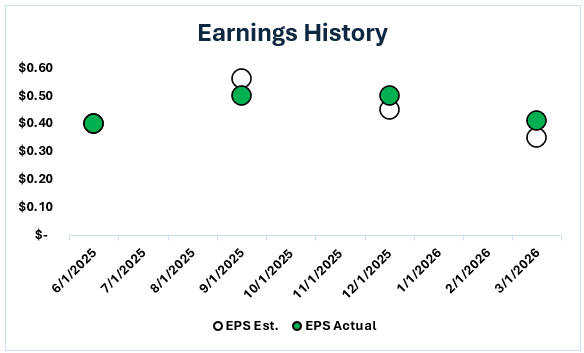

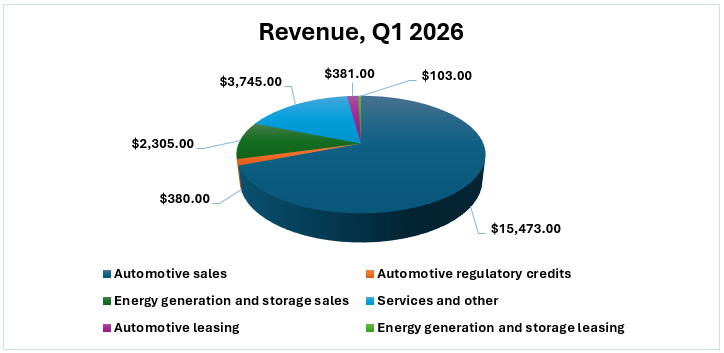

Tesla (TSLA, B, Halal) released its first-quarter 2026 earnings report, which saw a top-line revenue beat and a major pivot to AI and robotics. It achieved revenues of $22.39 billion, up 16% year-on-year, exceeding the analyst estimate of $22.28 billion (Stocktitan). On profits, Tesla stock has achieved a non-GAAP EPS of $0.41 versus the analyst consensus of $0.37 in the recent TSLA earnings. This earnings performance was supported by the company's improved gross margins for its automobile business (excluding credits) to 19.2% and a highest-ever gross margin for the Energy Storage segment of 39.5% (Tesla). However, GAAP net income only increased to $491 million, as a major player among EV stocks and Shariah-compliant stocks, TSLA, Tesla juggled successful operational performance against a staggering $2.5 billion in capital expenditure to build its AI and manufacturing capacity.

Revenue Growth Drivers

The main driver of Tesla's Q1 results was a 20% year-on-year rise in vehicle sales, aided by a rebound in demand in the EMEA region, particularly in France and Germany, and steady average selling prices (ASPs). Although global deliveries of 358,023 vehicles fell slightly short of some analyst forecasts, revenue was offset by a shift in product mix toward more profitable configurations and continued growth in services revenue.

The second, but no less important, driver was the growth in the Autonomy and AI services, with active FSD (Supervised) subscribers up 16% quarter-over-quarter to 1.28 million. Also, although there was a 15% drop in total deployments in the Energy segment to 8.8 GWh, revenue was "high quality" due to much lower material costs and one-time tariff benefits, enabling the segment to disproportionately contribute to operating profit despite lower volume.

Main Points

The quarter was dominated by a dramatic shift in positioning itself as a high-margin robotics and software ecosystem, aside from the traditional car metrics.

1.Tesla lifted its Capital Expenditure guidance for the year to $25 billion (from $20 billion) to support the construction of the "Terafab" data centre and Cybercab pilot build (MSN).

2.The Energy segment achieved a new high, 39.5% gross margin, despite lower sales, demonstrating that the Tesla stationary storage business (Megapack) is becoming a key source of profitability (Investing).

3.Tesla closed the quarter with $44.74 billion in cash and short-term investments, giving it a huge cash pile to fund its $2.0 billion SpaceX investment and the purchase of a niche AI hardware company.

4.Tesla generated $1.4 billion in free cash flow, a number helped by the strategic delay of suppliers' accounts from 61 to 71 days to buy time as Capex is ramping.

Main Risks & Headwinds

Management highlighted a few structural issues that may impact the TSLA stock forecast performance in the near term:

1.Tesla disclosed that it expects negative free cash flow for the rest of 2016 due to the ambitious $25 billion investment plan and that it is prioritizing the long-term AI "S-curve" over short-term cash flows (Tesla).

2.With 408,386 units produced, there was a 50,000-unit gap between production and deliveries. This resulted in the largest single-quarter inventory build-up on record for Tesla, which could lead to price reductions (Tesla).

3.Tesla pointed out that 100 basis points of margin pressure remains from international tariffs and EV tax credit phase-outs in major markets such as the U.S.

4.The P/E ratio of ~360 Tesla carries is premised on the near-perfect execution of its Robotaxi and Optimus programs, which will be several years from generating substantial revenue (Seeking Alpha).

Sources

1. Musaffa

2. Stocktitan

3. Tesla

4. MSN

5. Investing

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Nusrat Ahmed

Nusrat Ahmed