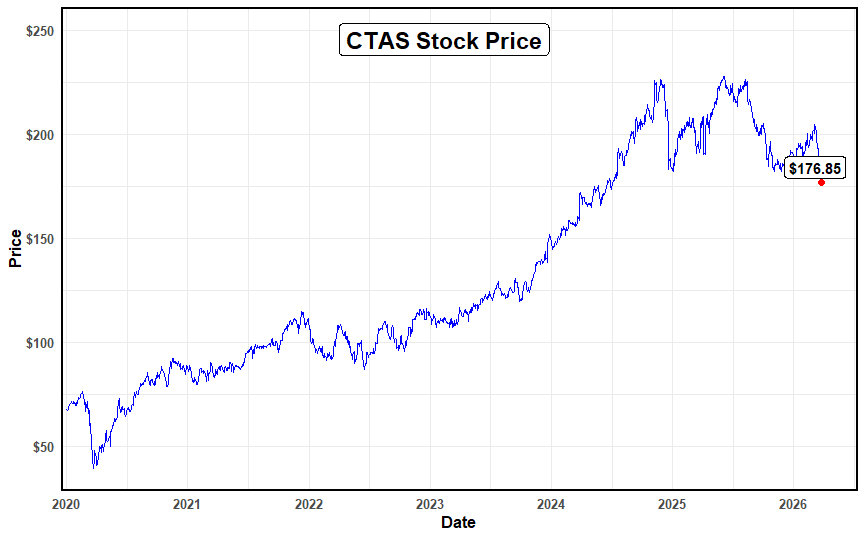

Cintas Corporation (CTAS, A+, Halal) specializes in providing highly specialized facility services and business supplies. They are mainly focused on providing uniform rentals, mats, mops, cleaning supplies, restroom products, and first aid and safety services and business supplies following their strong Cintas Q2 results. They make use of a route-based service delivery model to deliver and clean these supplies and products. The current market capitalization of the company is $76.53 billion, with a share price of $186.05.

Shariah status

For those seeking Shariah compliant stocks CTAS, the Shariah status of the company is considered halal, with a ranking of A+ according to the AAOIFI screening methodology by Musaffa. According to the screening results, 99.94% of its business activity is recorded as Shariah-compliant, while 0.06% is not halal due to interest income. Interest-bearing securities and debt account for 0.29% and 4.34% of their assets and liabilities, respectively.

Business analysis

For the first six months of fiscal 2026, in its Q2 results, Cintas posted a strong performance by reporting total revenue of $5.52 billion, an increase of an impressive 9.0% over the same period last year. This increase was consistent, as the Cintas Uniform Rental and Facility Services segment posted an increase of 8.2% to reach $4.25 billion in revenue, while the First Aid and Safety Services segment posted an increase of 14.4% to reach $676.9 million in revenue. The main cause of this increase was a record operating margin of 23.4%, achieved by leveraging "Cintas SmartTruck" AI technology to optimize delivery routes and minimize fuel and labor costs. This allowed Cintas to achieve an organic growth rate of 8.6% without relying on price increases, even as it faced fluctuating supply chain costs and a labor market that is increasingly complex. Additionally, Cintas focused on recession-resistant industries such as healthcare and hospitality, keeping service volumes high even as other industries cooled.

As such, Cintas was able to return over $1.24 billion in shareholder value in the form of buybacks and dividends while simultaneously increasing its full-year revenue guidance to a range of $11.15 billion to $11.22 billion.

Ultimately, the half-year results demonstrate that Cintas is succeeding in its evolution from a basic uniform provider to a high-tech "essential services" provider that companies are increasingly unwilling to eliminate from their budgets.

Financial analysis

Based on the performance of Cintas over the last six months, it’s easy to see that they are on an enormous winning streak, bringing in an impressive $5.52 billion in revenue, an increase of 9% compared to the same time the previous year. While the uniform business is still the main earner, the company’s First Aid and Safety segment is increasing its revenue much faster, by over 14%, proving that they are successful in selling more to the customers they already have.

The most interesting part of the report is the fact that they were able to achieve an impressive record operating margin of 23.4% because they are utilizing AI tools such as “SmartTruck” to make their delivery routes more efficient, thus saving on costs. The efficiency of the company has also allowed them to increase their goals for the remainder of 2026, along with returning over $1.24 billion to shareholders.

When it comes to the historical table from 2021 to 2025, it is clear that this is not a one-time thing. They have increased their revenues from $7.1 billion to over $10.3 billion in only five years. What is even more impressive is that their Net Income has grown by 63% in this same period, which is much faster than their sales growth. This basically proves that when Cintas is getting bigger, they’re also getting much smarter and more profitable with every dollar they earn.

Earnings analysis

The above financial data verifies that Cintas Corporation has a perfect "beat" record throughout 2025 in its CTAS earnings, as the firm continues to exceed the earnings per share (EPS) estimates made by analysts. As the firm entered the month of February 2025, the actual EPS was reported to be $1.13, which exceeded the estimated EPS of $1.06 by a margin of $0.07. This positive trend of beating the estimates was consistent throughout the firm’s performance in May and August, culminating in an actual EPS of $1.21 as of November 30, 2025, which exceeded the estimated EPS of $1.19.

The above data confirms that Cintas is more successful in controlling its internal expenses and increasing its high-margin service businesses than experts’ estimates. The steady rise in the actual EPS from $1.13 to $1.21 over the four periods verifies the firm’s trajectory of increasing its EPS, thereby executing its corporate growth strategy successfully. The above results verify the firm’s high level of financial discipline, which has enabled the firm to raise its long-term estimates and deliver record-breaking returns to its shareholders.

Valuation analysis

The Debt-to-Equity (D/E) ratios for Cintas over the five-year period up until May 2025 show the significant and strategic strengthening of the company’s balance sheet. The company’s D/E ratios experienced a brief peak of 0.90 in May 2022, but the company has consistently reduced its ratios for the past three years, reaching its lowest five-year rate of 0.57 as of May 2025.

The steady decline in the company’s D/E ratios, from 0.90 to 0.57, shows the company’s aggressive reduction of debt and its simultaneous growth in shareholder equity through record-breaking profits. A lower D/E ratio implies that the company is becoming less dependent on debt and is increasingly relying on its own cash flow for growth.

With such a conservative approach to its balance sheet, Cintas has put itself in the best position possible to make significant strategic moves, such as the acquisition of UniFirst, without overextending its credit

The Price-to-Earnings (P/E) ratio for Cintas Corporation has shown an interesting expansion over the past five years, rising from 34.53 in May 2021 to 51.48 in May 2025. The P/E ratio has been steadily climbing over the past five years, especially in the last two years, where there has been a sharp increase from 36.32 to 51.48. This shows that the stock price is rising much faster than the actual earnings of the company.

A rising P/E ratio is normally an indication that investors are becoming increasingly optimistic about the company's future performance. This means that investors are currently willing to pay a higher P/E ratio for this stock because they believe that, in the future, there will be significantly higher earnings for the company. This expansion in valuation is probably due to the company's ability to beat earnings estimates and its entry into high-margin segments such as the healthcare and fire protection industries. The P/E ratio of 51.48 is high compared to its historical P/E ratio but reflects that investors believe that this is currently a high-growth technology and services company rather than an industrial company.

The cash ratio of Cintas follows a fluctuating pattern over the five-year period, with the cash ratio peaking at 0.26 in May 2021, only to decline drastically to a low of 0.06 in May 2022. The drastic decline in the cash ratio over this period means that the firm was investing heavily, which led to a decline in cash and cash equivalents over the short term. However, the cash ratio has steadily increased to 0.19 by May 2024, before declining slightly to 0.16 by May 2025.

Risks

Cintas Corporation is vulnerable to various risks that might affect its future financial performance and industry standing:

- While Cintas focuses on non-cyclical industries such as healthcare, it is still highly sensitive to total employment levels in the economy. If there is an economic recession resulting in high levels of job losses, it will directly affect the total uniform-wearing population as well as the frequency of facility services required by clients.

- Cintas is highly vulnerable to labor cost inflation as well as fuel price volatility due to its labor-intensive nature of providing services. If Cintas is unable to fully offset these increased costs by leveraging its automated efficiency programs, it might compromise its profit margins.

- Cintas’s aggressive acquisition strategy of large-scale businesses, such as its ongoing merger with UniFirst, exposes it to significant risks of failing to successfully integrate complex logistics networks, corporate cultures, as well as proprietary technology platforms of acquired businesses.

Conclusion

Overall, Cintas exhibits strong growth, high profitability, and good financial discipline. The firm’s adoption of AI, along with its emphasis on essential services, is a testament to its long-term success among facility serving stocks, despite the risks of economic downturn and increased costs. The consistency of Cintas’ earnings, as well as its improving balance sheet, adds to its positive picture. Furthermore, high investor confidence bodes well for the firm’s future growth.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.