Company overview

Ross Stores is a discount store. Through Ross Dress for Less and DD's DISCOUNTS, it offers branded clothing and household items at reduced costs. Because customers can trade down from more expensive stores without completely halting purchasing, the model often works best when shoppers are value-focused.

What’s driving the story right now

Sales and same-store sales were the two most important retail scorecard metrics for the most recent quarter. Comparable store sales increased by 9% and Q4 sales increased by 12% to over $6.6 billion. This combination helps explain why the quarter's profit performance was better than anticipated and typically indicates true demand strength (rather than just price inflation or new stores).

Additionally, management focused on "shareholder returns." The quarterly Ross Stores dividend was increased by 10% to $0.445 per share, and a new two-year $2.55 billion repurchase authorization was authorized. These measures demonstrate confidence in cash generation, which is important to many investors.

Financial analysis

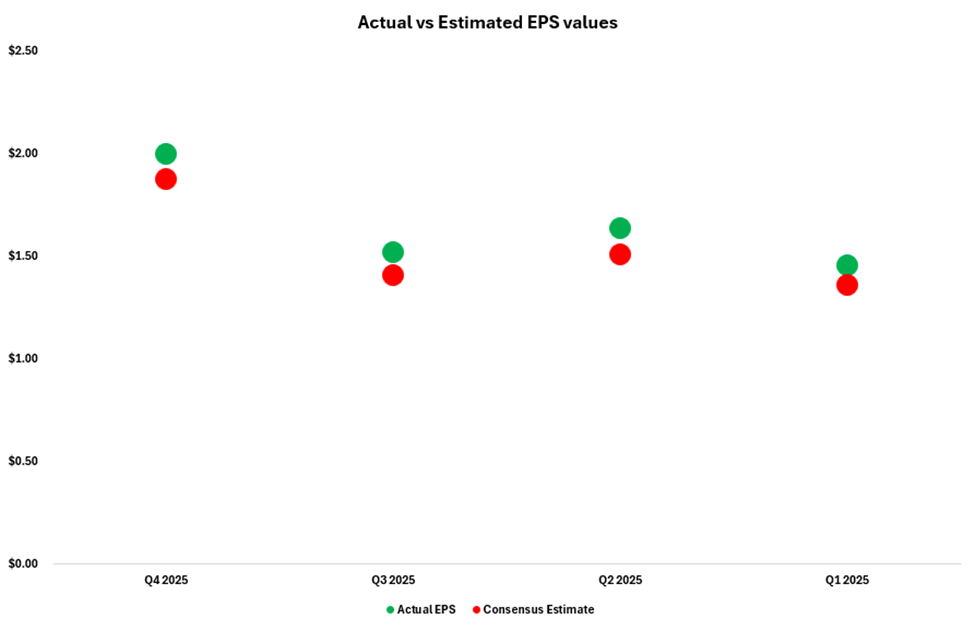

Growth and better-than-expected profitability were both achieved during the quarter. Exploring the Ross Stores Q4 results, Q4 EPS was $2.00, up from $1.79 a year earlier, while net income was $646 million. Significantly, the company's operating margin in Q4 exceeded its forecast by 12.3%, mostly due to higher-than-expected sales.

For the entire year, comparable sales increased by 5%, revenues hit a record $22.8 billion, and EPS was $6.61. When considering "cleaner" growth comparisons, management quantified the EPS impact at roughly $0.16 and cited tariff-related charges as a drag in the year. This helps explain why, in a retail year with cost pressure, EPS growth may appear slower than sales growth.

Additionally, cash flow increased annually. For the year, operating activities generated around $3.03 billion in net cash. This is significant because it facilitates buybacks, dividends, and retail expansion without significantly depending on additional financing.

Quarter check

Q4 revenue exceeded expectations by around 3%, coming in at $6.64 billion as opposed to $6.44 billion. Q4 non-GAAP EPS surpassed expectations by around 6%, coming in at $2.00 as opposed to $1.88. Particularly for an established retailer, these are strong beats.

Depending on what the market focuses on next, the stock may still move in multiple directions even after a beat. According to Ross, the "next" challenge is whether the business can maintain competitive advantages as comparisons become more difficult and whether expenses (such as tariffs and pressure on wages and logistics) can be controlled. Guidance is therefore frequently just as important as the reporting quarter.

Read More:

- The Rise of DoorDash: Q4 Results, Expansion, And Challenges

- Moody’s 2026 Guidance Highlights AI Tailwinds—and the Real-Time Credit Cycle

- EQIX Q4 Earnings: Revenue, EBITDA Beat? AI Hyperscale & 2026 Outlook

Outlook

Comparable sales are expected to rise by 7% to 8% for Q1 FY26 (13 weeks ending May 2, 2026), while EPS is expected to be between $1.60 and $1.67.

Shaping the ROST stock forecast, the company forecasts same-store sales growth of 3% to 4% and EPS of $7.02 to $7.36 for FY26 (52 weeks ending January 30, 2027).

To put it simply, management is informing investors that the robust Q4 momentum is anticipated to continue into spring before normalizing to a good but more moderate full-year pace.

Price and valuation context

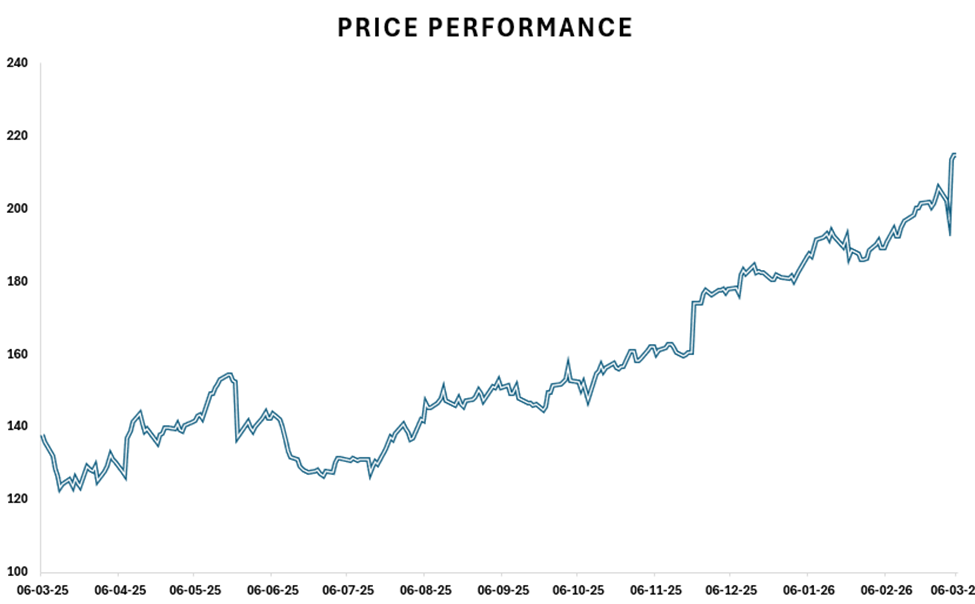

As of March 3, 2026, ROST closed at $197.64. It is trading below its 52-week high of $206.40 but well above the $122.36 low, down 2.30% on the day but up 11.03% over three months and up 9.71% year-to-date.

The valuation at current prices indicates that the market is still viewing Ross as a "quality" retailer: trailing P/E is roughly 30.9x, EV/Sales is roughly 3.1x, and EV/EBITDA is roughly 21.6x. The market pays for consistent execution—positive comps, managed inventory, and robust margins—when a retailer trades at a premium multiple.

The balance sheet displays $1.52 billion in total debt (current plus long-term) and $4.59 billion in cash and cash equivalents. Additionally, Ross has significant lease obligations (about $2.97 billion non-current and $0.73 billion current). This is significant because, in the retail industry, lease obligations are "debt-like," which helps explain why, even in situations where cash appears to be robust, enterprise value can remain higher than market cap.

Risks

The primary danger is that the current momentum will cool more quickly than anticipated. Comps are currently strong, but if customers retreat or competition demands more deals, retail demand could shift rapidly. Another risk is cost pressure. Tariffs, freight, wages, and shrinkage can all put pressure on margins; the company has already shown how tariffs affected outcomes. In off-price retail, execution risk is especially important because the business relies on continually sourcing appealing branded inventory at appropriate discounts; any failure in this area could negatively impact traffic and profitability. Lastly, if early-quarter indicators worsen or guidance softens, a premium valuation may prompt a strong response in the stock.

Shariah Compliance

For investors reviewing Shariah-compliant stocks ROST, as of December 2025, Ross Stores (ROST) is classified as Shariah-compliant (Halal) with an A+ Musaffa rating based on the Shariah Screening results at Musaffa. ROST’s 2025 3rd Quarter Report was used to conduct the screening analysis in line with the AAOIFI methodology. ROST passed all three required screening thresholds, with 99.24% of its business activity meeting the permissible (Halal) threshold (0.00% doubtful and 0.76% not Halal). Both interest-bearing securities and assets (0.01%) and interest-bearing debt (0.00%) remain below 30% of the 36-month average market capitalization.

Conclusion

Ross's Q4 performance was outstanding, with high comps, sales, and EPS that exceeded expectations. Follow-through is the focus of the next phase, where management is increasing buybacks and raising the dividend, leading to a very robust spring and a strong full-year projection. Comps (especially as comparisons get more difficult), operating margin stability, and whether cost pressures remain under control while shareholder returns continue are the easy benchmarks to monitor.

Sources

- Ross Stores Inc. Stock Analysis

- Ross Stores Inc Stock News from GuruFocus

- Ross Stores Inc

- Ross Stores Reports Fourth Quarter Earnings Well Above Guidance

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed