UniFirst Corporation (UNF, A+, Halal) is the leader in the United States of America that offers managed uniform and workwear programs, facility service products, and first-aid supplies. They lease, rent and sell clothes such as shirts, pants, and flame-resistant clothes and offer cleaning, maintenance and pick-up and delivery services to more than 300,000 businesses. The current market capitalization of the company is $3.73 billion, with current market share price of $256.19.

Shariah Status

For those seeking Shariah compliant stocks UNF, the Shariah status of the company is considered halal, with a ranking of A+ according to the AAOIFI screening methodology by Musaffa. According to the screening results, 99.69% of its business activity is recorded as Shariah-compliant, while 0.31% is not halal due to interest income. Interest-bearing securities and debt account for 3.92% and 0% of their assets and liabilities, respectively.

Business Analysis

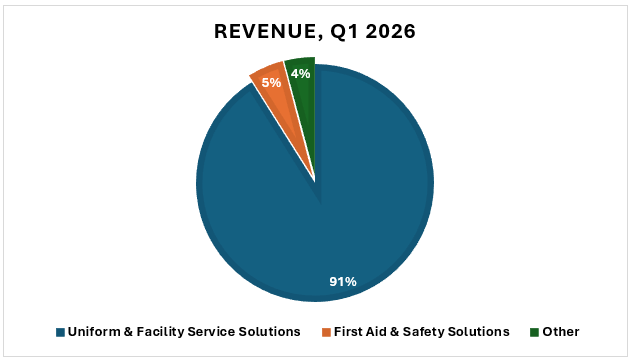

The first quarter of fiscal 2026 consolidated revenue of UniFirst Corporation showed effective growth in the key business segments with a consolidated revenue amounting to $621.3 million. The UniFirst Uniform and Facility Service Solutions segment, which comprises most of the company income of $565.9 million, grew by 2.4% due to steady organic growth and the effective acquisition of new customers. This was supported by a remarkable 15.3% growth in the First Aid and Safety Solutions segment, which increased to $30.2 million owing to strategic investments and minor acquisitions which increased delivery services of the company that specialized in being offered by vans.

On the other side, the other segment, consisting of nuclear decontamination and cleanroom services, suffered a minor 2.9% drop to $25.2 million due to a reduced number of scheduled reactor outages and the finishing of a significant refurbishment project. Although these revenue numbers indicate an encouraging trend in the marketplace, total profitability during the period was curtailed by higher operating costs associated with a multi-year digital transformation project and higher-than-anticipated healthcare and legal costs.

Financial analysis

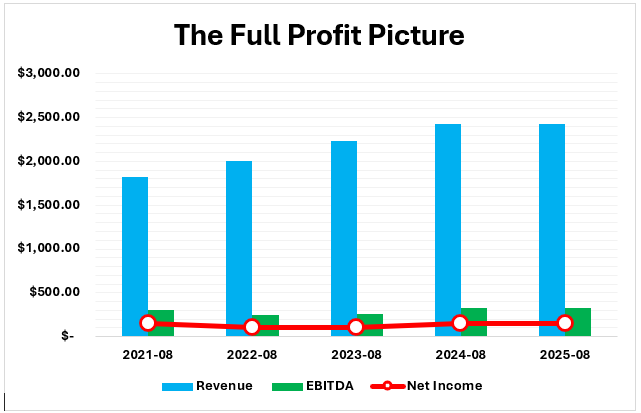

The five-year financial performance of UniFirst Corporation up to fiscal 2025 shows that the company experienced a growth in revenues with changing profitability impacted by strategic investments and changes in market conditions. Consolidated revenue increased by 10 percent, between fiscal 2021 and 2025, to 2.43 billion, due to a consistent upward trend, with the core Uniform and Facility Service Solutions division contributing the most, and the First Aid and Safety business increasing by more than 10 percent. Although in 2025, revenue was at a new peak, the rate of growth has slowed to 0.2 year over year growth, though with the additional week of operations to fiscal 2024, the true growth rate of 2025 was healthier at 2.1%. The measures of profitability, namely Net Income and EBITDA, were more volatile in this same period, with the lowest rates observed in 2022 and 2023 before returning to normal. EBITDA declined to $243.1 million and 254.8 million in fiscal 2022 and 2023 respectively, respectively, as the company incurred high expenses on Key Initiatives, which included a multi-year digitalization of its ERP and CRM systems.

These same pressures were also observed in net income, along with increased merchandise, payroll and energy expenses in the post-pandemic inflationary period. The financial situation of the company has stabilized by fiscal 2024 and 2025, with net income going back to the range of $145 million to 148 million and EBITDA going over 324 million. This recovery was assisted by the successful acquisition integration such as Clean Uniform in 2023 and better operating leverage as the most intense spending of their technology programs started to lessen (UniFirst).

Earnings analysis

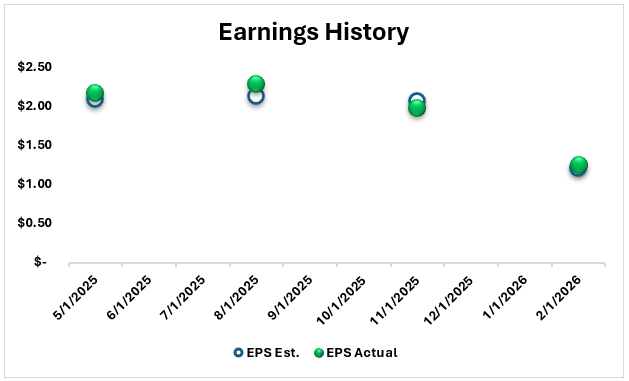

The performance of UniFirst Corporation in terms of UNF earnings Per Share (EPS) in the past four quarters shows a steady performance above the market expectations although the overall per-share profitability is on a significant decline. The company recorded good performances in the period ending May 31 and August 31, 2025, with actual EPS of 2.17 and 2.28 respectively, which is far above the analyst estimates. Nonetheless, profitability started to narrow in the quarter ending November 30, 2025, when the actual EPS of 1.98 was below the forecast of 2.06, which was mainly because of the high legal and healthcare expenses. The latest quarterly release, as of February 28, 2026, is of UniFirst, with an EPS of 1.25, which, though higher than the estimate of 1.21, is an extreme sequential drop compared to the prior year.

This overall decline in EPS shows the existing strain on profit margins as the company balances its revenue growth with the high operational costs it must bear in its digital transformation and the expenses of its pending merger with Cintas (Cintas).

Valuation analysis

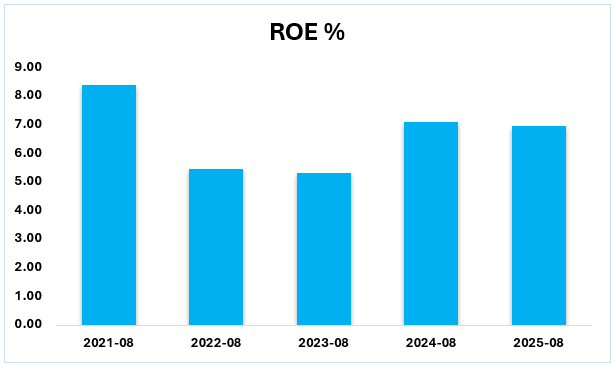

The Return on Equity (ROE) of UniFirst stock varied during the years 2021-2025 and this indicates that the company was undergoing an intensive internal investment that strained the returns to the shareholders in the short term. High operating costs associated with the multi-year digital transformation and the overhaul of the ERP system of the company caused the decrease in the percentage of 8.36 in 2021 to a low of 5.29 in 2023. ROE has rebounded by 2024 and 2025 to the 7% range as this technology investment has started to stabilize and newer acquisitions have begun to add to the bottom line. Although this is recovering, the metric is still lower than the industry peers because UniFirst has a debt free balance sheet with high equity levels, which of course dilutes the ROE computation.

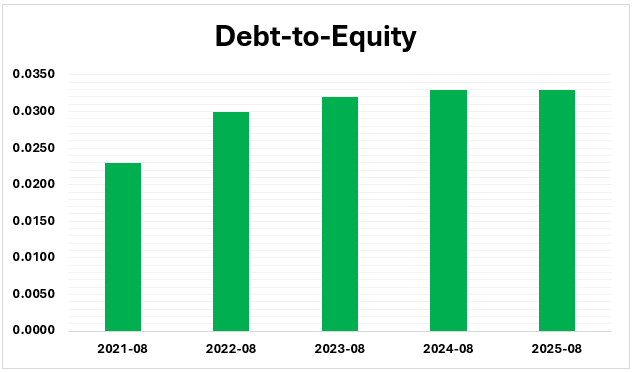

UniFirst Corporation has a highly conservative capital structure due to its Debt-to-Equity ratio that was consistently lower than 0.04 in 2021-2025. This insignificant amount of debt shows that the company funds its operations and multi-year digital transformation practically only out of internal cash flow and shareholder equity and not with the help of external borrowing. Although there was a slight improvement in the ratio between 0.023 in 2021 to 0.033 in 2025, it is still very low compared to industry averages, as the company has a very low-risk financial profile before its merger with Cintas in 2026.

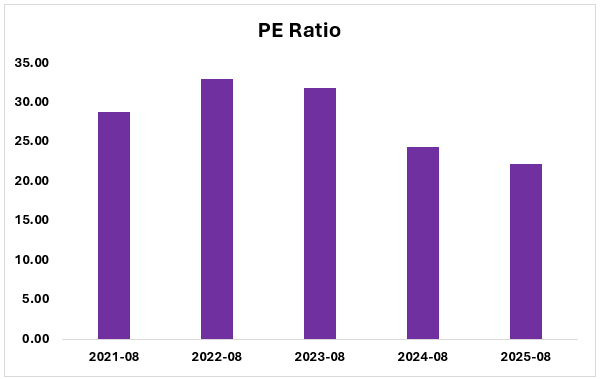

Prices to earnings (P/E) ratio of UniFirst Corporation has also undergone a discernible contraction during the period 2021-25 and this represents a drastic change in the market valuation. The ratio reached a peak of 33.01 in 2022 and has consistently decreased to 22.28 by 2025, which means that the investors have started to spend less on every dollar of the company earnings. This pattern is probably a shift away to a growth-at-any-cost valuation at the height of the company spending on digital transformation to a more value-based one as the merger of Cintas and the company in 2026 neared.

Risks

UniFirst Corporation has three major threats that might affect its financial results and strategic objectives in 2026.

1.The company is vulnerable to changes in the employment environment with a weaker labor market or fewer of its industrial clients driving uniform wearers and overall organic growth to the ground.

2.There has been constant pressure on profit margins because it has been spending a lot of money over a multi-year period to transform its operations digitally (ERP and CRM overhaul), and there is also a possibility of integration issues, given its impending $5.5 billion merger with Cintas (Cintas).

3. The profitability is exposed to an increased cost that is mostly beyond its control such as fluctuating energy prices, escalating healthcare and legal claims and the possible effect of new tariffs on its international supply chain of merchandise.

Conclusion

UniFirst Corporation has shown a consistent increase in revenue and a good financial standing with a low-risk capital base. Nevertheless, profitability is at stake because of the excessive operational and transformation expenses. Although recent recovery is positive in terms of efficiency, the current risks and strategic issues provide a moderately pessimistic short-term perspective with a moderate potential in the long term.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Foziljon Kamolitdinov

Foziljon Kamolitdinov

Nusrat Ahmed

Nusrat Ahmed