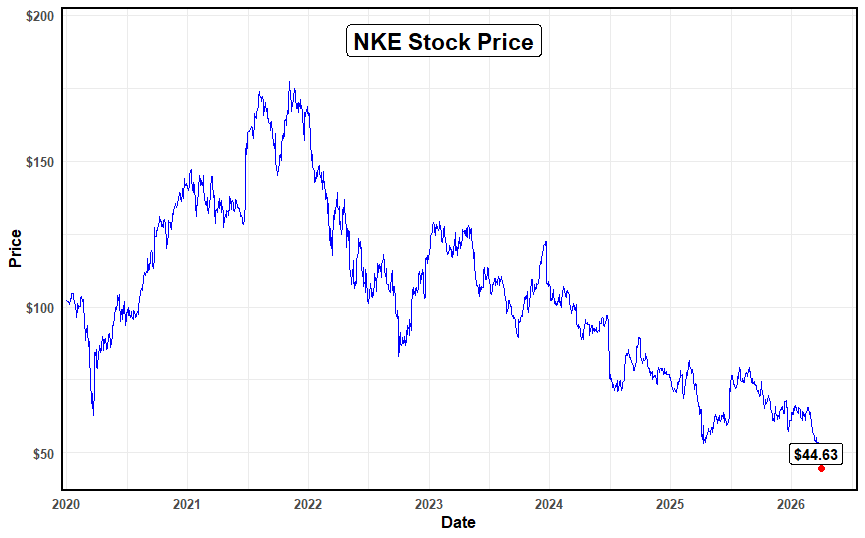

Nike, Inc (NKE, A-, Halal) is the world's largest seller of athletic footwear, apparel, and equipment, designed to bring inspiration and innovation to athletes worldwide. They focus on creating high-performance products (like Air Jordan), promoting sustainability, and fostering community through sports initiatives. The current market capitalization of the company is $91.5 billion, with current share price of $44.63.

Shariah Status

The Shariah status of the company is considered halal among Shariah compliant stocks NKE, with a ranking of A- according to the AAOIFI screening methodology by Musaffa. According to the screening results, 99.40% of its business activity is recorded as Shariah-compliant, while 0.60% is not halal due to interest income. Interest-bearing securities and debt account for 6.17% and 5.93% of their assets and liabilities, respectively.

Business Analysis

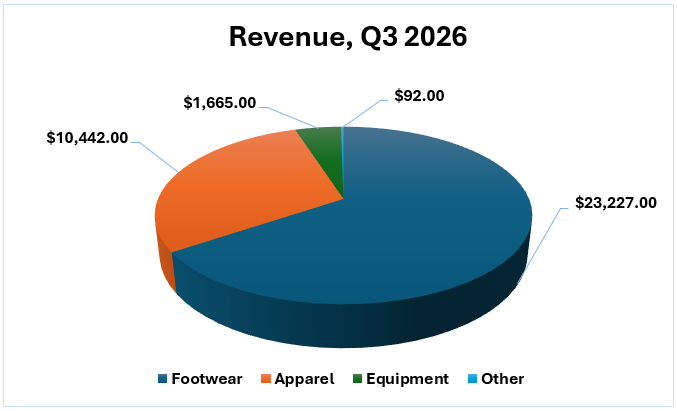

During the third quarter of fiscal 2026, Nike posted a segmented income report that shows that the brand is still in the process of shifting to performance-based innovation. Nike footwear revenue continued to be the core business with revenue of $23,227 million, which was backed by high single digit growth in the running and global football segments even though the supply of the classic lifestyle franchise was strategically cut to ensure it retained its market scarcity. The apparel added 10,442 million dollars to the total, which was a mixed performance with the strong demand on technical training equipment in North America slightly undercut by a 7 per cent decrease in the Greater China market owing to the changing habits of consumer spending.

The Equipment division brought in revenue of around 1,665 million, which was supported by a 10 percent growth in the North American sales where the company effectively re-energized consumer interest in team sport and field equipment. On the other hand, "Other" sources of revenue, which comprised licensing and non-core operations, constituted 92 million out of the total. The effect of these figures is due to the Nike turnaround strategy, Win Now, that focused on re-establishing its wholesale relationships, resulting in a 5% growth in this channel, and deliberately suppressed its Direct-to-Consumer online sales by 4% to clear the older inventory. Finally, these outcomes were obtained in the context of strong macroeconomic headwinds, such as a 230 million restructuring cost and increased tariffs in North America, which forced gross margins to 40.2 per cent in this critical reset phase.

Financial Analysis

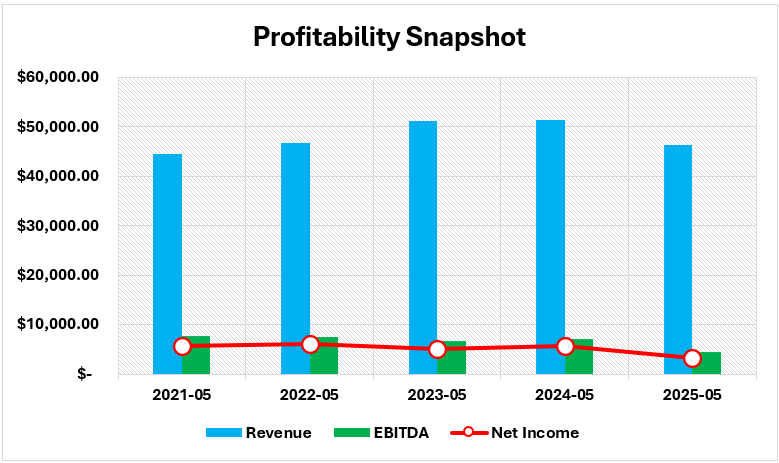

In the fiscal year of May 31, 2025, Nike disclosed a serious decline in its main financial indicators, a factor which the management described as the climax of a Nike calculated strategic reset. Revenue dropped to 46,309 million, a decline of 10 percent over the year before as the company deliberately limited the number of its most coveted classic footwear silhouettes, including the Air Force 1 and Dunk, to create a situation of brand scarcity and allow new innovation. This intended narrowing was enhanced by a decrease in the Nike Direct revenues by a factor of 13 percent and a drop in online sales by 20 percent, due to the online traffic reduction and a reversal of the deep promotions that had sustained high volume sales but weakened brand equity.

Its effect on the bottom line was even more significant, as the net income decreased 44 percent to $3,219 million and EBITDA decreased to $4,510 million. These falls were mainly due to a shrink in gross margin of 190 basis points which were strained by increased markdowns to clear seasonal stock and the poor developments in the channel mix. The company was experiencing strong headwinds in Greater China where its revenue declined by 13% owing to weak consumer demand and emerging competition by local brands. Nike, despite the fact, remained long-term brand health-focused, with the percentage growth of its demand creation rising by 9 percent, focusing on the Paris Olympics marketing and the reopening of its sport-center brand image, led by the new CEO, Elliott Hill.

Earnings Analysis

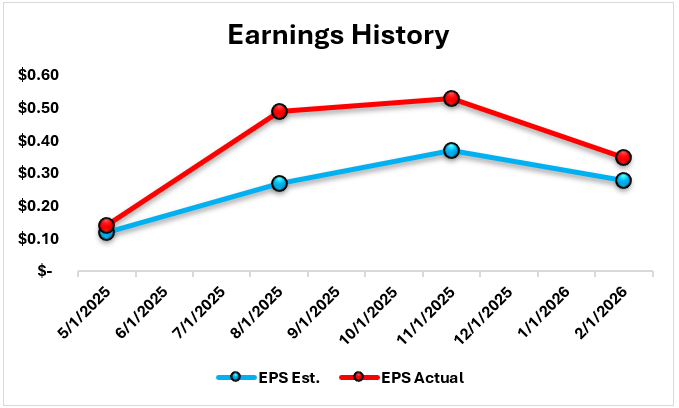

According to the graph of Nike Earnings Per Share (EPS) that is presented, Nike showed a steady trend of exceeding market expectations in all four quarters that ended at the beginning of 2026. The greatest outperformance was seen in the quarter ending August 31, 2025, as the actual EPS of $0.49 was significantly higher than the estimate of $0.27 by almost 81 per cent, which was a strong indication of much quicker recovery in profitability than the initial projections of the analysts had indicated. The trend persisted in the November 2025 and February 2026 quarters, where actual earnings have continued to exceed the forecasts by 0.16 and 0.07 respectively indicating that the company cost-cutting strategy and Win Now turnaround plan were more effective at cushioning the bottom line than expected.

The highest earnings per share in November (0.53) and the seasonal low in February (0.35) are also typical of retail cycles, but the fact that Nike still exceeded the 0.28 forecast in Q3 2026 is indicative of more efficient operations despite the operation-related headwinds mentioned above. Overall, this information suggests that, although the revenue was experiencing a reset, Nike still managed to generate profit per share, which is probably due to the fact that the company achieved above average inventory turnover and administrative overhead decreased.

Valuation analysis

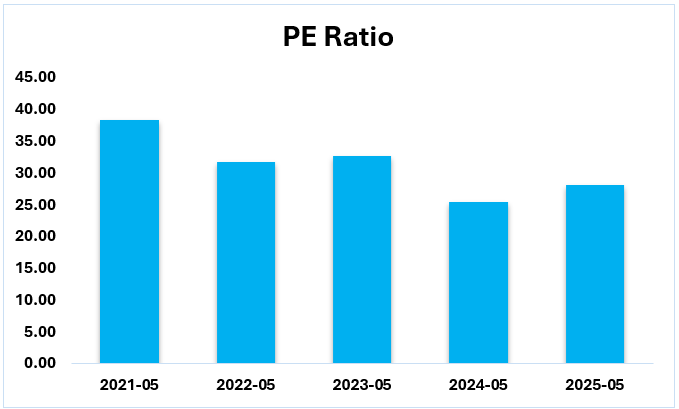

The PE ratio of Nike has also shown a significant negative trend between May 2021 and May 2025, falling between 38.33 and 28.05. Such downward movement is a 27 percent valuation squeeze, which implies that investors are currently willing to pay a dollar less per dollar of Nike earnings than they have been paying throughout the post-pandemic boom. Although the ratio continued to be relatively stable, with the values fluctuating around the 32x point, in May 2024, it went down to the lowest level of the last five years, at 25.48. This drastic decline was probably an indication of the market anxieties regarding the declining growth or higher competition. Nevertheless, the later increase to 28.05 in May 2025 suggests that the investor confidence will recover moderately, and the share is still trading below the 2021 valuation levels.

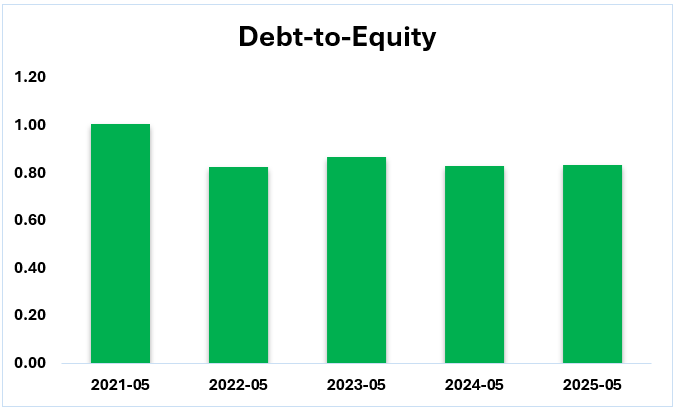

The debt-to-equity ratio of Nike has been growing steadily and negatively since May 2021 and has fallen, reducing its value to a more stable 0.83 since then. The fact that this was reduced by 17%, means that the company is less dependent on borrowed funds to finance its operations, which essentially has been strengthening its balance sheet. Following a significant decline in 2022, the ratio was impressively steady (between 0.83 and 0.87) in the next three years. Such stability gives an indication of a well-managed capital management plan as Nike has managed to balance its debts with its expanding shareholder equity even with the changing market conditions.

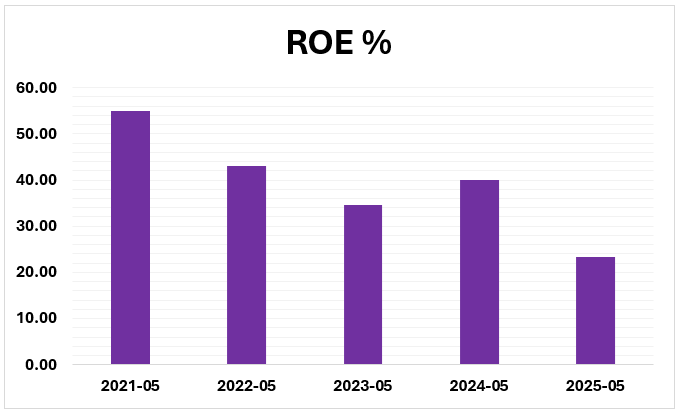

The ROE of Nike has been decreasing sharply in the past four years, with the highest value of 55.01% in May 2021 and the lowest value of 23.29% in May 2025. This 58% net reduction indicates that the efficiency of the company in creating profits out of the capital of shareholders has significantly diminished throughout this period. The steepest decline was recorded between 2024 and 2025, during which the ROE reduced by almost half, to 23.29. Although a short-term recovery was observed in 2024, the further dive to a five-year low is a sign that Nike is under mounting pressure on its net income margins or is undergoing a major change in its equity structure.

Risks

1.Nike is losing a great deal of market share to both traditional competitors such as Adidas (Yahoo Finance) and more specialized performance shoe brands such as Hoka and On Running (Forbes). The rivalry is especially fierce in the running segment, where Nike has been ineffective in its innovations in the past, letting more agile brands win over the luxury market.

2.Nike is extremely susceptible to trade shocks because approximately 95 percent of its footwear and 60 percent of its apparel are produced in Southeast Asia. New tariffs on imports into countries such as Vietnam and China have been estimated to cost the company as much as $1.5 billion annually (Global Banking & Finance), which will drastically narrow the profit margin.

3.The third largest market in the world, Greater China has become one of the main setbacks to Nike thanks to the so-called Guochao trend, as the local audience is becoming more inclined to use domestic brands such as Anta and Li-Ning (IMD). The result of this cultural change alongside the absence of localized product innovation has seen six quarters of revenue decline in the region in a row by the early of 2026 (The Business Times).

Conclusion

Nike is in the process of a strategic shift, which is manifested in the form of falling revenues, profitability, and valuation levels. Although the financial situation is under strain in the short term, the business has strength in its strong brand positioning, cost management, and stable earnings showing. Nevertheless, the growing competition, weakness in the region, and external risks are still important issues. In general, the NKE stock forecast has a complex picture, as it is uncertain in the short term but can recover in the long term in case the strategic initiatives are carried out successfully.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Foziljon Kamolitdinov

Foziljon Kamolitdinov

Nusrat Ahmed

Nusrat Ahmed