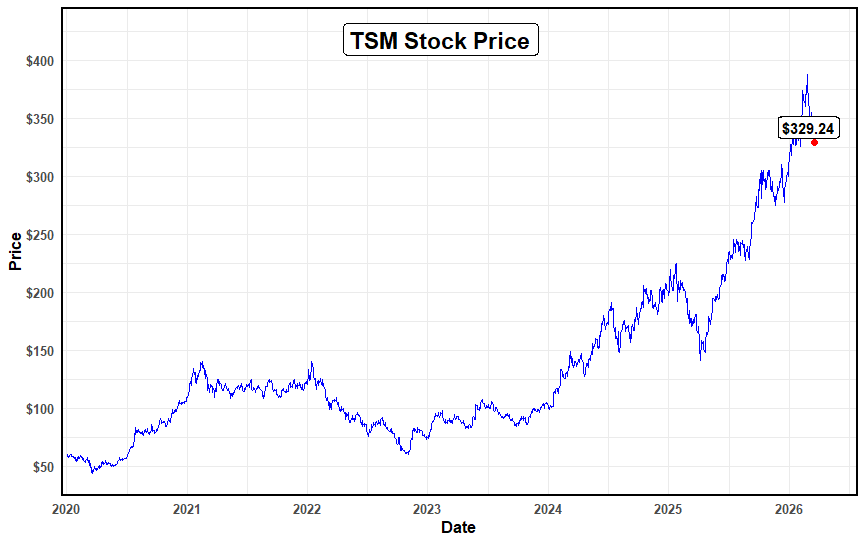

Taiwan Semiconductor Manufacturing Co., Ltd (TSM, B, Halal) engages in the manufacture and sale of integrated circuits and wafer semiconductor devices. The company is headquartered in Hsinchu, Hsinchu. The integrated circuit manufacturing services include process technology, special process technology, design ecosystem support, mask technology, 3DFabric™ advanced packaging, and silicon stacking technology services. The firm has completed the transfer and mass production of 5nm technology and is engaged in the research and development of 3nm process technology and 2nm process technology. The current market capitalization of the company is 1.708 trillion, with a TSM stock share price of $329.24.

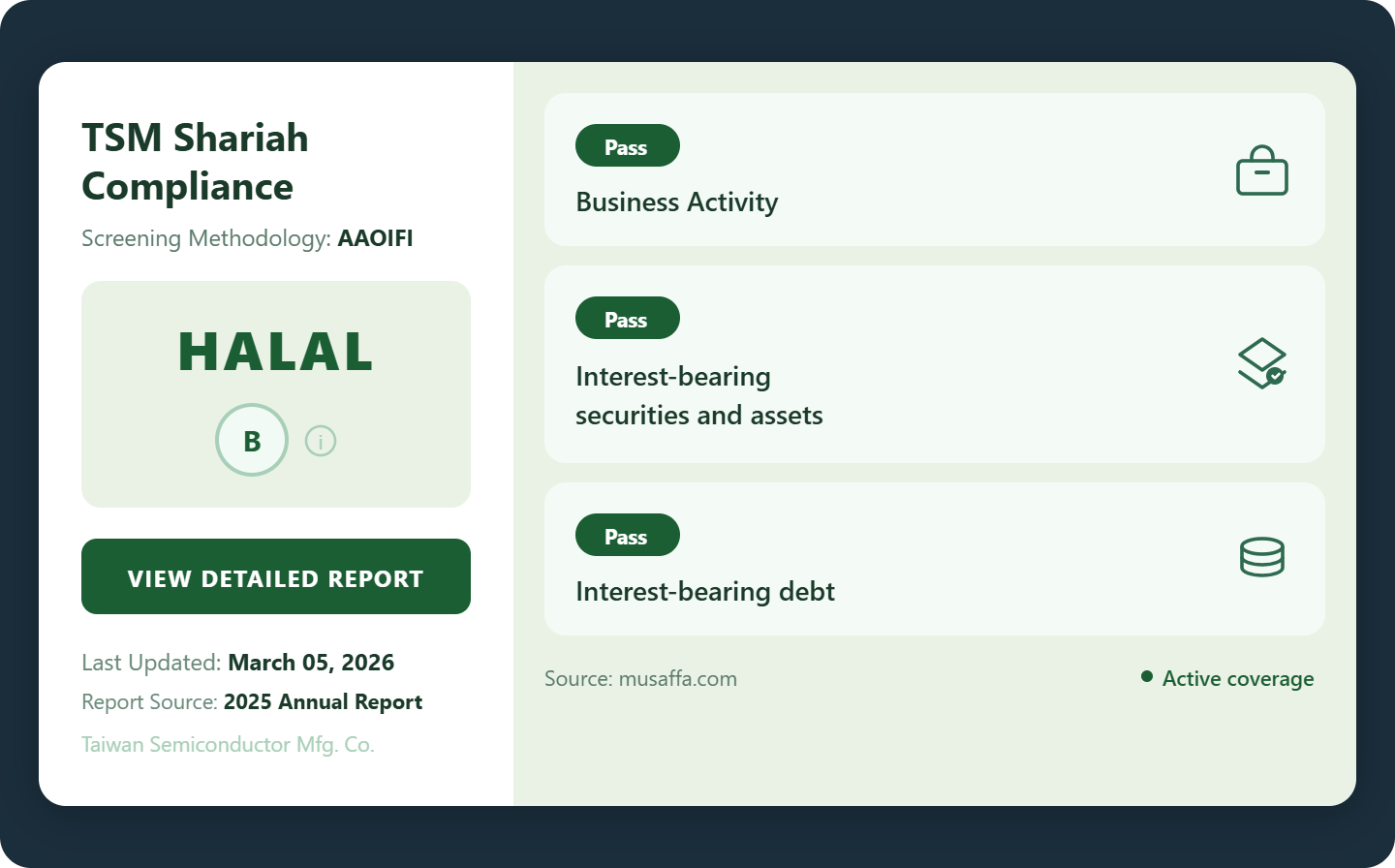

Shariah Status

For investors reviewing Shariah compliant stocks TSM, the Shariah status of the company is considered halal, with a ranking of B according to the AAOIFI screening methodology by Musaffa. According to the screening results, 97.31% of its business activity is recorded as Shariah-compliant, while 2.69% is not halal due to interest income. Interest-bearing securities and debt account for 13.11% and 3.74% of its assets and liabilities, respectively.

Business Analysis

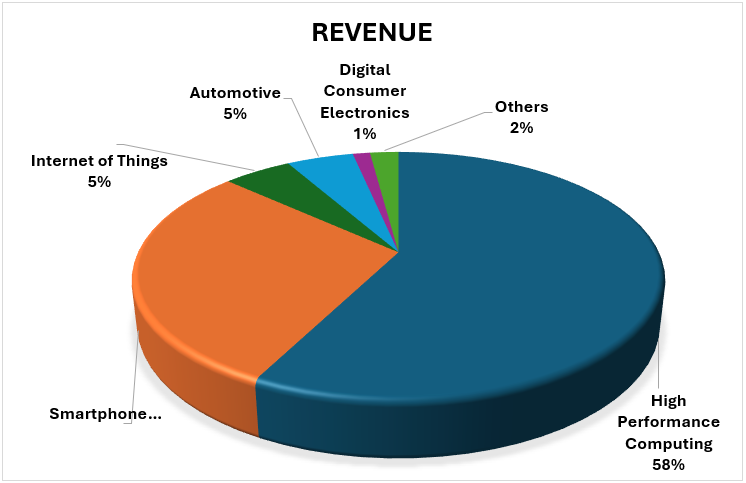

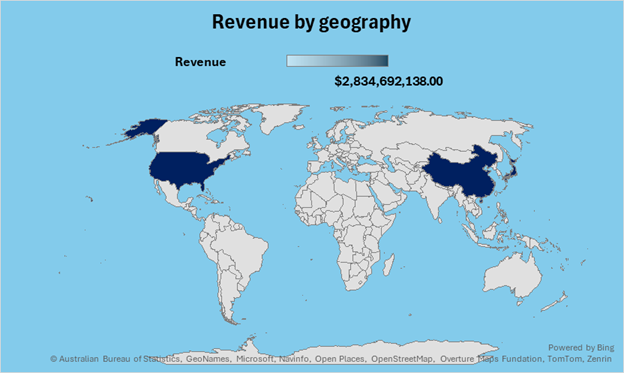

The significant increase in total TSM revenue, from $2.89 trillion to $3.81 trillion, was mainly driven by the Wafer segment, which increased by close to $758 billion due to high-performance computing and AI chips becoming the major driver in the semiconductor industry. This is evident in the company’s performance in the United States geography, which saw revenue rise by $1.99 trillion to $2.83 trillion, affirming that American tech giants are the main consumers of TSMC’s latest 3nm and 5nm chips. TSMC’s $3.81 trillion NTD revenue growth in 2025 was sparked by a 48.5% explosive growth of High-Performance Computing (HPC), which grew to $2.19 trillion NTD, officially becoming the largest business driver of the company. This AI-driven demand has also been seen in the United States, which has driven its revenues up to $2.83 trillion NTD as American tech giants increased their data centers using their premium 3nm and 5nm wafers. Although the Smartphone and Automotive segments have driven some secondary growth, the stagnant Digital Consumer Electronics and China markets indicate a global trend: the world is moving away from basic gadgets and investing its capital into the high-end infrastructure needed for the AI world.

Although the core wafer business is the powerhouse, the "Others" category, which is advanced packaging and testing, saw a substantial increase to $536 million, which is a move towards higher-complexity, integrated chip designs needed to support modern data centers. In terms of geography, while the U.S. is the anchor, Taiwan and Europe/EMEA are showing good growth, which is a move towards modernizing the world's digital infrastructure, even though there is a slight stagnation in China, which grew from $331 million to $327 million.

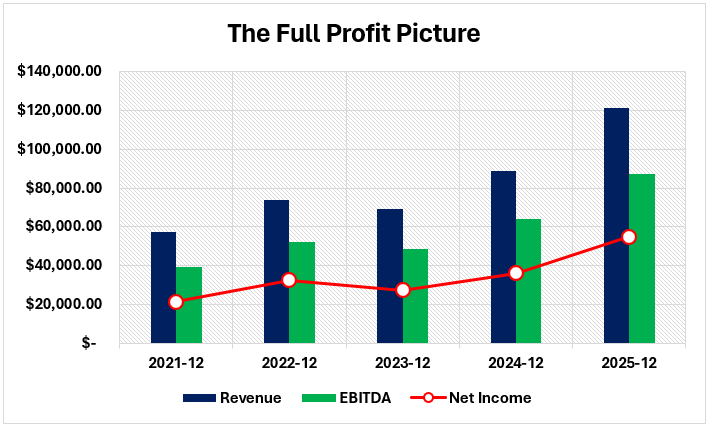

Financial Analysis

Reflecting on the TSMC FY 2025 results, between 2024 and 2025, TSMC underwent a transformation from being a supplier of smartphone chip technology to being the driving force behind the global AI boom. The company's total revenues increased from $2.89 trillion to $3.81 trillion NTD. This is a staggering 31.6% increase in just a single year.

The growth of TSMC's revenues is mainly attributed to the High-Performance Computing sector. The geographic market for TSMC's products is dominated by the US, given that the country is home to the world's most prominent players in the field of AI technology. This market segment increased from $1.99 trillion to $2.83 trillion NTD as companies such as NVIDIA and Microsoft sought to acquire TSMC's 3nm and 5nm wafers. The company did not only increase their revenues; they also increased their profitability. The company’s net income increased by 46.4% to $1.71 trillion NTD. This is further evidenced by their EBITDA, which increased to $2.34 trillion NTD. This is a significant amount of cash flow for the company to utilize for expansion into other markets such as Arizona and Japan.

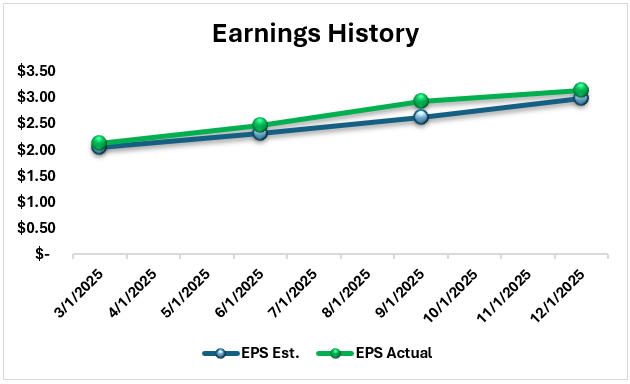

Earnings History

Reviewing recent TSMC earnings, the Taiwan Semiconductor Manufacturing Company has shown impressive performance in terms of earning surprises for the past four quarters of 2025. For every quarter of 2025, the company's actual EPS surpassed the estimates. The surprises were more pronounced during the middle of the year. Additionally, the company's earnings figures have shown consistent growth from $2.12 in the first quarter to $3.14 in the fourth quarter of 2025. This indicates that the company is gaining momentum in terms of business performance. It is evident that the company is enjoying robust business due to increased demand for advanced semiconductor products.

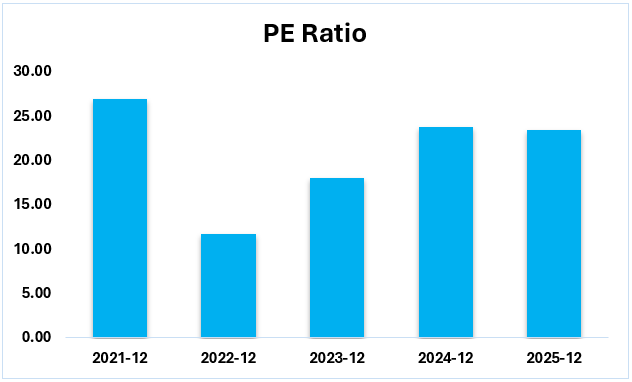

Valuation Analysis

Taiwan Semiconductor Manufacturing Company displays a trend in valuation over the years, which is cyclical in nature but shows improvement in valuation over time, according to the company’s P/E ratios from 2021 to 2025. The company’s P/E ratios declined from 26.93 in 2021 to 11.71 in 2022, indicating that the company’s stock became cheaper over this period. The company’s stock became cheaper due to a fall in demand for semiconductors in the industry, which affected TSM in 2022, when the company’s P/E declined to historic lows of ~11 to 12 (The Globe and Mail). The company’s stock began to recover in 2023, with the P/E rising to 18.05, indicating a positive trend in the company’s stock valuation over time. The company’s stock valuation continued to improve in 2024, with the P/E rising to 23.76, indicating improved demand, particularly in the production of high-performance computing and AI chipsets. In 2025, the company’s P/E declined to 23.40, indicating that while the company is growing in terms of earnings, the valuation did not increase, indicating that the company is now a mature company with growing earnings.

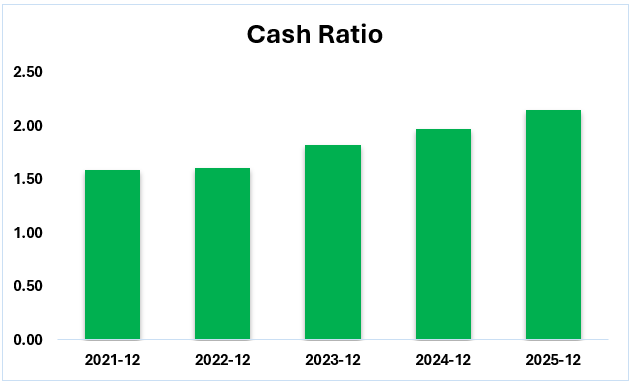

The cash ratio of Taiwan Semiconductor Manufacturing Company gradually increased from 1.59 in 2021 to 2.15 in 2025. This demonstrates that the company is generating more cash to cover short-term liabilities each year. The steady increase in the cash ratio indicates that the company is becoming more financially stable. The increase in the cash ratio from 1.82 in 2023 to 2.15 in 2025 is significant. This is because the company is generating more cash to cover short-term liabilities. The cash ratio is already above 1, indicating that the company is financially sound.

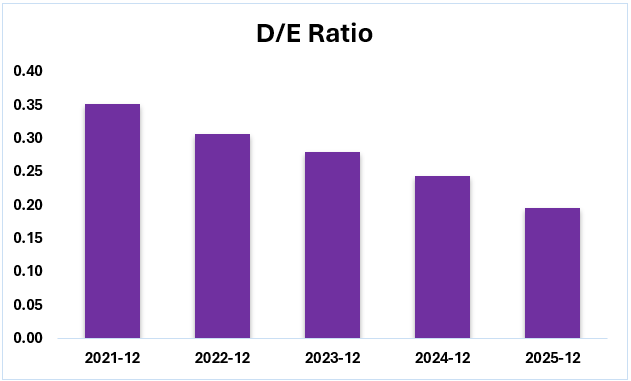

Taiwan Semiconductor Manufacturing Company displays a declining financial leverage trend over time, as reflected by the company's debt to equity ratio over the years 2021 to 2025. The company's financial leverage has been declining steadily over time. From 0.35 in 2021, the company's financial leverage declined to 0.20 by 2025. This indicates that TSM is using fewer debts as a source of financing compared to shareholders’ equity. This declining financial leverage indicates that TSM is either paying off debts or adding to shareholders’ equity. A declining financial leverage indicates that TSM has less financial risk since the company has fewer debts to pay. This indicates that TSM is not under any pressure to pay debts. A declining financial leverage over time indicates that TSM has been managing its finances well over time. By 2025, TSM's financial leverage stands at 0.20, which is relatively low for a company operating in a capital-intensive industry. This indicates that TSM has a robust financial position. This declining financial leverage indicates that TSM has been doing well over time.

Risks

There are several risks which should be considered by investors while making decisions:

1.Despite earning $2.83 trillion NTD from North American customers, TSMC still produces the majority of its high-end wafers in Taiwan, which makes its entire supply chain susceptible to regional instability or a potential blockade in the Taiwan Strait (Sciencedirect).

2.With High Performance Computing driving 58% of total revenues, any slowdown in the AI "gold rush" or a technology shift away from its major clients like NVIDIA could leave TSMC’s costly 3nm and 5nm fabs idle.

3.The company will have an uphill task ahead of it given the high cost of expanding to Arizona and Japan, while stagnant revenues from China, which were flat at $327 million, indicate that US export controls and increasing energy costs are creating a permanent drag on their record-breaking $1.71 trillion NTD net income (CNBC).

Conclusion

Taiwan Semiconductor Manufacturing Company has shown excellent financial results and growth in its operations, mainly due to increased demand for AI and high-performance computing chips. The firm’s revenues, profitability, and cash position are excellent and show its financial stability. In addition, the reduction in its financial leverage and strong cash ratios show its prudent management of resources. However, investors should always be cautious about possible risks in investing in TSMC, which include regional instability in Taiwan, high expansion costs in new markets, and its dependence on large clients like NVIDIA and US technology firms. TSMC is in a strong position as a leader in the global semiconductor industry.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed