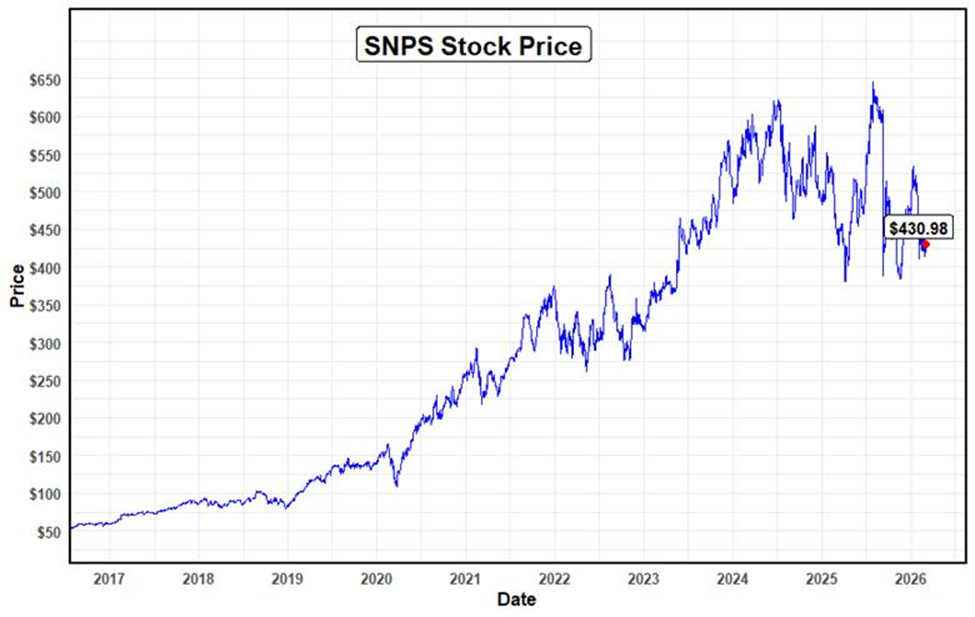

Synopsys, Inc (SNPS, B, Halal) is a global leader in Electronic Design Automation (EDA), semiconductor intellectual property (IP), and software security, providing tools that enable engineers to design, verify, and manufacture silicon chips and software systems. The company supplies mission-critical electronic design automation (EDA) software that engineers use to design and test integrated circuits (ICs). The company's current market capitalization is $88.98 billion, with Synopsys stock trading at 430.98 per share.

Shariah Status

For investors reviewing Shariah-compliant stocks SNPS, the Shariah status of the company, according to the AAOIFI screening methodology calculated by Musaffa, is considered Shariah-compliant, with a ranking of B. 98.96% of its business activity is classified as halal. In comparison, only 1.04% of that was not halal because of interest income. However, while investing in this company, investors should purify this “not halal” revenue using the purification calculator of Musaffa. When it comes to interest-bearing securities, assets, and debt, they also accounted for 3.85% of assets and 17.53% of liabilities. To get more information and calculations, you may find them there.

Business analysis

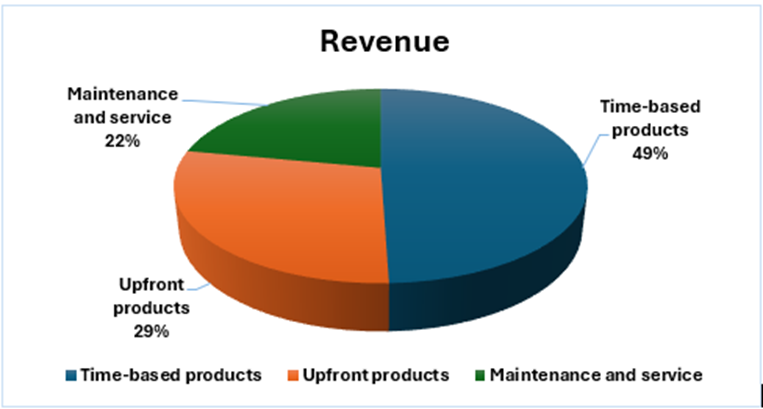

The company generates most of its revenuefrom two core business segments: product revenue and maintenance and services. Its product revenue is primarily derived from two business segments: Design Automation and Design IP. These segments create income through software licenses, hardware sales, and integrated semiconductor designs. The Design Automation segment provides software and hardware tools for designing and testing integrated circuits. The Design IP segment involves licensing pre-designed functional blocks, which customers integrate into their own chips to enhance development (Synopsys). The company reached a record annual revenue of $7.054 billion in fiscal year 2025. This rise in product revenue mainly came from the Synopsys Ansys acquisition merger, which immediately boosted the top line and closed in July 2025. This acquisition contributed nearly $756.6 million to total revenue in FY 2025. In addition, growth in product revenue was driven by record shipments of hardware systems such as ZeBu Server 5 and HAPS-200.

The company’s maintenance and service revenue includes recurring fees for software updates and technical support. It accounted for 22% of total revenue in FY 2025, generating $1.55 billion.

Financial Analysis

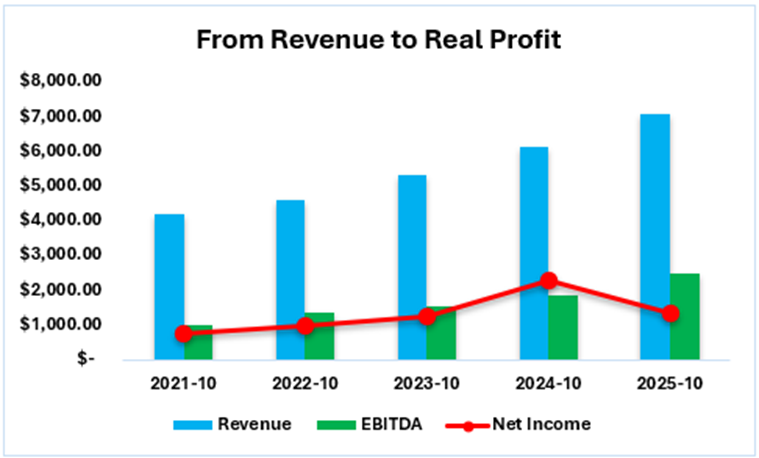

The company reported EBITDA of about 2.5 billion, while GAAP net income declined sharply to $1.33 billion in fiscal year 2025. This was caused by massive one-time and non-cash expenses related to the $35 billion acquisition of Ansys. In 2024, Synopsys’s net income was even higher than EBITDA because of a major one-time gain from discontinued operations. EBITDA only measures the performance of continuing operations and excludes such one-time investment gains. In 2024, the company’s Software Integrity business was finalized as part of a strategic shift to focus on its core EDA and IP segments (Cleary Gottlieb). The company also witnessed record growth, with revenue increasing to $7.054 billion because of high-demand technology trends and a major acquisition.

Earnings history

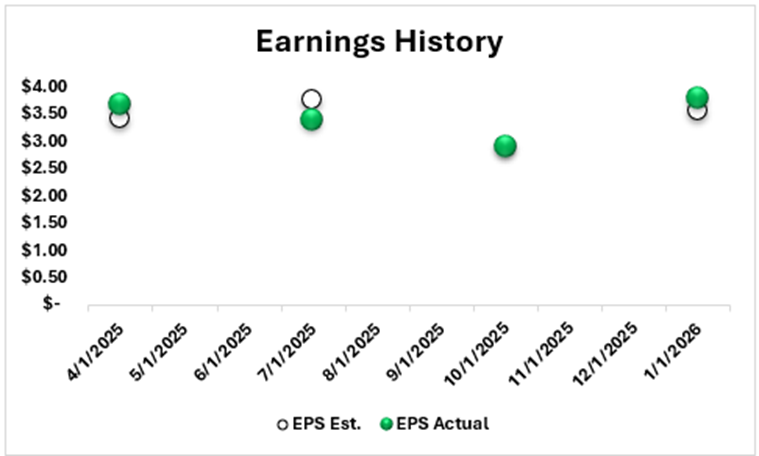

Reviewing the Synopsys FY 2025 results, over the last year, the company's earnings performance was mixed, including a major miss in 2025. According to Synopsys' Q3 earnings report for FY2025, the company missed market expectations. Adjusted EPS was $3.39, falling 10.6% short of the $3.75 forecast. This happened because of a decline in Design IP revenue and significant Ansys acquisition-related costs (Investing). For Q4 results, the company surpassed market expectations, with actual EPS of $2.9 versus the $2.88 consensus. Likewise, the last earnings report showed that Synopsys posted a major beat, with EPS of $3.77, exceeding the market and analyst estimates of $3.56. The main reason for this beat is the acquisition of Ansys, which significantly increased revenue, contributing $886 million in Q1 FY 2026 (Investing). Another reason may be the company's massive backlog, which stood at $11.3 billion, providing strong financial visibility and supporting guidance raises (Futurum).

The company also expects several financial statements for FY 2026 (Synopsys).

Revenue- $9.56-$9.66 billion

Non-GAAP EPS - $14.38- $14.46

GAAP Expenses- $8.46- $8.60 billion

The estimations show positive signs, which will be useful for further investment decisions about the company.

Valuation analysis

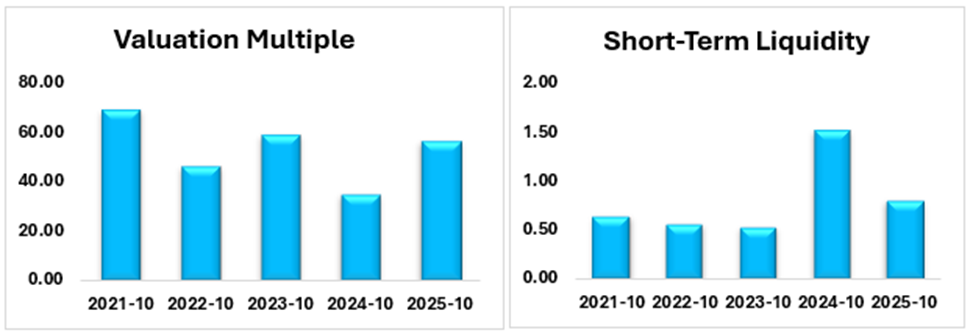

In 2024, the company's P/E ratio was lower than in other fiscal years. One reason is that the company reported a considerable increase in its annual EPS, which led to a decline in its P/E ratio. In addition, the stock price showed a nearly 17% year-to-date return, leading to a lower multiple as earnings growth increased. For FY 2025, EPS dropped sharply due to higher expenses and integration costs from the Ansys deal, resulting in a lower P/E ratio. The company also ended 2024 with a robust liquidity position, reporting a net change in cash of $2.46 billion from the sale of its Software Integrity business (Synopsys).

Moreover, the company's total liabilities were about 44.05 billion, resulting in a high asset-to-liability ratio of 3.23. Because of these reasons, the company’s cash ratio increased considerably in 2024. However, the acquisition of Ansys involved significant cash outlay while the company expanded its debt to fund its strategic expansion in FY 2025. As a result, the company’s cash ratio again dropped.

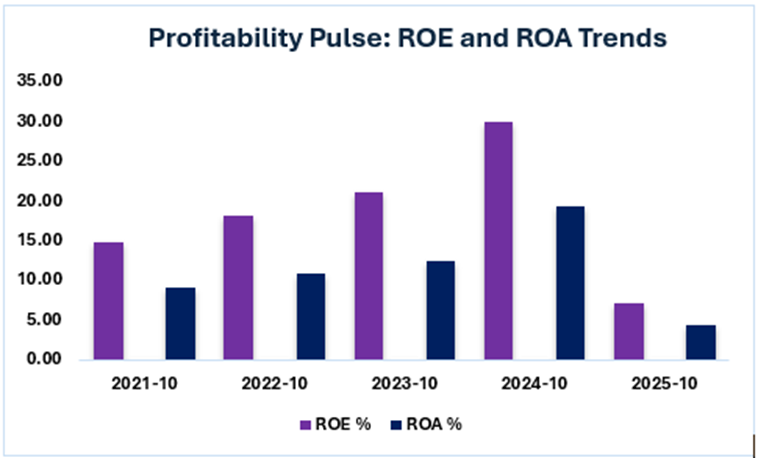

In 2025, the company's ROA declined sharply from its 2024 peak to a low level, following the massive expansion of its asset base after the Ansys acquisition. As mentioned above, the company's GAAP net income increased noticeably, leading to a significant increase in its ROA in 2024. The scenario was the same for ROE, which increased due to higher net income, a lower equity base, and the company's high efficiency in FY 2024.

Even though ROA and ROE decreased in 2025, this does not mean the company failed. The company is trading its short-term efficiency and liquidity for a massive long-term expansion through the $35 billion Ansys acquisition (Synopsys).

Read More:

- Inside Snowflake (SNOW): AI Growth, Financial Strength & Risks

- MongoDB posts strong Q4 results, but shares pressured by slower growth outlook.

- Salesforce (CRM): The stock is trading on "what's next," despite a strong quarter.

Risks

Several risks should be considered when deciding on the company:

1.About 10%–14% of the revenue of the company is related to China. The mid-year “broad ban” on sales in 2025 was repealed in July 2025, but the region remains volatile due to changing U.S. export controls on AI and advanced chip design software (CNBC).

2.Part of the value proposition of the merger is the planned launch of the first software suite, which will be available in the first half of 2026. Delays in integrating Ansys-developed multiphysics tools with Synopsys-developed EDA tools could allow competitors, such as Cadence, to gain ground (Synopsys).

3.The $13.5 billion in debt for Synopsys (SNPS) resulting from the acquisition of Ansys is a risk for Synopsys because it requires the company to focus on paying off debts instead of investing in growth-oriented opportunities (Yahoo Finance).

Conclusion

In conclusion, mapping out the SNPS stock forecast, Synopsys Inc. is a major semiconductor design software and IP solutions company with robust financial growth due to increasing demand for AI-driven chip design solutions. Although it has been under financial pressure due to the acquisition of a major company, Ansys has robust long-term growth prospects, with high backorders and positive growth ahead. As it has been given a halal Shariah status by Musaffa screening, it may be considered for investment by Shariah-conscious investors after considering all risks, including geopolitical issues and rising debt.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed