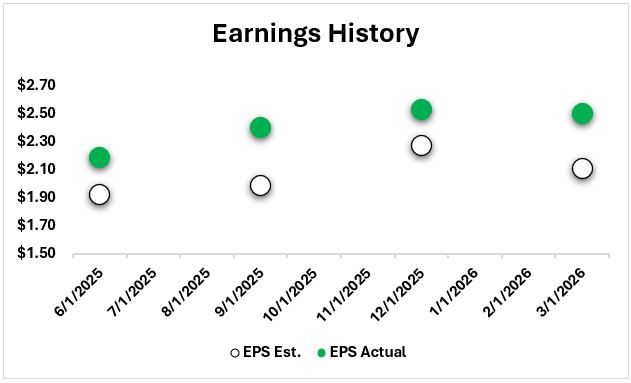

Intuitive Surgical posted an incredibly good first-quarter 2026 performance, which was marked by a big beat and raise performance in ISRG earnings, as the company exceeded expectations in all key financial indicators. Total revenue increased to $2.77 billion, which is 23 percent higher than in the year before, and adjusted earnings per share went to 2.50, which is much higher than the forecasted 2.12. This operational power was supported by a robust non-GAAP gross margin of 67.8, which indicated that the company is operating its supply chain and production expenses at a very high efficiency, with the global rollout of new hardware still going on.

This performance of Intuitive Surgical Q1 results was mainly caused by the quick uptake of the new da Vinci 5 platform, which contributed to more than half of the 431 systems sold in the quarter (Seeking Alpha). This next-generation technology shift increased average selling prices, and a 17% increase in procedure volumes around the world guaranteed a continuous flow of high-margin recurrent revenue on instruments and accessories. Moreover, the company experienced rocketing growth in its Ion endoluminal system, which means that Intuitive can diversify its revenues out of conventional robotic surgery into specialized diagnostic procedures. When considering future projections of the next round of results, Intuitive Surgical will be in a good position to continue moving and will probably surpass the present estimates once again. The management has already indicated an increased level of confidence by increasing its full-year growth projection of procedures by 13.5% to 15.5%, a move that would normally indicate a beat in the earnings, as the company has a record of under-promising. As the da Vinci 5 is only starting its global rollout, and recent regulatory clearances in major markets, including a new cardiac clearance, the company is in a high-growth stage, as demand in the marketplace remains strong and unsatisfied by supply in the market.

Revenue Growth Drivers

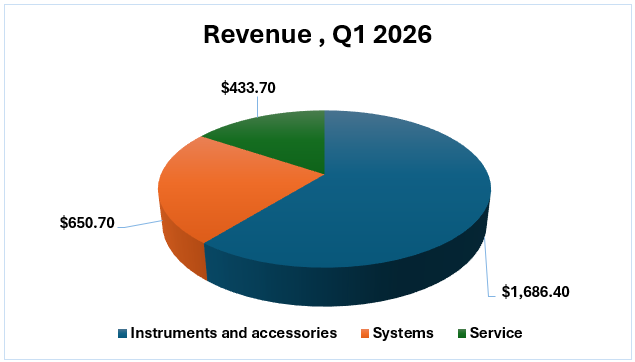

The total ISRG revenue growth of Q1 fiscal year 2026 was reported to be 2.77 billion in the company, which is a 23 percent increment from the 2.25 billion that was reported in the first quarter of 2025. This mainly contributed to the fact that the volume of surgical procedures increased drastically, and the next generation of the da Vinci 5 platform was successfully rolled out to the rest of the world. In the segment breakdown, Instruments and Accessories revenue was $1.69 billion, up 23.3% due to a 17% increase in global procedure volumes and a phenomenal 39% increase in Ion endoluminal procedures.

In parallel form, Systems revenue increased at an alarming rate to $650.7 million, with Intuitive placing 431 systems in the quarter, with the da Vinci 5 taking over half of the placements and the average selling price increasing to over $1.7 million. To add to these profits, Service revenue increased by 19% to $433.7 million as the global installed base was 11,395 systems with recurring revenue now representing an unbelievable 86 percent of total sales. The company can exhibit high operational leverage with Non-GAAP Gross Margins of 67.8 increasing to 38% in Non-GAAP Earnings Per Share (EPS) despite the pressure of about 100 basis points caused by international tariffs. Finally, the management has observed certain capital expenditure caution in specific regions of Asia, but the potential of robotic-assisted surgery demand in Western markets is a strong tailwind that the company has increased its full-year 2026 growth forecast of procedures to 13.5%15.5%.

Key Positive Takeaway

The overall conclusion of the Q1 2026 outcomes is the robustness of the growth procedure. Although selling robots (capital) is great, the true power is the number of robots that are in use.

1. 86% of total revenue has become recurring (Simply Wall St). This implies that the business does not have to depend on a one-off sale anymore; it will provide consistent cash flow each time a surgeon does surgery using the ISRG instruments and accessories.

2.The da Vinci 5 is not a slow adopter and has been taking in more than 54 percent of all the system placements during this quarter (Stock Titan). This demonstrates that hospital networks are keen on adopting the latest technology even though it is expensive.

3.The Ion platform (lung biopsies) is no longer considered a side project; it increased by 39% this quarter (Zacks). This shows that ISRG can effectively repeat the domination of robotic surgery in completely new areas of surgery.

4.Adjusted operating margins have greatly increased to 38.9% (Zacks). This demonstrates that the growth in revenue is enabling the company to be more profitable due to control in its internal costs (such as R&D and administration) as the sales scale up.

Main Risks

Although Intuitive Surgical (ISRG) is performing at a high level among robotic surgery stocks and Shariah-compliant stocks, investors need to keep an eye on several major risks that may affect its valuation and long-term supremacy. These are short-term challenges and longer-term competitive risks:

1. China is a key growth market, but provincial bids are becoming more inclined to give local Chinese robotic producers preferential treatment over foreign technology (Simply Wall St). Also, there are existing U.S.-China trade tariffs, which are already dragging the company's gross margins by 1.0 percent (Zacks).

2.The stock is currently trading at a forward Price-to-Earnings (P/E) ratio of about 47x57x, much higher than the medical device industry average of 26x, after the Q1 beat. This premium exposes the stock to the possibility of severe pullbacks in case future performance reveals any indication of a decline (Yahoo Finance).

3.With ISRG shifting to a data-driven, more digital surgery model, with its My Intuitive+ ecosystem, the organization is at a higher risk of cyberattacks. The recent reported cybersecurity attack on customer and employee data underlines the continued susceptibility of their cloud-based systems (Investing.com).

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed

Foziljon Kamolitdinov

Foziljon Kamolitdinov