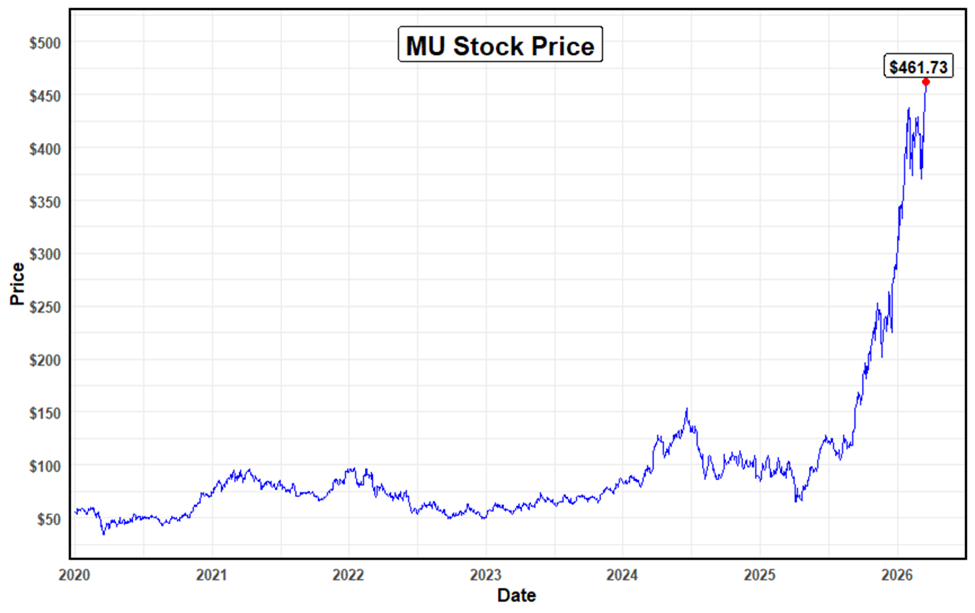

Micron Technology (MU, B, Halal) is a leading American manufacturer of computer memory and data storage solutions, including DRAM, NAND flash, and NOR memory, serving the AI, data center, automotive, and mobile industries. The company produces high-performance memory chips, SSDs, and modules. The company’s current market capitalization is $466.95 billion, with a MU stock price of $461.73 per share.

Shariah Status

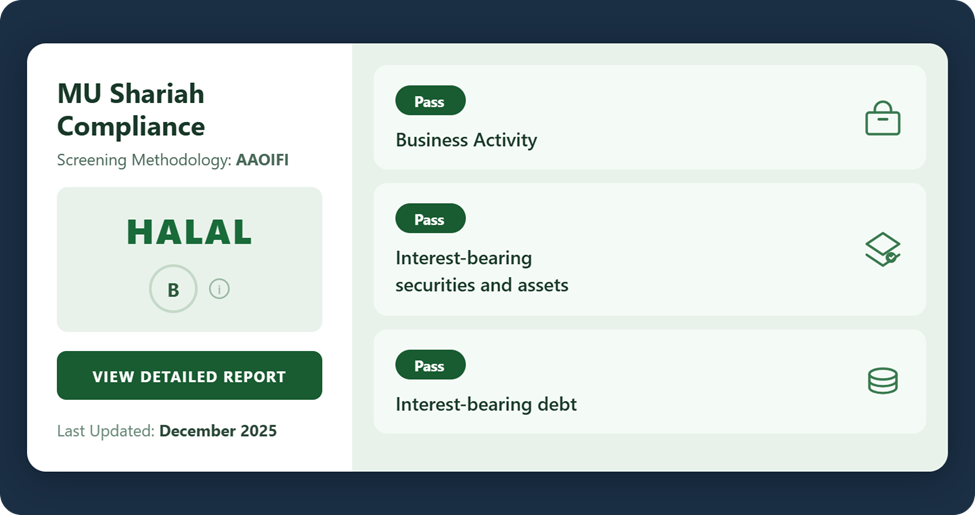

The Shariah status of Micron is considered halal, with a ranking of B according to the AAOIFI screening methodology by Musaffa. According to the screening results, 98.99% of its business activity is recorded as Shariah-compliant, while 1.01% is not halal due to interest income. Interest-bearing securities and debt account for 10.57% and 10.34% of its assets and liabilities, respectively.

Financial Performance and Revenue Growth

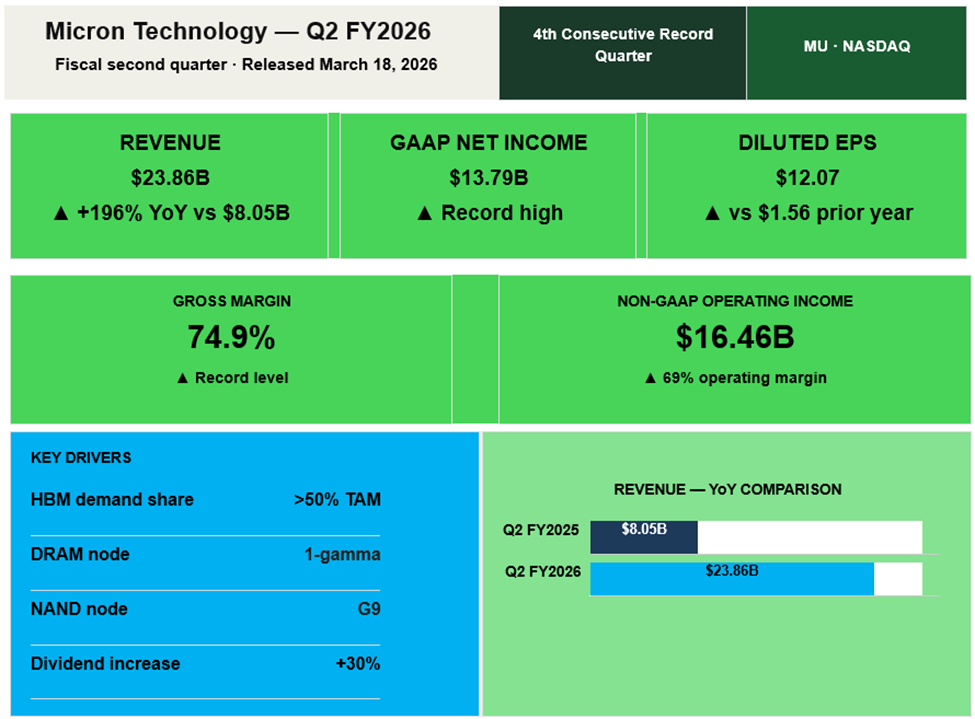

The fiscal second-quarter 2026 results announced by Micron Technology on March 18, 2026, mark a historical peak in the company’s financial performance, attributable to a fundamental shift in memory as a strategic resource amid the AI revolution (Micron). This Micron Q2 FY2026 earnings report underscores why MU stock has emerged as the standout memory chip stock of the current AI cycle.

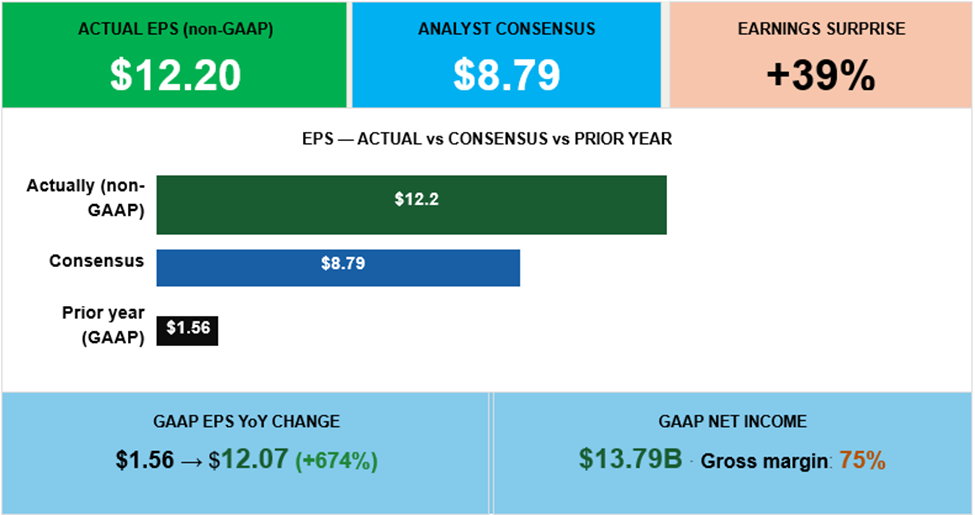

The company reported a new revenue record of $23.86 billion, nearly tripling from $8.05 billion in the same period last year, marking the fourth consecutive record-breaking quarter (Micron). The main driver behind this significant Micron revenue growth was the “memory crunch” driven by the AI revolution, where High Bandwidth Memory (HBM) and Micron data center demand pushed bit demand to surpass 50% of the total available market for the first time (Micron). This enabled Micron to achieve a new record in GAAP net income of $13.79 billion, or $12.07 per diluted share, nearly eight times higher than the previous year’s $1.56 per share (Micron).

Earnings Per Share (EPS) Performance

Micron Technology exceeded market expectations for the second quarter of fiscal 2026. It posted a record non-GAAP diluted earnings per share of $12.20, representing a 39% positive surprise over the consensus estimate of $8.79 per share (Micron). This historic achievement was driven by GAAP net income of $13.79 billion, or $12.07 per diluted share, a significant increase compared to the year-earlier period’s $1.56 per share (Micron).

Operational Drivers and Profitability Factors

These impressive results were mainly due to the “fundamental recasting of memory as a strategic AI asset,” which enabled Micron to benefit from a severe industry-wide supply shortage for its high-margin products, such as HBM3E and HBM4 (Micron). Furthermore, the company achieved mature manufacturing yields on its advanced 1-gamma DRAM node ahead of any previous generation, allowing it to ship more premium-priced products and achieve an unprecedented gross margin of 75% (Micron).

The company also meets expectations for the third quarter of fiscal 2026. It indicates that future results are expected to be higher than current results, which is a positive sign for investors.

FQ3-26 GAAP Outlook |

Revenue $33.5 billion ± $750 million |

Gross margin Approximately 81% |

Operating expenses Approximately $1.60 billion |

Diluted earnings per share $18.90 ± $0.40 |

Investment Risks

Even though the company has strong financial results, there are several risks that investors should consider when making investment decisions:

1.Micron has already raised its CapEx guidance for the 2026 financial year to more than $25 billion, with a planned increase of an additional $10 billion in the 2027 financial year. This high level of spending makes earnings more volatile, and there is a risk if an “AI winter” occurs before these investments generate returns (Seeking Alpha).

2.The memory market remains cyclical. As competition increases, there is a looming threat of oversupply in the market by 2027–2028, which may cause a decline in prices.

3.Ongoing conflicts, such as those in the Middle East, are a threat to critical inputs such as helium, which is required for semiconductor lithography and is supplied in 30-38% by Qatar (Seeking Alpha).

Conclusion

Overall, Micron Technology has shown impressive financial performance, with high demand for memory solutions in AI and data centers driving this performance. The fact that the company has achieved record-breaking revenues, earnings, and margins underscores its position in the market. Moreover, as it is Shariah compliant with a B rating, it could be a good investment option for Islamic investors. However, investors should be careful as there are various risks, such as high capital costs, which could affect the company’s performance in the future.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed