Acuity, Inc. (AYI, A-, Halal) is a major industrial technology stock that deals with lighting and intelligent spaces, producing products that augment, connect, and streamline buildings. They prioritize IoT solutions, smart lighting, and energy management to ensure the environments are safer and more sustainable. Market capitalization of the company is $9.48 billion, with current Acuity Brands stock market price of $282.32.

Shariah Status

The Shariah status of the company is considered halal among Shariah compliant stocks AYI, with a ranking of A- according to the AAOIFI screening methodology by Musaffa. According to the screening results, 99.82% of its business activity is recorded as Shariah-compliant, while 0.18% is not halal due to interest income. Interest-bearing securities and debt account for 4.84% and 10.27% of their assets and liabilities, respectively.

Business Analysis

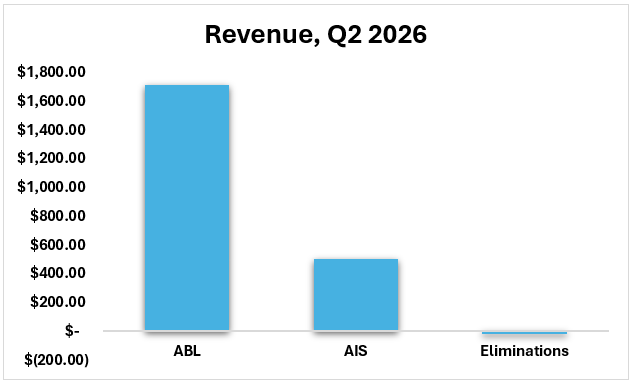

Acuity Brands, Inc. realized a consolidated revenue of around 2,199.40 million in the Acuity Brands Q2 results of 2026, prior to internal adjustment, which is a result of strategic balance between its traditional manufacturing core and its high growth technology divisions. The Acuity Brands Lighting (ABL) segment was the main contributor of this total, as it delivered $1,712.50 million by keeping a consistent base of infrastructure and roadway lighting projects even with a wider "softness" in the commercial construction way of life. The Acuity Intelligent Spaces (AIS) segment contributed greatly to this huge revenue floor as it brought in $505.50 million in revenue after a spike in the demand of smart building controls and successful implementation of the Q-SYS audio-visual platform. To maintain the accuracy of these figures, the company recorded the inter-segment sales, which included intra-company component transfer, using $18.60) million of Eliminations and as a result, the company avoided the duplication of revenue in the final financial statement. Finally, this particular level of revenue was achieved because the technology-oriented AIS segment had registered record 44.7% growth that offset the minor decline in the year-on-year growth of the larger lighting business.

Financial Analysis

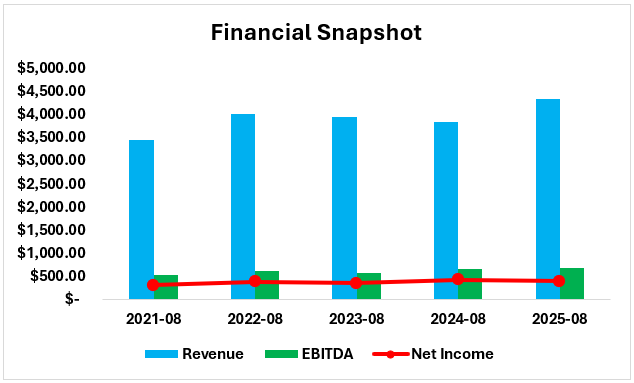

Acuity Brands has had a Revenue increase of a total of about 25.5% between August 2021 and August 2025, as its Revenue growth increased by a total of 3,461.00 million to 4,345.60 million in the same period. Although revenue experienced a slight decline in 2023 and 2024 with an underperforming lighting market and post-pandemic supply chain normalization, the business in 2025 experienced a colossal recovery with a growth of more than 500 million annually. This new boom was mainly fuelled by the aggressive growth of the Acuity Intelligent Spaces (AIS) division and the strategic purchase of the Q-SYS audio-visual platform that took the company to the next highest-demand building automation levels. The same trend was observed in the EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) of the company as it increased by 520.50 million in 2021 to record highs of 675.80 million in 2025. This gradual rise in EBITDA, despite any decline in revenue, underscores the achievements made by the management in its concentrated aim of achieving price-cost neutrality (and) operational efficiency, which, in effect, indicates that the company could get more cash out of every dollar in sales through selling higher-value technology products.

Nonetheless, Net Income has been more volatile with its highest point of $422.60 million in 2024 and its lowest point of $396.60 million in 2025. This small 6% drop in net profit, despite all-time high revenue and EBITDA, can be mostly explained by increased interest payments and one-off restructuring costs associated with job cuts in the old lighting business segment as the company shifts its human resource base to digital engineering. These numbers all lead to an image of a changing organization that is trading short-term net profit stability to invest in a more profitable software-integrated future.

Earnings History

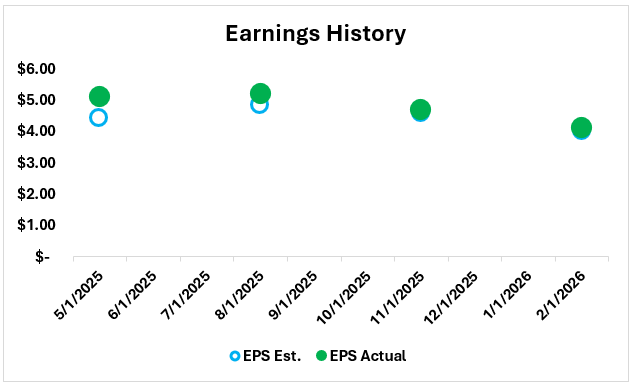

Acuity Brands has a proven history of operational excellence as the company has surpassed the analyst AYI earnings expectations in four consecutive quarters between May 2025 and February 2026. The company posted an impressive surprise figure of 15.3% in the period ending May 31, 2025, with an actual EPS of 5.12 as compared to an estimate of 4.44, indicating that the company is off to a great start in the fiscal year. This trend extended to the quarter ending on August 31, 2025, as the company attained a peak EPS of $5.20, again beating the forecast of 4.84. The size of these beats shrank as the company entered the 2026 fiscal year, but both quarter-ends were positive, with the quarter ending November 30, 2025 producing a $4.69 (a $0.10 beat), and the latest quarter ending February 28, 2026, producing a result of $4.14 compared to an estimated result of 4.00.

The steady performance of the company in achieving earnings targets, even though the absolute EPS values have been declining since 2025, demonstrates the effectiveness of the management in terms of its emphasis on profitability and cost management. These findings confirm that the company is successfully defending its margins via pricing and productivity improvements and can, therefore, create more-than-anticipated profits even when the overall lighting business is experiencing temporary volume "softness."

Valuation Analysis

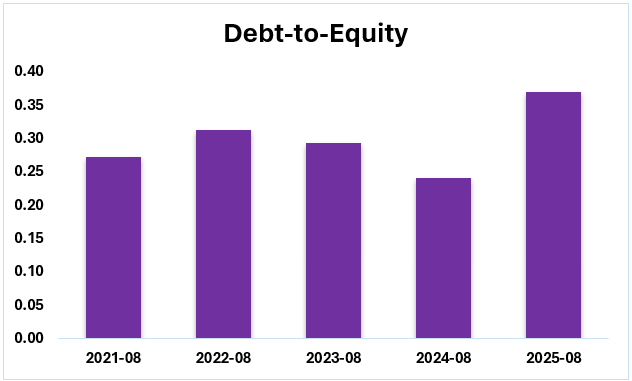

The company had a very stable and low leverage profile between 2021 and 2024 with a D/E ratio ranging between 0.24 and 0.31. Its lowest point was reached in August 2024 at 0.24, meaning that the company had 24 cents of debt per dollar of equity- an excellent financial position and lots of dry powder to invest in future. High cash flow generation and prudent borrowing environment in times of high interest must have contributed to this low leverage. In August 2025, however, the ratio saw a significant rise to 0.37, the highest level in the five years. Although the ratio of 0.37 is very safe and far below the danger levels in the industry, the growth of this 54 percent a year over year is a change in capital allocation. This increase in debt is directly related to the fact that the Q-SYS audio and control platform has been acquired by the company in mass, thus confirming that the management decided to use its strong balance sheet to finance a high growth technology expansion.

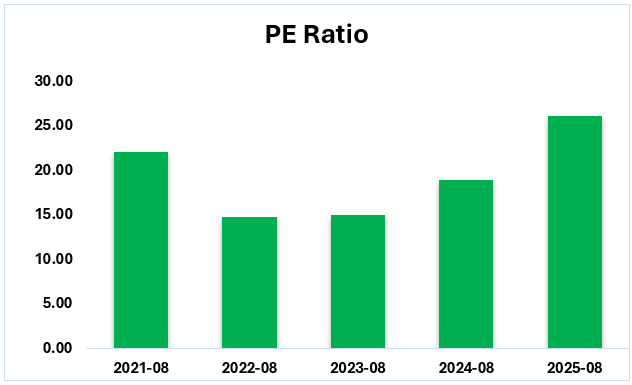

The P/E ratio of Acuity experienced a major re-rating between 2021 and 2025, going down to a minimum of 14.80 and up to 26.06. Such an increase in the valuation multiplier, 76 percent, means that the market has ceased to treat Acuity as a traditional lighting company and rather a high-growth technology company. Investors are now ready to pay a significant higher premium on each dollar of earnings, that is, betting on the future scalability of the Intelligent Spaces and Q-SYS software platforms.

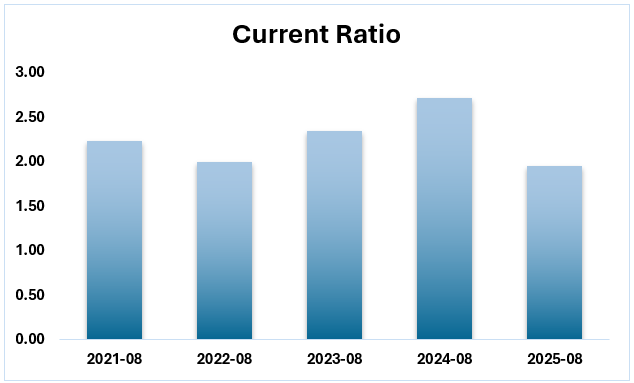

Acuity Brands has enjoyed a robust liquidity position since 2021-2025, and the Current Ratio was well above the healthy range of 1.0. From August 2021 through to August 2024, the ratio has been increasing by 0.52 to a high of 2.72, which is an extremely safe margin of covering current liabilities in the short run by current assets. Nonetheless, the ratio decreased to 1.95 in August 2025. Although it continues to reflect a strong financial position, this decline can indicate that there was a substantial utilization of cash or growth of current liabilities, probably associated with the intensive capital expenditure in the QSC acquisition and strategic investments in the Intelligent Spaces segment.

Risks

There are several risks that should be considered.

1.Although technology has improved, the Acuity Brands Lighting (ABL) segment continues to contribute the biggest share of overall revenue. The high interest rates have put the commercial market in a snarl, as core sales have decreased by 2.8 percent that could go on unless new construction starts picking up.

2.The data center infrastructure is experiencing a crowding out effect due to the explosive demand of data center infrastructure. This shift is capturing the local electrical labor and specialized electronic parts (including memory) needed on the Acuity conventional projects, which may cause the possibility of supply shock and project delays.

3.The Q-SYS acquisition increased the debt-to-equity ratio of the company to a five-year high of 0.37, and the P/E ratio to 26.06. This kind of tech-level valuation does not allow any mistakes; any stuttering in implementing new software platforms or a minor setback in Intelligent Spaces development may cause a severe market adjustment.

Conclusion

Acuity Brands evolves into a technology-based company with solid revenue growth, enhancing EBITDA, and steady earnings outperformance, as well as strong conversion of a traditional lighting manufacturer to a technology-based company. Though short-term net income variability and increasing leverage indicates continued strategic spending, especially on Intelligent Spaces and Q-SYS, the company is in good financial stand. Nevertheless, the vulnerability of the construction market and execution risk during its technology transition are still the issues. All in all, Acuity Brands is a promising business in the long term if it can cope with its strategic change and risks involved.

Sources

1.Musaffa

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Foziljon Kamolitdinov

Foziljon Kamolitdinov

Nusrat Ahmed

Nusrat Ahmed