Company overview

AutoZone is a major retailer of automotive accessories and replacement parts. Through its commercial operation, it serves professional repair companies in addition to selling to do-it-yourselfers. At the conclusion of the quarter, the company had 7,774 stores in Brazil, Mexico, and the United States.

What’s driving the story right now

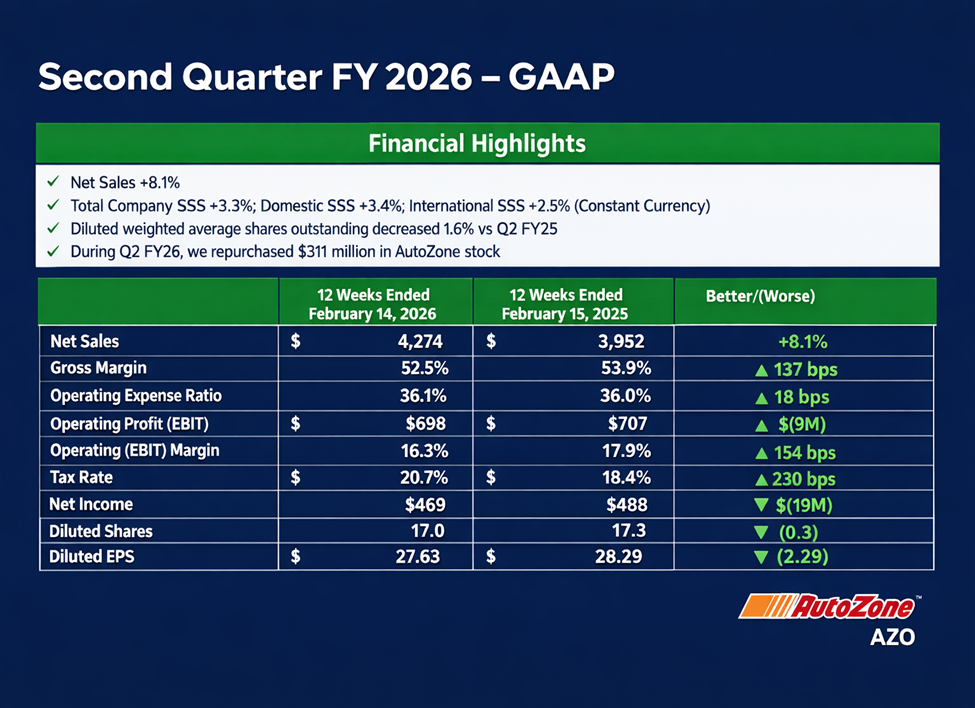

Demand strength was evident during the quarter. Same-store sales were up, and net sales increased to $4.27 billion (up 8.1% year over year). On a constant-currency basis, domestic AutoZone same-store sales rose by 3.4%, while overall business same-store sales increased by 3.3%. This is a crucial indicator, as it shows that sales at current stores are exceeding those of the previous year, rather than merely expanding through the opening of new locations.

Because profitability shifted in the opposite direction, the market's response was weaker. Due mostly to a non-cash AutoZone LIFO charge, the gross margin decreased from the previous year to 52.5%. Investors frequently question whether earnings can continue to rise even if sales remain strong while margins shrink.

Financial analysis

Highlighting the AutoZone Q2 FY26 results, AutoZone's revenue increased, but its profits did not. In Q2 FY26, net sales were $4,274 million, up from $3,952 million in the previous year. Net income was $468.9M compared to $487.9M the previous year, and operating profit was $698.5M (down 1.2% year over year). Diluted EPS was $27.63 as opposed to $28.29 in the previous year.

The commercial side remained robust. Domestic commercial sales increased 9.8% year over year to around $1,154.8 million. This is important because commercials can help smooth out outcomes over time and are typically more repeat-driven.

The quarter's cash flow was weaker. While capital spending was $327.5 million in Q2 FY26, cash flow from operations was $342.5 million as opposed to $583.7 million in the same period last year. Investors utilize cash flow as a "reality check" on the quality of earnings; a short-term decline in cash flow does not always indicate a problem.

Quarter check and Outlook

The results did not meet expectations. While non-GAAP EPS was $27.63 vs $27.17 predicted (a beat), revenue was $4.27 billion as opposed to $4.31 billion as anticipated (a slight miss).

Suppose the market doesn't like the "how," a stock may still decline on an EPS beat. In this case, operational profit was somewhat lower year-over-year, and gross margin decreased. Because it raises the question of whether margin pressure persists, that may be more significant than a slight EPS beat.

The margin narrative gains significant perspective from the guidance.

Management anticipates EPS of approximately $36.63 for the upcoming quarter (Q3 FY26). Additionally, the company plans to establish 350–360 new stores worldwide this fiscal year, with an additional 90–95 scheduled for the next quarter. Additionally, it is working for a quicker long-term pace of roughly 500 new store openings per year by FY2028.

In terms of expenses, the business anticipates non-cash LIFO charges of roughly $60 million in each of the next two quarters (Q3 and Q4), for a total of approximately $277 million for the fiscal year. This fiscal year, it intends to invest close to $1.6 billion in technology, distribution networks, and store expansion. To reach its long-term goal of 300 Mega Hubs, it also anticipates opening roughly 30 new ones this fiscal year.

To put it simply, management states that although the company is currently making significant investments in new shops and distribution to support future development, margins may remain under pressure due to ongoing LIFO costs.

Read More:

- TJX tops Q4 estimates, proposes dividend, and targets steady growth through FY27

- Ferguson Enterprises (FERG) Q4 2025 Earnings

- Tempus AI: High-Growth Healthcare Technology Analysis

Price and valuation context

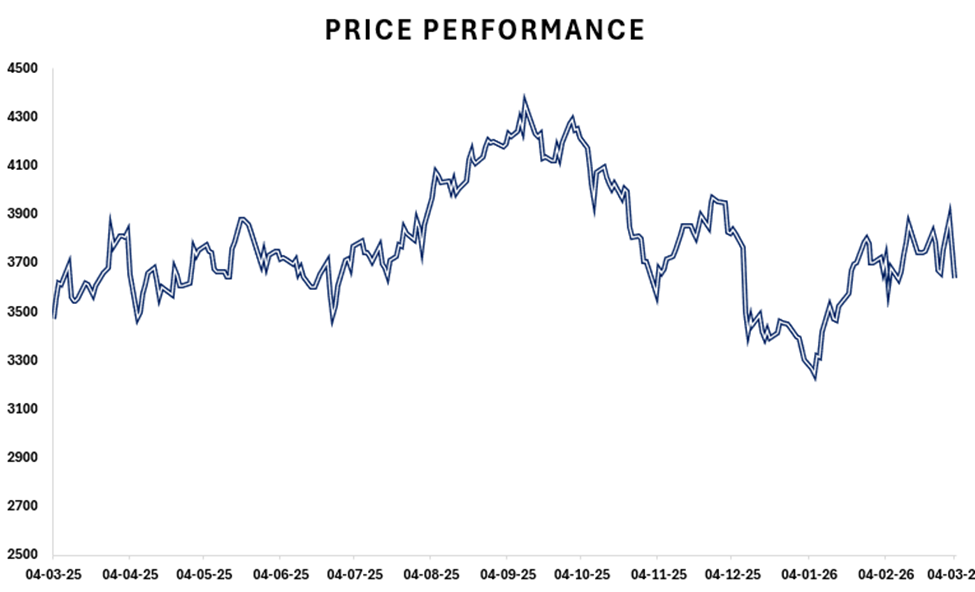

As of March 3, 2026, AZO closed at $3,637.17, down 6.32% for the day. The stock is below its 52-week high of $4,388.11 and has dropped 13.18% year to date. This implies that, despite stable demand trends, the market has grown more cautious.

P/E (TTM) of 25.35x and EV/EBITDA of 15.08x indicate that investors are paying for consistent earnings and execution, which is more in line with a high-quality retailer than with a high-growth story. P/FCF is roughly 24.1x, and EV/Sales is 3.36x. This indicates that the direction of cash flow and margins significantly impacts how the stock trades.

With a market capitalization of $60.26 billion and an enterprise value of roughly $63.67 billion, the financial situation suggests a net debt of roughly $3.41 billion. Additionally, the company benefits from a working-capital structure in which a significant amount of inventory is financed by suppliers: $7,449 million in inventory and $8,263 million in accounts payable. Inventory planning becomes crucial when costs and demand are changing, but it can also improve financial efficiency.

Risks

In terms of financial positioning, enterprise value is approximately $63.67 billion, while market capitalization is $60.26 billion, resulting in net debt of approximately $3.41 billion. Additionally, the company benefits from a working-capital structure in which a significant amount of inventory is financed by suppliers: $7,449 million in inventory and $8,263 million in accounts payable. Inventory planning becomes crucial when costs and demand are changing, but it can also improve financial efficiency. Quarter-to-quarter demand might also be distorted by weather; the corporation observed that winter storms caused business disruptions in late January and early February. Lastly, the company is making significant investments ($1.6 billion in capital expenditures) and accelerating store expansion, which may eventually pay off but could strain short-term cash flow if circumstances worsen.

Shariah Compliance

For investors reviewing Shariah-compliant stocks AZO, as of January 2026, AutoZone (AZO) is classified as Shariah-compliant (Halal) with a B+ Musaffa rating based on the Shariah Screening results at Musaffa. AZO’s 2026 1st Quarter Report was used to conduct the screening analysis in line with the AAOIFI methodology. AZO passed all three required screening thresholds, with 99.91% of its business activity meeting the permissible (Halal) threshold (0.00% doubtful and 0.09% not Halal). Both interest-bearing securities (0.79%) and interest-bearing debt (16.21%) remain below 30% of the 36-month average market capitalization.

Conclusion

In Q2 FY26, AutoZone demonstrated strong demand, with strong growth in the domestic commercial market and favorable same-store sales. The prognosis confirms that LIFO-related costs remain unfinished, and the market's response suggests concern that margin pressure may persist. To map out the AZO stock forecast relative to other auto parts retail stocks, the same-store sales trend, gross margin direction (particularly while LIFO charges persist), and whether cash flow stabilizes while the business continues to invest in shops and distribution are easy ways to track this story.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Musaffa Marketing

Musaffa Marketing