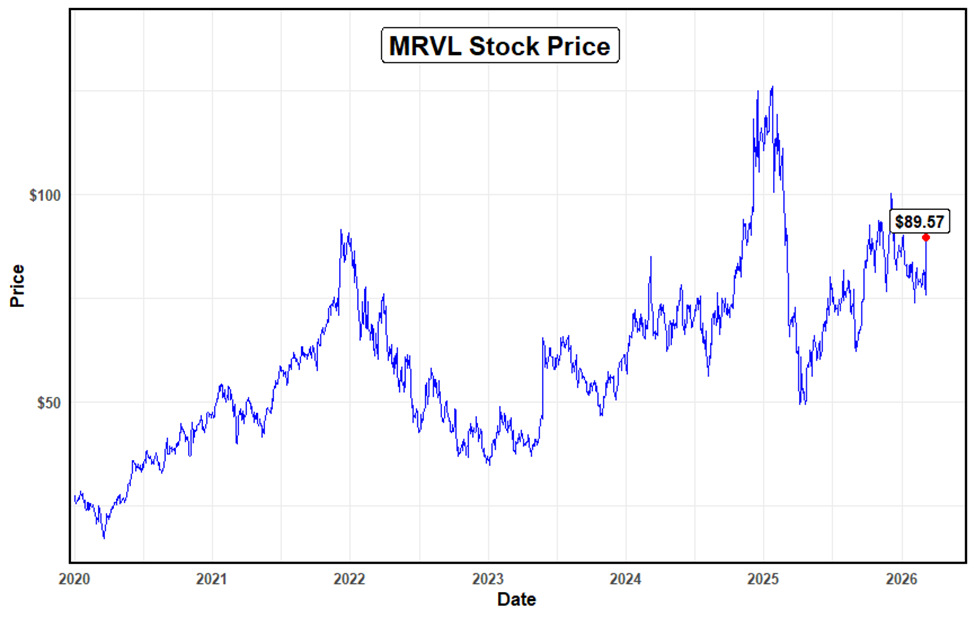

Marvell Technology (MRVL, A-, Halal) is a leading American semiconductor company that develops and supplies data infrastructure chips and silicon solutions, with a major focus on accelerating data centers for AI, networking, and storage. It engages in the design, development, and sale of integrated circuits. The company's market capitalization is $66.93 billion, and its current Marvell Technology stock price is $89.57.

Shariah Status

The company’s Shariah status is considered Halal with a rating of A-, according to the AAOIFI screening methodology analyzed by Musaffa. From the business activity perspective, the company’s compliant income accounted for 99.23% of total revenue, while 0.77% was recorded as non-compliant revenue because of the company’s interest income. Interest-bearing assets and liabilities accounted for 4.45% and 7.33%, respectively, which are below the 30% standard threshold. More calculations are provided there.

Business Analysis

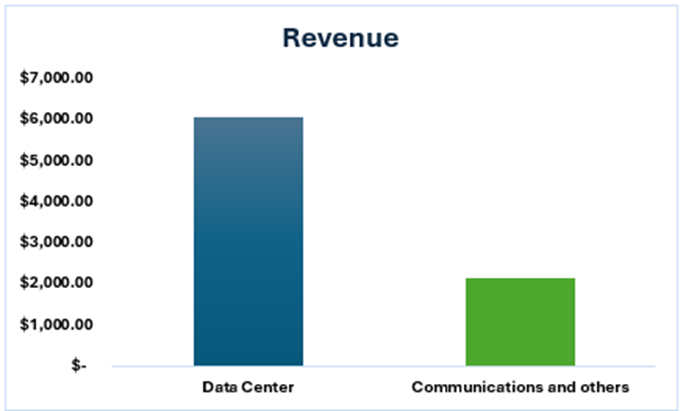

The company generates its main revenue from two segments: Data Center and Communications and Others. Its total revenue amounted to $8.195 billion, representing a 42% year-over-year increase, while the Data Center segment accounted for 74.4% of the total. The Data Center segment is the company's main revenue driver, and Marvell Data Center revenue increased this year due to demand for AI, including custom AI silicon (XPUs), electro-optics, and networking switches.

There are several reasons why the Data Center segment’s revenue increased in 2026. During the year, revenue from custom-designed chips for major cloud clients doubled, and Marvell is now engaged in over 50 new custom opportunities. Likewise, there was strong demand for high-speed optical interconnects (800G and 1.6T), which move data between AI processors. Deals involving Celestial AI and XConn expanded the company’s addressable market for high-speed AI connectivity. As a result, the company’s revenue rose significantly in FY 2026 (Nasdaq).

Financial analysis

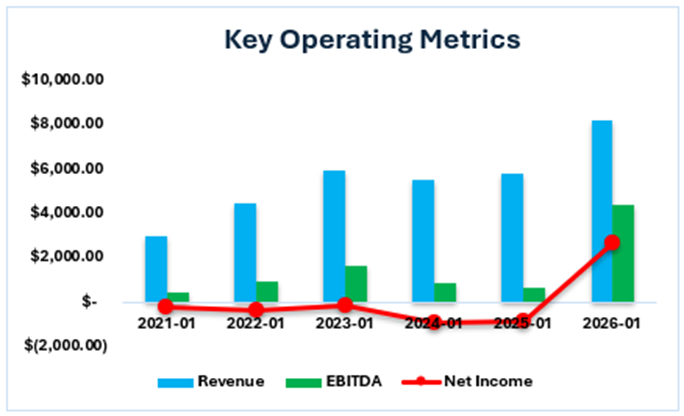

During FY 2024–2025, Marvell faced severe headwinds in its traditional markets, which offset early AI gains. Customers in the company’s enterprise networking and carrier infrastructure markets had excess chip inventory from a buying spree during the pandemic, resulting in a sharp drop in new orders (Telecom). In addition, the company maintained high spending on Research and Development (R&D)—almost $2 billion annually—to develop next-generation AI chips. As a result of lower revenue and high R&D expenses, the company incurred GAAP operating losses.

Read More:

- The Rise of DoorDash: Q4 Results, Expansion, And Challenges

- Moody’s 2026 Guidance Highlights AI Tailwinds—and the Real-Time Credit Cycle

EQIX Q4 Earnings: Revenue, EBITDA Beat? AI Hyperscale & 2026 Outlook

Turning to EBITDA and Net Income, both were lower in 2025, and the company incurred net losses over the last two years. The reason for the lower EBITDA in 2025 was mainly lower overall revenue and higher R&D intensity relative to sales. In 2026, net income was significantly boosted by the 2025 sale of its Automotive Ethernet business to Infineon. In addition, EBITDA improved due to strong operating leverage.

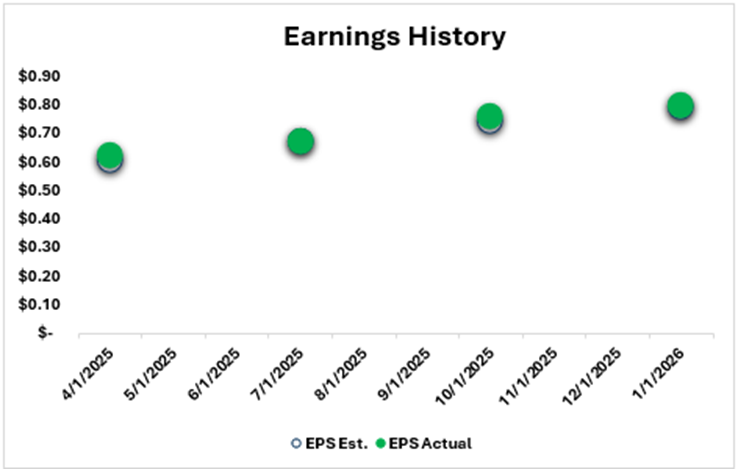

Marvell Technology has consistently outperformed market expectations over the last four quarters, primarily due to strong growth in demand for AI infrastructure and in the Data Center segment. In FY 2026, the company’s Data Center revenue rose significantly, driven by hyperscalers such as Amazon and Google ramping up spending on AI clusters. Moreover, Marvell’s custom chip business doubled in fiscal 2026, enabling the company to exceed market expectations in the recent MRVL earnings.

There are also company expectations for the first quarter of FY 2027:

First Quarter of Fiscal 2027 Financial Outlook

- Net revenue is expected to be $2.400 billion ± 5%.

- GAAP gross margin is expected to be 51.4% to 52.4%.

- Non-GAAP gross margin is expected to be 58.25% to 59.25%. (Marvell)

Valuation analysis

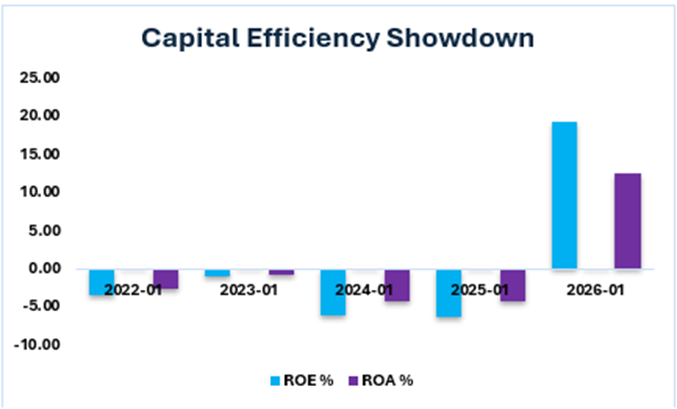

The company’s ROE and ROA were negative over the last four years due to GAAP net losses, but they suddenly turned positive in FY 2026, driven by a one-time multi-billion-dollar gain and a massive surge in AI-driven revenue (Tradingview). In addition, there were significant non-cash expenses related to prior acquisitions, including the amortization of intangible assets and stock-based compensation.

However, in FY 2026, the sale of its Automotive Ethernet business to Infineon on August 14, 2025, was the single biggest driver of gains, significantly increasing net income (Marvell). As a result, the company’s ROE and ROA also surged during this fiscal period.

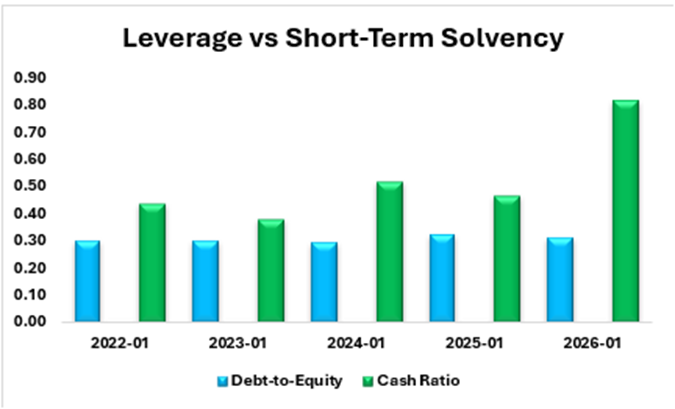

Marvell Technology’s Debt-to-Equity ratio and cash ratio are below 1 due to its conservative capital structure and cash-management strategy for investments in high-growth opportunities, such as Artificial Intelligence. This indicates that the company relies more on equity than on debt to finance its operations. According to the latest report, the company’s total equity amounted to $14.31 billion, while total debt stood at about $4.47 billion (Marvell). This indicates management’s commitment to a conservative financial policy and periodic debt reduction.

A cash ratio of less than 1 means the company does not have enough cash to cover all its immediate short-term debts. Marvell recorded $2.64 billion in cash and equivalents in FY 2026, while its total current liabilities were $3.22 billion. Instead of holding excess cash, the company aggressively allocates capital to R&D on AI chips and to shareholder returns (Marvell).

Risks

There are several risks that investors should consider when making decisions about the company and its stock:

1. A huge portion of Marvell’s growth is directly related to a handful of “hyperscale” accounts, such as Amazon, Google, and Microsoft. A reduction in CapEx by any of these giants would directly affect Marvell’s revenue growth.

2. After selling its automotive business unit, Marvell Technology is now less diversified. The Data Center segment is expected to account for more than 80% of total revenue in the coming years. Therefore, the company is extremely vulnerable to a cyclical downturn in the AI sector (Marvell).

3. Marvell’s growth strategy depends on acquisitions, such as Celestial AI and XConn Technologies. If these acquisitions are not successfully integrated or the expected synergies are not achieved, profitability may be adversely affected(Marvell).

Conclusion

When evaluating MRVL stock among semiconductor stocks, Marvell Technology has strong growth potential due to rising demand for AI infrastructure and its expanding Data Center segment. The company's financial performance improved in the 2026 financial year, driven by AI revenue growth and the sale of its Automotive Ethernet business. From the Shariah perspective, the company qualifies under the AAOIFI screening criteria as its revenue comes from Shariah-compliant activities. However, the risk factors to consider when investing in the company include its dependence on major cloud customers and a lack of diversification.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed