Johnson and Johnson (J&J, B, Halal) is a large American multinational company in the fields of healthcare, pharmaceuticals, and medical technology. Since the 2023 spin-off of its consumer health business (Kenvue), J&J currently focuses mostly on creating innovative medicines (diseases like oncology, immunology) and medical devices (orthopaedics, surgery, vision). The current market capitalization of the company is $547.51 billion, with the current Johnson & Johnson stock market share price of $230.69.

Shariah Status

The Shariah status of the company is considered halal among Shariah-compliant stocks, JNJ, with a ranking of B according to the AAOIFI screening methodology by Musaffa. According to the screening results, 98.50% of its business activities are Shariah-compliant, while 1.50% are not halal due to interest income. Interest-bearing securities and debt account for 5.02% and 11.98% of their assets and liabilities, respectively.

Business Analysis

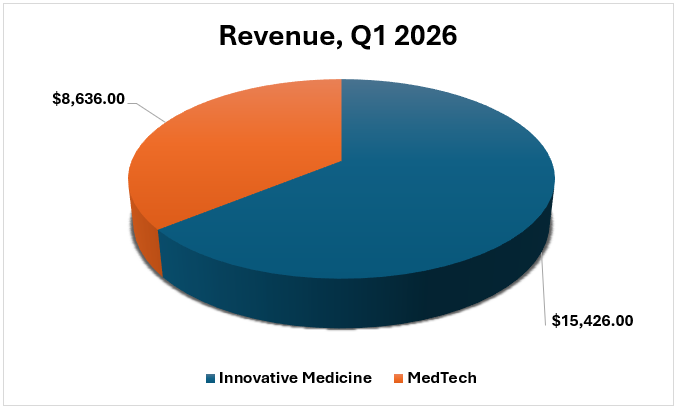

The information given on JNJ Q1 2026 indicates a strong beginning to the fiscal year, where the overall quarterly revenue is expected to be around $24.1 billion. The individual amounts of $15.4 billion of JNJ Innovative Medicine and $8.6 billion of JNJ MedTech show that the company is effectively implementing its strategy to offset the revenue lost to patent expirations by launching new products and acquiring new companies that are experiencing high growth. Its Innovative Medicine segment reported double-digit improvement of about 11 percent in this quarter, which is a huge accomplishment given the high level of headwind in the case of biosimilar competition of one of its blockbuster drugs, Stelara. This particular revenue figure was enabled by the outstanding performance of the oncology franchise, with the multiple myeloma therapy Darzalex bringing in close to 4 billion dollars in one quarter. In addition, the segment had the advantage of the faster acceptance of newer therapies like Carvykti and Tecvayli in the market, and the successful acquisition of Caplyta in a recent acquisition. The total amount of $15.4 billion also involves the initial business influence of Icotyde, a recently approved oral peptide for plaque psoriasis, which will be one of the significant growth drivers in the long term.

The revenue of the MedTech division is $8.6 billion, representing a gradual increase and a reported growth rate of about 7.7% compared with the same period last year. The cardiovascular sector was at the heart of this performance, with an increase in the demand for electrophysiology products and technologies of the recently acquired Shockwave Medical and Abiomed. The quarterly figure was also backed up by the stabilized mid-single-digit growth in the Orthopedics and Vision units, where a stabilized global supply chain and high procedure volumes in the United States supported sales. Although there was certain regional volatility in the international markets, the $8.6 billion figure is a confirmation that MedTech is a crucial and high-margin part of the simplified two-sector business model of the company. The key factor behind these particular Q1 totals was a planned front-loading of product launches and research spend aimed at the company hitting its ambitious target of $100 billion annual revenue by 2026. This was done through aggressive commercial performance within the U.S. market, which increased by more than 8 percent, and thus successfully covered the drastic reduction in revenue of older products that were under competition. Also, the company enjoyed positive exchange rates effects on some of its foreign markets, which contributed about 3.5 percent to the overall recorded rise in sales. Johnson & Johnson has also ensured that by sustaining a high investment in its pipeline during this first quarter, the firm has created a financial curriculum that enabled the management to increase the full-year forecast for sales and earnings.

Financial Analysis

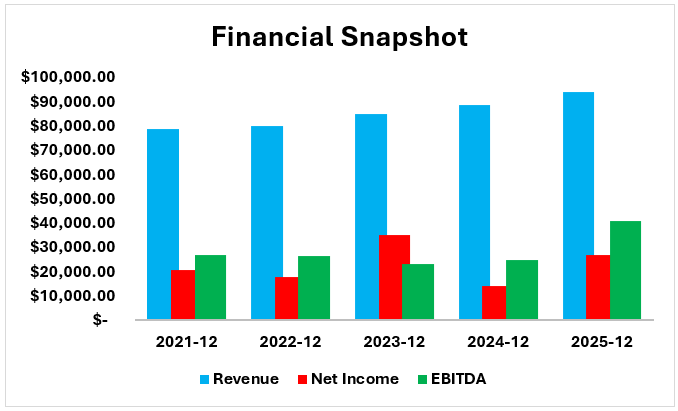

The 2021-2026 financial data shows that the company has been able to trade high-volume consumer goods for high-margin medical innovation. Through the divestiture of its consumer health unit, Johnson & Johnson increased its annual revenue to 94.2 billion dollars by 2025, a feat that was made possible by strongly relying on its Innovative Medicine unit and a renewed MedTech unit. The 2025 EBITDA of $41.1 billion underscores the fact that the business units have increased in operational efficiency by a great margin, which indicates that the rest of the business segments are much more profitable than the former conglomerate model. This trend persisted into Q1 2026 as the company brought in $24.1 billion in only three months, effectively offsetting the effect of the expiry of the patents with the success of the drugs such as Darzalex and new heart technologies. Although the Net Income of 2023 of $35.2 billion was artificially high through the Kenvue spin-off, the income of 2025 of $26.8 billion is a genuine and sustainable profit. Finally, these numbers imply a tactical shift that has stabilized the balance sheet of the company and put it on a definite path towards reaching over $100 billion in annual revenue.

Earnings Analysis

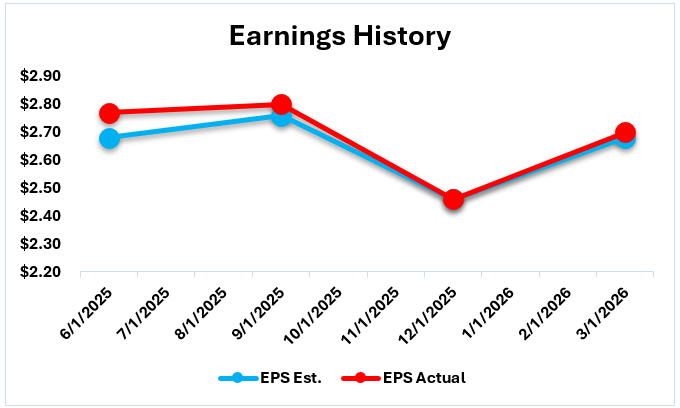

The JNJ Earnings Per Share (EPS) data from 2025 to 2026 (Q1) indicates some stable financial performance, and the actual performance is in line with the analyst’s expectations. The consistent EPS, which was between $2.46 and $2.80, was due to strong oncology sales and successful strategic acquisitions such as Shockwave Medical. The company experienced an adjusted EPS of $2.70 in Q1 2026, which is better than the estimated $2.68, as the company experienced a colossal 61.7% sales reduction of Stelara because of biosimilar competition. This "beat" was made possible by an 18% surge in Darzalex revenue and a strong 8.3% growth in the U.S. market. Johnson & Johnson has proven the strength of its new two-sector model by repeatedly exceeding forecasts, enabling the management to increase full-year 2026 expectations with a definite roadmap leading to the attainment of 100-billion-dollar annual revenues.

Valuation Analysis

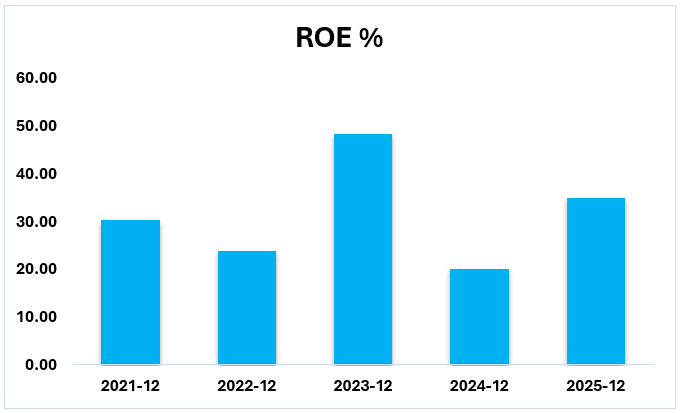

The 2021-2025 data on Return on Equity (ROE %) is a trace of how Johnson and Johnson turned into a high-efficiency medical giant. This massive spike was a one-time accounting gain of spinning off its consumer health business, Kenvue, and was thus a non-operational surge to 48.29% in 2023. After a transitional low in 2024 to 20.06, the 35.03% in 2025 is the real strength of the company following the restructuring. This 35% stabilized return is evidence that the company is now making a much greater profit on every dollar of shareholder equity than it was making with its old conglomerate structure by concentrating only on high-margin Innovative Medicine and MedTech.

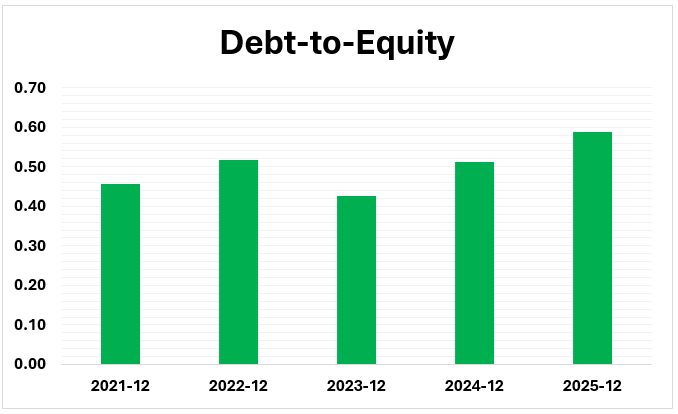

The 2021-2025 Debt-to-Equity (D/E) ratio shows how Johnson and Johnson utilized leverage to finance its huge corporate transformation. The increase in the ratio between 0.46 in 2021 and 0.59 at the end of 2025 indicates the capital needed to purchase high-growth companies such as Abiomed and Shockwave Medical, and at the same time to undertake the Kenvue spin-off. A D/E ratio of less than 0.60, despite this small increment, is still very conservative on the part of a healthcare giant, and this shows that the company is indeed expanding its debt-financed pipeline without jeopardizing its financial health in the long term. These numbers indicate that J&J is comfortably using its good balance sheet to offset older sources of revenue with high-margin medical innovations.

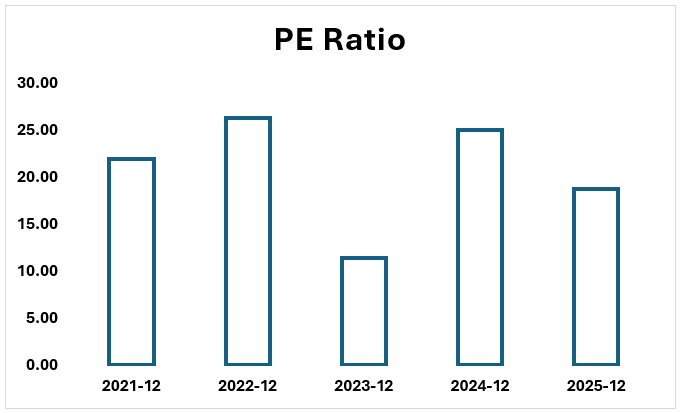

The P/E Ratio figures of 2021 to 2025 show how investors and the market have changed their attitude towards Johnson and Johnson and its valuation in its restructuring of corporate activities. The ratio that indicates the amount of money that the market is willing to pay per dollar of the company’s earnings is very volatile because of the huge one-off accounting events that have taken place over the past several years.

The steep decline to an 11.42 P/E ratio in 2023 was directly due to the Kenvue spin-off that artificially inflated earnings and made the stock seem "cheaper" on paper than it truly was. After adjusting the 2024 ratio to 24.98, the transition to a more balanced 18.76 P/E ratio in 2025 is a market that is valuing the company on its high-margin medical future and not its conglomerate history. This 18.76 number indicates that investors are getting increasingly comfortable with the risk profile and long-term growth prospects of the company in the fields of oncology and robotics. This trend is ultimately a shift towards a more defensive “value” stock to a more explosive healthcare innovator with a sustainable valuation.

Risks

- The company is experiencing a huge revenue loss due to the loss of exclusivity of its hottest-selling drug, Stelara, since biosimilar products offer a 60 percent reduction in sales. To sustain growth, J&J needs to quickly grow newer oncology and immunology assets to offset billions of lost annual sales (Investing).

- Current litigation on talc use is a billion-dollar liability, and more than 67, 000 cases await adjudication and insolvency efforts to pay claims. The threat of unforeseeable, huge jury awards still affects the valuation and cash reserves of the company (Drugwatch).

- The Inflation Reduction Act (IRA) will enable the government of the United States to negotiate the prices of the most successful drugs of J&J, directly threatening its profit margins. These are forced price reductions that hamper the earning capacity in the long run of the same products that are supposed to promote future growth (JNJ).

Conclusion

Johnson and Johnson has effectively evolved to be a lean, high-growth, Innovative Medicine and MedTech company out of a wide-ranging consumer conglomerate. Although the firm is experiencing serious headwinds, most notably the Stelara patent cliff and the current litigation over talc, the JNJ forecast indicators of 2025, as well as Q1 2026, show that the firm can overcome these factors due to its intensive innovation in oncology and heart health. Having a stabilized ROE at 35% and a clear path toward achieving over $100 billion in annual earnings, J&J is demonstrating that its tighter focus on breakthrough medical innovations that are high stakes is providing it with greater efficiency and sustainable value to shareholders.

Sources

Disclaimer: This content is provided for informational purposes only and does not constitute investment, legal, tax, or financial advice, nor a recommendation to buy or sell any security. It is not tailored to your financial situation, risk tolerance, or investment objectives. Past performance does not guarantee future results, and all investing involves risk, including loss of principal. All opinions, analyses, forecasts, and estimates reflect the author’s views as of the publication date and may change without notice. Market conditions can change rapidly.

Stock screenings, Halal status, ratings, and classifications are based on AAOIFI standards and the oversight of Musaffa’s Shariah scholars and may change over time. Musaffa Islamic Socially Responsible Investing (MISRI) rankings are proprietary, may be in beta, and are not guaranteed to be accurate or complete.

Musaffa is a registered investment advisor (RIA) but is not a broker or dealer. Registration does not imply endorsement by the SEC. Musaffa does not execute or solicit securities transactions. Analysts may be internal or third-party contributors and are not necessarily licensed or certified to provide any professional advice.

Information is provided “as is” and may be sourced from third parties. Musaffa does not guarantee accuracy, completeness, or timeliness and is not responsible for errors or third-party content. Logos and trademarks are used for identification only and do not imply endorsement.

Readers should conduct their own research and consult qualified financial and/or religious advisors before making any decisions. For further details, please refer to the General Disclaimer.

Analyst’s Disclosure: I/we hold no positions in any securities mentioned and have no plans to initiate any within the next 72 hours. This article reflects my own opinions, for which I receive no compensation other than from Musaffa. I have no business relationship with any company mentioned.

Foziljon Kamolitdinov

Foziljon Kamolitdinov

Nusrat Ahmed

Nusrat Ahmed